Preamble

You get more impact when you ship finished products, not raw commodities. For millet and sorghum, that means safe flours, instant porridges, breakfast snacks, and malt beverages. For shea, it means butter and fractions like stearin for chocolate and cosmetics. Markets are expanding, and governments are nudging exporters to process at home. Nigeria, for example, prohibited raw shea nut exports in 2024 to push domestic processing. (globalshea.com)

Millets and sorghum are climate smart and fit drylands. They grow with less water and handle heat better than many cereals, which strengthens resilience in Sahelian and savannah zones. Shea parklands add a further edge. They store carbon and support millions of women collectors and processors. These properties make the trio ideal anchors for a regional value-add strategy. (FAOHome, Open Knowledge FAO, globalshea.com)

My rough notes : Outline artefacts

The case for moving up the processing value chain and adding circular market dynamics

Abstract

Processing raw millet, sorghum, and shea nuts into flours, snacks, beverages, and shea butter can multiply farmer incomes, create skilled jobs, and reduce environmental pressure if planned well. Global markets are growing for all three product families. The millet market is projected at 38.9 billion dollars in 2024 and 55.7 billion dollars by 2030. The sorghum market is projected at 23.2 billion dollars in 2024 and 31.8 billion dollars by 2030. The global shea butter market keeps expanding across food and cosmetics. Policy signals are also shifting toward domestic value addition, including Nigeria’s 2024 ban on raw shea nut exports. Processing delivers strong value uplift. Raw shea nuts priced at about 0.42 to 0.58 dollars per kilogram become butter that sells at roughly 4.33 to 6.26 dollars per kilogram, an eight to ten times increase. Circular models turn husks, bran, shells, and wastewater into feed, briquettes, biogas, or activated carbon. This article maps stakeholders, sizes markets, quantifies value uplift, compares scaling models, and outlines finance-ready mini business plans. It closes with policy actions and incentives that help public agencies and investors back inclusive, low-carbon growth. (Grand View Research, globalshea.com, ScienceDirect)

Stakeholder mapping

- Farmers and collectors. Smallholders who produce grains or collect shea. Women dominate shea collection and processing. About 16 million women participate across the shea belt. (globalshea.com)

- Aggregators and cooperatives. Organize supply, quality, and payments. Women’s groups are central in shea. (Savannah Fruits)

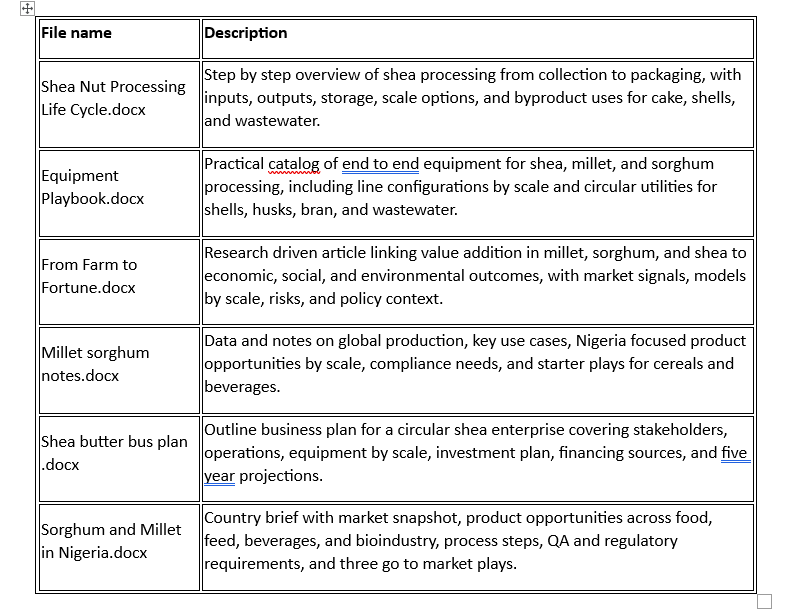

- Processors. Micro units, regional SMEs, or industrial parks. Typical lines and capacities appear in the attached Equipment Playbook for shea, milling, extrusion, beverages, and feed.

- Exporters and offtakers. Local brands, regional buyers, global firms in food and cosmetics. Examples include Nigerian Breweries for sorghum malt beverages and international shea buyers. (Nigerian Breweries PLC.)

- Government agencies. Standards, export promotion, incentives, and trade policy, for example NEPC and customs. (NEPC)

- NGOs and development partners. Organize training, finance, and certification. Savannah Fruits Company’s work with women’s cooperatives is a strong example. (West Africa Trade & Investment Hub)

- Investors and lenders. Banks, DFIs, impact funds, diaspora investors.

- Research and QA institutions. Universities, FIIRO, standards bodies, and labs.

- Consumers. Local households, school feeding and safety nets, export buyers.

Market size and growth potential

- Millet. Global market size estimated at 38.90 billion dollars in 2024, projected to 55.71 billion dollars by 2030, CAGR about 6.2 percent. Other analysts give a lower 2024 base near 15.3 billion dollars. Treat the band as a range driven by scope differences. (Grand View Research, Global Market Insights Inc.)

- Sorghum. Global market size estimated at 23.19 billion dollars in 2024, with a path to 31.77 billion dollars by 2030. Food and beverage sorghum specifically at 3.43 billion dollars in 2024, growing 5.9 percent CAGR to 2030. (Grand View Research)

- Shea. Demand is rising in cosmetics, confectionery, and specialty foods. EU buyers source kernels and butter through companies such as Bunge and Cargill alongside certified Fairtrade and organic channels. (CBI)

Policy tailwinds

Nigeria’s 2024 raw shea export ban pushes value addition at home. Nigeria also runs the Export Expansion Grant with 5 to 15 percent rebates based on product category for qualifying exporters. Customs granted temporary duty and VAT waivers on key food items in 2024, and broader rules already provide zero duty on many agro machines. These measures affect input costs and competitiveness. (globalshea.com, NEPC, KPMG, nigerianembassythehague.nl)

Value addition through processing

- Shea nuts to shea butter and fractions. Typical farmgate or export parity price for raw shea nuts is about 0.42 to 0.58 dollars per kilogram. Refined or filtered shea butter commonly trades at about 4.33 to 6.26 dollars per kilogram, and EU import notes show stearin fetching several thousand euros per ton. Even without full refining, moving to butter multiplies value roughly eight to ten times. (ScienceDirect, iesc.org)

- Millet and sorghum to consumer foods. Dehulling, milling, extrusion, and controlled fermentation convert 200 to 350 dollar per ton grain into ready-to-eat or ready-to-cook foods that retail at a much higher ex-factory price. Instant porridges and extruded cereals are proven categories in Nigeria.

- Malt beverages and adjuncts. Sorghum malting and beverage lines have a strong Nigerian track record after the 1988 barley ban, which led brewers to develop local sorghum supply chains. (Nigerian Breweries PLC.)

Scaling models and employment

Use these indicative configurations to scope projects. Capacities and line-ups are taken from the Equipment Playbook and the sorghum–millet processing briefs.

Small scale, community or cooperative

- Typical products. Shea butter in jars, millet and sorghum flours, fermented beverages in PET.

- Equipment. Solar tunnel dryer, hand or motorized crackers, LPG roaster, small screw press and filter press for shea. Pre-cleaner, small dehuller, hammer mill, sachet sealer for grains.

- Capacity. 100 to 500 kilograms kernels per day for shea extraction; 0.5 to 2 tons grain per day for milling.

- Jobs. About 10 to 25 direct roles depending on shift.

Medium scale, regional SME hub

- Typical products. Drum-filled shea butter, instant porridge from a twin-screw extruder, pasteurized kunu or malt drinks, bran-to-feed reuse.

- Equipment. Roller cracker with aspiration, continuous roaster, press battery, vacuum dryer for shea. Intake cleaning, pearler, roller mill, twin-screw extruder with dryer and packer, small PET line with tunnel pasteurizer for grains.

- Capacity. 1 to 10 tons kernels per day for shea; 2 to 10 tons instant foods per day; 5,000 to 20,000 liters beverages per day.

- Jobs. About 50 to 100 direct roles.

Large scale, industrial park

- Typical products. Refined shea butter and fractions, aseptically filled beverages, high-capacity extrusion, integrated 20 ton per hour feed mill.

- Equipment. Continuous roaster, press plus extractor and refining, aseptic bulk filling. Full intake with dryers and silos, high-capacity extruder line, aseptic PET block, biochar unit.

- Capacity. 20 to 200 tons kernels per day for shea; 1 to 3 tons per hour extruded foods; 50,000 to 200,000 liters per day beverages.

- Jobs. About 200 to 400 direct roles.

Risk analysis

- Operational. Heat steps, moisture control, and hygienic design are critical, especially for fermented drinks and instant foods. Build HACCP around fermentation, water activity, and mycotoxins.

- Financial. FX volatility, seasonal raw material swings, and working capital for inventory and packaging.

- Market. Brand acceptance, certification gaps, buyer concentration in shea.

- Climate. Droughts and heat waves. Millets and sorghum mitigate exposure compared to maize, but variability still matters. (FAOHome)

- Policy. Export bans or tariff changes can shift margins and inventory risk. (globalshea.com)

Circularity and sustainability

Circular economy opportunities

- Millet and sorghum bran and husks. Convert to feed pellets or briquettes. Studies support millet husk briquetting for clean energy. (ScienceDirect)

- Shea shells. Carbonize and activate into biochar or activated carbon for water and air applications. The Equipment Playbook lists carbonizer and activation kiln options by scale.

- Shea cake. Use as fuel briquettes or a feed ingredient where permitted.

- Wastewater. Use biodigesters to produce biogas and liquid fertilizer.

Environmental impact

- Climate resilience and water. FAO notes millets grow with little water and high heat. Research shows C4 millets have higher water use efficiency than many C3 cereals. (FAOHome, Frontiers)

- Agroforestry carbon. The shea value chain fixes an estimated 1.5 million tons of CO₂ per year. Lifecycle work suggests each ton of kernels may carry a net negative carbon footprint when trees and soils are counted. (Open Knowledge FAO)

Use cases and innovation

Case studies

- Dala Foods, Nigeria. Commercial instant fura and millet beverages show demand for safe, branded heritage foods. (dalafoodsng.com)

- Nigerian Breweries. Sorghum substitution during and after the 1988 barley import ban built a lasting malt sorghum ecosystem. (Nigerian Breweries PLC.)

- Savannah Fruits Company. Co-investments with development partners expanded organic and fair-trade shea butter exports while growing cooperative incomes. (West Africa Trade & Investment Hub)

Digital integration

- Traceability and inventory. Deploy FarmERP or AgUnity-style tools for QR code traceability, batch records, and audits. (Listed in the uploaded shea business plan.)

Packaging concepts

- Foods. Nitrogen-flushed laminates for instant cereals, multihead weighed portion packs, PET bottles with tunnel pasteurization for ready-to-drink products.

- Shea. Net weight fills for drums and totes, optional aseptic bulk for food grade butter.

Strategic frameworks

PESTLE summary

- Political. Supportive signals for local processing and export growth, including EEG rebates and targeted waivers. (NEPC, KPMG)

- Economic. Large and growing global demand bands for millets, sorghum, and shea categories. (Grand View Research)

- Social. Women’s economic empowerment through shea, nutrition gains from millet and sorghum in school feeding and retail. (globalshea.com)

- Technological. Proven lines for extrusion, malting, refining, PET pasteurization, and biochar.

- Legal. Food safety, labeling, and export standards.

- Environmental. Carbon storage in shea parklands and water-efficient grains. (Open Knowledge FAO)

SWOT summary

- Strengths. Climate-smart crops, strong heritage demand, women-led shea networks.

- Weaknesses. Quality variability, capex for modern QA and utilities, FX exposure.

- Opportunities. Value uplift from kernels to butter and stearin, instantized foods, traceability premiums, byproduct valorization. (iesc.org)

- Threats. Weather shocks, policy swings, buyer consolidation.

Appendices A and B below provide full PESTLE and SWOT matrices with detailed factors.

Business plan outlines

All figures are indicative model ranges in USD based on typical line-ups and capacities described in the Equipment Playbook and processing notes. Use them to build RFQs and verify with vendor quotes.

A) Small cooperative shea cell

- Scope. Solar drying, cracking, roasting, pressing, filtration, jar or pail filling, briquetting of cake.

- Capacity. 300 to 500 kilograms kernels per day, 40 to 45 percent butter yield.

- CapEx. 80,000 to 150,000 dollars (fabrication, installation, QA kit, working tables).

- OpEx per year. 60,000 to 90,000 dollars (nuts, fuel, labor, packaging, QA).

- Revenue per year. 100,000 to 180,000 dollars at 2.0 to 3.0 tons butter per month priced 3,500 to 5,000 dollars per ton ex-factory.

- Cost structure. Variable 70 to 75 percent, fixed 25 to 30 percent.

- ROI and payback. 25 to 50 percent pre-tax ROI, 18 to 36 month payback if quality and sales are steady.

- Notes. Map suppliers through women’s groups and build lots around moisture and free fatty acid targets.

B) Medium millet–sorghum hub

- Scope. Cleaning, dehulling, roller milling, blending and fortification, twin-screw extrusion with dryer and packer, small PET line for pasteurized beverages, bran to 2 ton per hour feed line.

- Capacity. 2 to 6 tons instantized foods per day plus 5,000 to 20,000 liters beverages per day.

- CapEx. 1.5 to 3.5 million dollars.

- OpEx per year. 1.2 to 2.5 million dollars.

- Revenue per year. 2.0 to 4.0 million dollars at 1,600 to 2,200 dollars per ton ex-factory for instant cereals and 0.6 to 1.0 dollars per 500 ml beverage.

- Cost structure. Variable 70 to 80 percent, fixed 20 to 30 percent.

- ROI and payback. 15 to 30 percent pre-tax ROI, 3.5 to 6 year payback depending on utilization and mix.

C) Large integrated agro-industrial campus

- Scope. Refined shea butter and fractions, high-capacity extrusion and cereal snacks, aseptic PET beverages, 20 ton per hour feed mill, biochar and biogas utilities.

- Capacity. 50 to 150 tons kernels per day processed, 1 to 3 tons per hour extruded foods, 50,000 to 200,000 liters per day beverages.

- CapEx. 12 to 25 million dollars.

- OpEx per year. 8 to 18 million dollars.

- Revenue per year. 15 to 35 million dollars.

- Cost structure. Variable 75 to 82 percent, fixed 18 to 25 percent.

- ROI and payback. 12 to 20 percent pre-tax ROI, 5 to 8 year payback, sensitive to export contracts and EEG recovery. (NEPC)

Policy recommendations and investment incentives

- Tie export privileges to value addition. Maintain raw-kernel export limits where local processing is viable, with clear phase-in periods and support to cooperatives. Nigeria’s 2024 raw shea policy is a reference point. (globalshea.com)

- De-risk first movers. Expand matching grants and concessional debt for small and medium lines. Prioritize circular utilities like biodigesters and carbonizers.

- Quality infrastructure. Fund regional labs for moisture, free fatty acids, aflatoxins, and micronutrients to reduce QA costs for SMEs.

- Export incentives and recovery. Ensure predictable EEG settlements and fast-track exporter baselines each year. Use Export Credit Certificates to offset taxes due. (NEPC)

- 0 percent duty on processing equipment. Enforce zero duty on agro-processing machinery, spares, and test kits. Publicize the schedule so SMEs plan imports with confidence. (nigerianembassythehague.nl)

- Public procurement pull. Include millet and sorghum instantized blends in school feeding and safety net tenders with clear specs, to anchor demand and crowd in private investment. (executiveboard.wfp.org)

Conclusion

You can turn climate-smart crops into jobs, export earnings, and healthier diets by processing where the crops grow. Millet and sorghum give resilient food and beverage platforms with strong circularity. Shea combines women’s income, carbon storage, and high-value exports. The business math works at cooperative, SME, and park scale when quality and offtake are locked. Next candidates for value addition in similar models include cocoa derivatives, cashew kernels and shell liquid, moringa leaf and seed oil, and baobab powder.

Appendices

Appendix A. Full PESTLE

- Political.

- Export incentives through EEG at 5 to 15 percent bands. Targeted bans or restrictions on unprocessed exports where domestic capacity exists. (NEPC, globalshea.com)

- Economic.

- Growing global markets for millets and sorghum. Sheabased ingredients in both food and cosmetics. Foreign exchange savings by substituting imports in beverages and breakfast foods. (Grand View Research)

- Social.

- Women-centered shea incomes. Nutrition benefits from diversified grains. Youth jobs in QA, maintenance, and digital traceability. (globalshea.com)

- Technological.

- Modular lines for milling, extrusion, PET pasteurization, and refining, with vendor presence in Nigeria and West Africa.

- Legal.

- Standards and registration for micro and small enterprises, HACCP, aflatoxin control, and labeling.

- Environmental.

- Millets and sorghum need less water than many cereals in hot environments. Shea parklands fix carbon and stabilize soils. (FAOHome, Open Knowledge FAO)

Appendix B. Full SWOT

- Strengths.

- Value uplift from kernels to butter and fractions. Proven heritage demand for millet and sorghum foods. Extensive women’s networks in shea. (iesc.org)

- Weaknesses.

- Variable raw quality, gaps in cold chain for beverages, and capex intensity for modern QA.

- Opportunities.

- QR-coded traceability and certification premiums. Bran, husk, and shell valorization into feed, briquettes, biochar, and activated carbon. Public procurement for school feeding.

- Threats.

- Climate shocks and price spikes. Policy changes on export or import waivers. Buyer concentration in shea.

References

- Market sizes and forecasts

Grand View Research millet market, 2023 to 2030; and press release highlights. Grand View Research sorghum market, plus F&B segment statistics. Global millets market alternative estimate by GMI. (Grand View Research, Global Market Insights Inc.) - Policy and incentives

Nigeria raw shea export ban. NEPC Export Expansion Grant details. Temporary zero duty and VAT waiver in 2024. Tariff-based incentives for agro machinery. (globalshea.com, NEPC, KPMG, nigerianembassythehague.nl) - Shea economics and social impact

Tridge price pages for shea nuts and shea butter. Global Shea Alliance and UNDP notes on women’s participation. EU buyer overview for shea. (ScienceDirect, iesc.org, globalshea.com, CBI) - Environmental and circularity

FAO millets resilience page. Bockel et al. on shea’s negative carbon footprint per ton of kernels. Millet husk briquetting study. Equipment Playbook circular utilities. (FAOHome, Open Knowledge FAO, ScienceDirect) - Case studies

Dala Foods products. Nigerian Breweries sorghum history. Savannah Fruits Company trade hub brief. (dalafoodsng.com, Nigerian Breweries PLC., West Africa Trade & Investment Hub)

Notes for implementation

- Use the Equipment Playbook to draft RFQs, define capacities, and pick one small, one medium, and one large configuration to pilot.

- Follow the millet–sorghum briefs for NAFDAC registration steps, SON standards, and hazard

{kind=link}

{kind=link}

{kind=link}

{kind=link}