Preamble

In Part 1 Cyber Cafés to Immersive Hubs Part 1: The Next Evolution of Shared Tech Spaces I explored how underused malls, town centers, and cultural venues can evolve into immersive, AI powered, human scaled hubs for gaming, learning, creation, and global social connection. Part 2 moves from concept to decision. You will get a clear view of viability, risk, and investment criteria, plus the unit economics and practical steps that let an investor, landlord, or operator say yes with discipline.

1) Investment thesis in one page

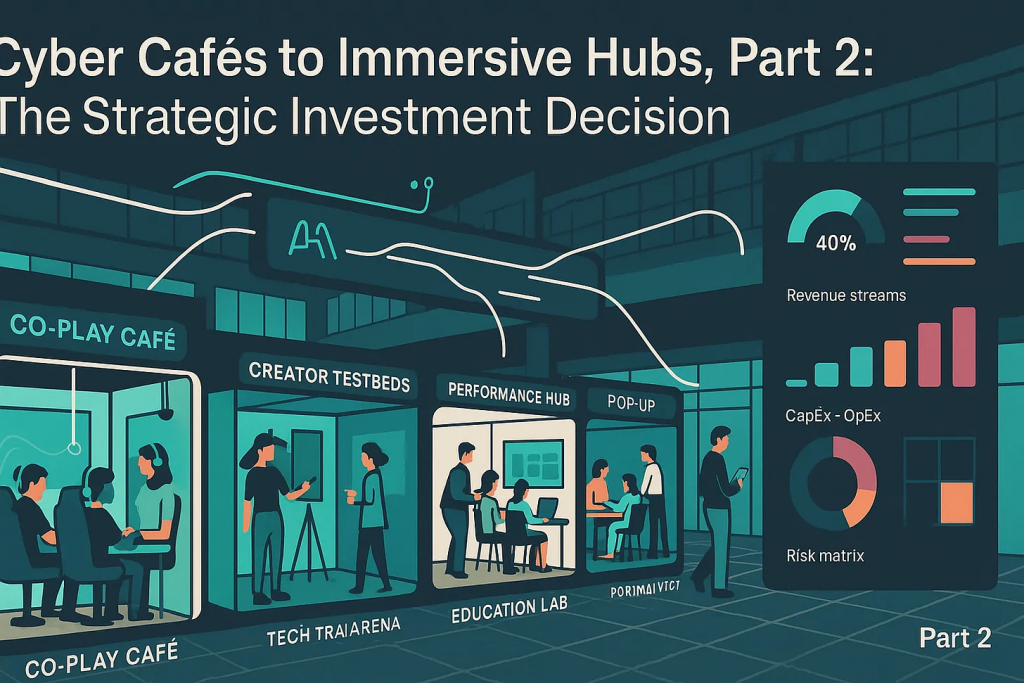

Immersive hubs convert underutilized real estate into adaptive spaces that accelerate XR and AI adoption. They work as community magnets, brand demo labs, creator studios, and event venues in a single modular footprint. The white space sits between single format VR arcades, esports arenas, and coworking. The opportunity is a hybrid model that blends multi use creation, trials, and events with AI orchestration and seasonal programming. This aligns with your typology of Co Play Café, Creator Testbeds, Tech Trial Arena, Performance Hub, Tourism Labs, and Hybrid Service Hubs.

From an investment lens, the model wins when you 1) diversify revenue across time based access, memberships, events, studio services, and brand labs, 2) reduce CapEx risk with modular fit out and leased hardware, and 3) lock weekday utilization through education and B2B contracts. The strategic rationale and value stack are set out in the investment memorandum and carry through to Part 2.

As usual some outline artefacts Two versions of strategic investment analysis

- Document name: Immersive Shared Tech Spaces, Strategic and Investment Analysis

Short description: A full market and strategy review for hybrid immersive venues, covering trends, demand drivers, competitive landscape, PESTLE, SWOT, Five Forces, financials, real estate strategy, and rollout plan. - Document name: Project Alpha, Strategic Investment Memorandum

Short description: An investor ready memo that sets the vision, thesis, unit economics, property strategy, operating model, and staged growth plan for a global network of immersive tech hubs. - Analysis documents .CSV sensitivity and finance

- Snapshot: Global Market malls and town centres

2) Market context that matters to returns

- XR demand is shifting from novelty to utility. Analysts project strong growth to 2030, with education and enterprise as key drivers. This supports staffed, pro grade access in shared venues.

- Location based entertainment continues to expand, with North America leading and Asia Pacific growing fastest. Momentum helps sponsorship and footfall.

- Headset landscape. Meta holds share through education and mixed reality content. Apple Vision Pro shows stronger traction in enterprise pilots than consumer, which favors venue based trials and design workflows.

- UK context. Retail vacancy is easing and landlords are selectively supporting experiential anchors, which improves lease and incentive terms for a first site. Bank Rate sits near 4 percent in late 2025, so debt cost is material, but rent incentives can offset unit economics during ramp.

3) Unit economics snapshot, single site

A reference site of about 8,000 to 15,000 square feet can host roughly 40 stations across the four core zones, plus an event area and a compact studio. A base monthly picture from the working model:

- Seats 40, open 12 hours for 30 days.

- Average hourly price 12 pounds.

- 300 members at 60 pounds.

- Events, 600 tickets at 15 pounds.

- Brand labs and sponsorship, 15,000 pounds.

- Studio hire, 120 hours at 35 pounds.

- Fixed costs roughly 71,000 pounds, plus depreciation on 350,000 pounds CapEx over 36 months.

In the memo, typical per location CapEx for a smaller footprint is around 600,000 dollars for fit out and hardware, with monthly OpEx of 37,000 to 52,000 dollars depending on city. The principle holds across currencies and sizes, you scale the zones and hours to match the catchment.

What moves EBIT the most. Occupancy and sponsorship. At about 50 percent occupancy, EBIT hovers near breakeven after depreciation. A move to 60 percent occupancy, with constant pricing and sponsor floors, pushes the site into healthy territory. That is why weekday institutional blocks and outcome based brand labs sit first in the sequencing.

4) Scenarios and sensitivity you can act on

Use three live scenarios for committee review.

- Base case, 50 to 55 percent blended occupancy. Two anchor sponsors on minimum guarantees. 300 members. Events keep weekends full. Breakeven after depreciation sits near the twelve to fifteen month window if sponsor floors are in place.

- Upside case, 60 to 65 percent occupancy and a corporate off site package twice per month. Outcome fees for qualified demos. Creator Pro uplift adds mid four figures monthly. Payback on fit out in 24 to 30 months becomes realistic.

- Downside case, 40 to 45 percent occupancy and one sponsor delay. Trigger the contingency plan, push school and workforce blocks, run pop up activations, and lean on venue media inventory until the next sponsor signs.

The investment memorandum flags the same sensitivities, especially the impact of a 10 percent change in occupancy on break even timing, and the advantage of leasing fast depreciating hardware.

5) Funding mix and deal structure

Per site, target a blended approach:

- 40 to 50 percent lease or vendor financing for fast cycle hardware.

- 30 to 40 percent tenant contribution or landlord incentive for fit out, helped by experiential anchor status.

- 10 to 20 percent equity for working capital and ramp.

Goal, recover upfront fit out in 24 to 30 months through EBITDA and incentives.

Pair this with stepped or turnover rent bands tied to traffic and PR commitments. Add break options linked to season performance. These terms protect downside in a rate volatile environment.

6) Site selection criteria that reduce risk

- Catchment. Dense, mixed use clusters near transit, universities, and malls. Strong evening and weekend traffic.

- Envelope. 3 phase power, cooling capacity, darkening and acoustic treatment, ceiling grid for truss, accessible ground or first floor with lift.

- Zoning. Confirm assembly and leisure use, audio rules, filming consent, and F&B permissions.

- Scalability. 8,000 to 15,000 square feet for a full hub. 2,000 to 4,000 square feet for pop ups and testbeds. Modular kit of parts to refresh zones without downtime.

7) Revenue design that hardens the P&L

- Time based access by zone and daypart.

- Membership ladder, Casual, Creator, Pro, with studio credits and priority booking.

- Events with ticketing, VIP boxes, and F&B.

- Brand labs, minimum guarantees plus outcome fees for qualified trials and follow ons.

- Studio micro services, volumetric portraits, scans, short edits.

- Education and NGO blocks, 3 to 4 hour weekday sessions.

- Data and insights, opt in dashboards for partners under strict privacy.

Near term profit moves, with conservative uplifts, include weekday institutional blocks, Creator Pro subscriptions, dynamic pricing, outcome based brand labs, corporate off sites, studio packs, mobile pop ups, and a media loop inside the venue.

8) Risk register with concrete mitigations

Financial. Sponsorship concentration and pop up cash flow variance. Mitigate with a cap per sponsor share of floor, three to four anchors per season, deposits for mobile activations, and standardized kits.

Operational. Staff skill gaps, device downtime, and content refresh. Mitigate with micro certifications, hot swap bays and a 15 percent spare pool, and eight to twelve week seasons that rotate partners.

Regulatory. Privacy, consent for capture, child safeguarding, and accessibility. Mitigate with consent desks and receipts, DPIAs, enhanced checks, age rated libraries, and published accessibility guides.

Market. Home device substitution and tech obsolescence. Mitigate with leased hardware, venue only content and social creation, and a hardware lifecycle that refurbishes and redeploys older rigs into pop ups.

The memorandum adds legal and environmental notes, including AI content IP and an energy conscious shared resource posture.

9) Due diligence checklist for committees and landlords

- Demand. Primary research with local schools, FE colleges, and creator groups. Pre sell weekday blocks to 35 percent of target utilization.

- Sponsors. Two anchor sponsors with LOIs, minimum guarantees, and outcome fee schedules.

- Lease. Turnover band or stepped rent, landlord contribution, and break options tied to seasons.

- Fit out. Kit of parts drawings, device neutral bays, power and cooling schedule, acoustic plan.

- Operations. Safety and consent playbooks, staff training path, accessibility plan.

- Financial model. Sensitivity to occupancy and sponsorship. Clear cash control during ramp and content refresh schedule.

- Compliance. Data protection, filming consent, safeguarding, and IP policies for AI assisted content.

10) Rollout plan with targets and early KPIs

First 90 days. Launch Schools and Skills blocks. Switch on yield management. Release a 50 seat Creator Pro cohort. Convert one brand to outcome based lab. Package two corporate off sites per month. Assemble a six bay pop up kit. Track occupancy by zone and daypart, sponsor mix, institutional hours, Pro conversion, pop up contribution, and device downtime.

12 months. One urban pilot to positive unit economics. Lock two anchors and one education partner.

24 to 36 months. Expand to five to ten cities. Add AI user matching and a cloud content layer for at home follow ons.

This sequence matches the phased roadmap and growth design in the investment memorandum, including company owned flagships and a franchising or white label path once the playbooks harden.

11) Decision criteria and go, no go

Use this short list to frame the investment vote.

- Catchment supports 60 percent peak occupancy by month six based on pre sold weekday blocks and sponsor activation.

- Lease terms include landlord contribution, turnover or stepped rent, and a season based break option.

- Two sponsors signed, with minimum guarantees plus outcome fees. One education partner contracted for term blocks.

- Hardware leased, device neutral bays specified, 15 percent spares, and vendor SLAs in place.

- Safety, consent, safeguarding, and accessibility policy stack approved. DPIAs completed where required.

- Sensitivity shows breakeven within 18 to 24 months in base to upside, with contingency actions defined for a sponsor delay or a 10 percent occupancy shortfall.

Conclusion

Immersive hubs are a time bound, high growth play that rides the utility phase of XR and the appetite for social, tech enabled experiences. The model is viable when you design for diversified revenue, modular fit out, and weekday contracts. You can protect downside with lease and sponsor structures, and you can grow margin with outcome based labs, institutional blocks, and Pro memberships. The prize is not only unit EBITDA, but a defensible network that serves as the entry point to the immersive internet for users, brands, and cities. The plan and numbers in your analysis and memorandum support a disciplined go, subject to the decision criteria above.

Appendices

Motivation and Alternative outline business case

A few years ago, I walked through a half-empty shopping mall, and it felt like a ghost town—a monument to a bygone era of retail. At the same time, I was spending more and more time with a VR headset, feeling the strange mix of wonder and isolation that comes with it. The digital world was vibrant, but lonely. The physical world was social, but sterile. It struck me that the solution to one problem might just be the solution to the other.

What if we could reimagine these underused spaces as vibrant hubs for the next wave of technology? Not just another cyber café, a concept whose limited lifespan we all remember, but something entirely new. This is the investment thesis for what I call the New Immersive Shared Tech Spaces: a global network of adaptive, AI-powered hubs that serve as the primary physical gateway to the immersive internet.

This isn’t a long-term real estate play in the traditional sense. It’s a strategic, time-bound venture designed to capitalize on a critical window in the adoption curve of immersive technologies. It’s a frontier business opportunity.

The ‘Why Now?’ – A Perfect Storm of Opportunity

Any savvy investor knows timing is everything. The thesis for these new spaces rests on a powerful convergence of market forces:

- The Experience Economy: Consumers, particularly Gen Z and Millennials, consistently prioritize spending on experiences over goods. The global market for these experiences is projected to surge past $15 trillion by 2030.

- The XR Market is Maturing: The Extended Reality (XR) market is shifting from novelty to utility, projected to grow from around $7.6 billion in 2025 to over $44 billion by 2030. While home adoption of devices like the Apple Vision Pro is finding its footing in enterprise, it remains slow for consumers, highlighting the need for “try-before-you-buy” venues.

- The Real Estate Crisis: Commercial real estate is crying out for a new purpose. These hubs offer a high-footfall, experience-based anchor tenant that can revitalize a property and increase dwell time. Landlords are becoming more open to experiential anchors on flexible leases.

- The Creator Economy Boom: A new class of digital creators needs access to professional-grade tools and studios, a market already valued at over $100 billion.

This isn’t about competing with home entertainment. It’s about offering what the home

can’t: collective immersion, professional-grade tools, and a powerful sense of community.

Learning from the Ghosts of Cyber Cafés

The immediate question is obvious: “Haven’t we seen this movie before?” The cyber café rose and fell on the tide of personal internet access. But this new model is built on a fundamentally different, more resilient foundation.

- It’s Not About Access, It’s About Experience: Access to tech is now abundant on personal devices. The value must come from immersion and community. Think less about checking email and more about co-creating an AI-augmented short film or attending a holographic concert.

- Diversified Revenue Is the Bedrock: These hubs are designed from the ground up with a stacked revenue model: hourly fees, monthly memberships, brand sponsorships, studio hire, event ticketing, and of course, food and beverages.

- Designed for Change: Technology becomes obsolete quickly. These spaces are not meant to last forever. They operate on 3–5 year cycles that match tech maturity curves, with modular designs that can be reconfigured for new uses—from esports to education labs—or transformed into something else entirely after peak use.

- Community as the Ultimate Moat: You can replicate hardware, but you can’t easily replicate a loyal community. By anchoring spaces in local culture—anime VR in Tokyo, Nollywood heritage experiences in Lagos—and running leagues, workshops, and events, these hubs build a loyalty that technology alone cannot.

A Glimpse Inside: The New Archetypes of Shared Space

To make this tangible, imagine a typology of spaces you could walk into:

- The Creative Testbed: A studio for the next generation of creators. Here, you can rent a space by the hour, complete with AI-enhanced production tools and on-demand robotics personnel, to film immersive portraits or AI-augmented shorts.

- The Performance Hub: The 21st-century arena. It hosts immersive concerts with holographic performers, esports tournaments with live streaming rigs, and VIP lounges for hybrid physical-virtual events.

- The Tourism Lab: A place to “try before you fly”. Partnering with tourism boards and airlines, these labs offer location-based VR heritage tours and immersive demos of travel experiences.

- The Co-Play Café: The social heart of the ecosystem, blending console lounges with streaming booths and nightclub-style immersive events for global socialisation.

These aren’t just separate ideas; they are zones within a flexible, hybrid model that can be tailored to local demand.

The Investor’s View: Beyond the Box Office

A single 5,000 sq. ft. location carries a total CapEx of around $300K-$600K for fit-out and hardware. With a multi-stream revenue model, break-even is projected within 18-30 months.

But the real genius of this model lies in the overlooked opportunities that turn a venue into a platform.

- Monetizing Data: The “Immersive Insights” Division. The hub is more than a space; it’s a live sensor network for human-tech interaction. By packaging anonymized, aggregated data on user behavior, hardware usage, and content preferences (with explicit user consent), we can create a high-margin B2B insights division. This provides premium R&D data to tech brands and content creators, shifting the business from a pure service model to a service-and-data model.

- Franchising: “Immersive-as-a-Service” (ImaaS). The most valuable asset isn’t the physical location; it’s the operational playbook. We can package the entire operating system—tech specs, AI software, training manuals, and brand guidelines—and sell it as a white-label or franchise model. This is the key to massive scalability without proportional capital outlay.

- The B2B Goldmine: The Corporate Immersion Accelerator. Beyond casual users, there is a deep market for niche B2B services. We can offer packaged corporate services: using VR for AI-powered recruitment assessments, facilitating C-suite strategy sessions where executives can visualize new factory layouts, or helping financial firms interact with complex data in 3D. These B2B contracts command premium day rates and fill the hubs during off-peak hours.

The Road to a Global Network

The implementation is designed to be methodical, de-risking the venture at each stage.

- Phase 1 (First 12 Months): Launch a single pilot location in a Tier 1 city like London or Seoul. The goal is to validate the business model, collect user data, and secure anchor sponsors.

- Phase 2 (Years 2-3): Secure Series A funding to scale to 5-10 cities. We would begin the franchising program and deploy proprietary AI for user matching and space management.

- Phase 3 (Years 4-5): Expand the network to 20+ locations globally, evolving into a hybrid physical-digital platform where the community persists beyond the physical visit. The ultimate goal is an exit via strategic acquisition or IPO.

This is more than a business plan; it’s a vision for revitalizing our urban landscapes. It’s about building the crucial “transitionary infrastructure” that bridges the gap between nascent technology and mainstream adoption. By converting marketing spend into place-based revenue and creating a community moat, we can build a profitable, scalable, and culturally relevant network that defines the next era of human interaction.

{kind=link}

{kind=link}

{kind=link}

{kind=link}