Preamble

Most pickle businesses start with the product and stop there. They make jars, try to get on shelves, and compete in a category where heritage brands, price pressure, and retail gatekeepers already dominate. Just Pickles works best when it does the opposite. It starts with the category, the customer journey, and the digital ecosystem, then builds products, content, subscriptions, and brand extensions around that foundation. FYI: USA and Europe market size : Greater than $5 billion

The core insight across the attached documents is simple. The strongest opportunity is not to launch another commodity pickle company. It is to build an online-first hybrid pickle platform, one that sells premium pickled products, sampler boxes, and brine-based extensions while also becoming a trusted destination for recipes, education, global pickle discovery, and taste-led recommendation. That positioning gives Just Pickles more room to differentiate, build loyalty, and expand internationally than a jar-only business ever could.

What makes the idea commercially interesting is that the market already validates each piece of the model. Premium chilled pickles, brine products, content-led food brands, gifting formats, and food discovery subscriptions all exist in adjacent forms. The gap is that few players combine them into one coherent operating system. Just Pickles can fill that gap if it stays disciplined about launch scope, margin, food safety, and channel sequencing.

As usual supporting documents Just Pickles

| Name | Short description |

| version of Just Pickles.docx | Recommends an online-first hybrid model for Just Pickles, with phased growth from e-commerce, content, subscriptions, and pop-ups into a tasting bar, and only later a deli if demand proves out. It also defines the core business model across products, brine, media, education, and community. |

| analysis.docx | Provides an executive view of expansion beyond the UK, USA, and EU, including priority markets such as Canada, Australia, Japan, Singapore, and the Gulf. It also includes stakeholder analysis, people-process-tech segmentation, SWOT, PESTEL, and international growth recommendations. |

| Executive view.docx | Reviews the pickle market across the USA, UK, and EU, and explains where Just Pickles fits competitively. It covers market attractiveness, competitor analysis, category trends, and a recommended entry ranking by region. |

| Generic business plan framework.docx | Sets out a modular business plan framework for multiple pickle-related business segments, including DTC, subscriptions, brine products, wholesale, foodservice, tasting bar, education, and private label. It also suggests phased rollout paths and segment combinations. |

| Software Requirements Specification.docx | Defines the SRS for the Just Pickles website and mobile app, including ecommerce, subscriptions, recipes, content hub, global pickle discovery, community features, AI-assisted recommendations, admin tools, integrations, and phased MVP planning. |

The business concept

Just Pickles should be understood as a four-layer business rather than a single packaged food line.

The first layer is the core product business. This includes premium pickled cucumbers and a wider range of pickled vegetables such as onions, carrots, okra, beets, radish, peppers, garlic, and rotating seasonal or global variants. These products give the brand its commercial base and allow it to establish hero SKUs with repeat purchase potential.

The second layer is the brine business. This is one of the strongest ideas in the concept. Instead of treating pickle juice as waste or a side note, Just Pickles can turn it into a product family that includes cooking brines, marinades, cocktail and mocktail mixers, spicy brine shots, and re-pickle kits. This creates differentiation, raises average order value, and supports cross-sell. It also gives the brand a strong sustainability and utility story, because it teaches customers how to get more value from the full pickle ecosystem.

The third layer is the media and education business. The website should not behave like a static store. It should function as a search-friendly content engine that helps people learn about pickling, fermentation, preservation, safety, recipes, ingredient traditions, and practical uses for both pickles and brine. This content supports discovery, trust, SEO, and long-term brand authority.

The fourth layer is the curator and community layer. This includes global pickle discovery, taste profiles, world pickle maps, featured creators, recipe sharing, curated social content, and themed discovery boxes. That layer matters because it turns Just Pickles from a packaged goods seller into a category builder.

Put simply, Just Pickles is strongest when framed as a pickle ecosystem brand, not just a pickle jar brand.

Why this market is worth entering

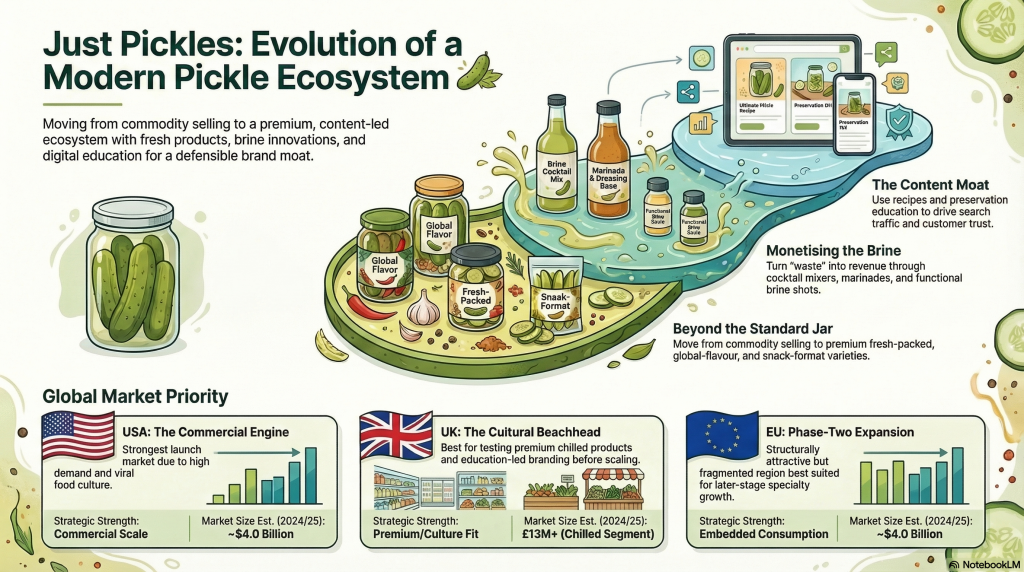

The attached market analysis makes clear that the pickle category is durable and commercially real, but it is not a blank space. Growth exists, yet most of the value does not sit in trying to underprice mainstream brands. The better opportunity is to target premium subsegments, chilled and fresh-feeling products, global flavor exploration, and new use cases such as brine-based adjacencies.

The USA stands out as the strongest first market. It combines category familiarity, scale, viral food culture, and enough whitespace for a modern challenger to win on discovery, refrigerated positioning, sampler packs, gifting, and brine products. Incumbents still dominate mainstream volume, but newer brands have shown that freshness, format innovation, and stronger brand culture can shift consumer attention. For Just Pickles, that means the U.S. offers the clearest commercial base for a digitally led launch.

The UK is smaller, but strategically attractive for premium chilled pickles, fermentation-adjacent storytelling, brine-led innovation, and education-led branding. It is a good market for a culture-rich concept, especially one that wants to combine commerce with workshops, recipes, and curated pickle discovery. The main constraint is scale. On its own, the UK is a strong beachhead, but not the largest long-term revenue engine unless paired with later expansion.

The EU offers broad structural demand because pickled products already have deep roots in everyday consumption. But it is fragmented by language, logistics, and market-specific competitive conditions. That makes it attractive as a phase-two or phase-three expansion region rather than the ideal place to start. Just Pickles would need a premium, curated, or educational angle to avoid being lost among heritage producers.

Outside the UK, USA, and EU, the analysis points to Canada, Australia, Japan, Singapore, and the UAE as the strongest next-wave markets. These markets combine premium imported-food potential, cultural acceptance of preserved foods, or digital retail maturity. The lesson is important. Expansion should not mean trying to be everywhere. It should mean moving into markets where the model has natural support and lower translation friction.

Competitor review and what it means

The competitor landscape tells an important story. In the USA, the mass market is controlled by large, well-known brands that win on familiarity, distribution, and price. A startup should not try to beat them at their own game. The real opportunity lies in what those players are not optimized to do well, namely category storytelling, premium discovery, content-driven commerce, brine innovation, and taste-led recommendation.

In the UK, the most relevant signals come from modern premium chilled brands and brine-led innovators. Together they prove that consumers will pay for a branded pickle experience beyond supermarket basics. This gives Just Pickles room to occupy the space above standard retail pickles and alongside culinary exploration.

In Europe, heritage brands remain strong. That means direct competition on generic gherkins would be a weak move. Just Pickles would need to enter through differentiation, such as global pickle curation, limited runs, hospitality tie-ins, online discovery boxes, or culturally rich educational content.

The broader takeaway is that most incumbents are structured as packaged goods companies. Just Pickles should position itself as a category platform. That is its best chance to build something harder to copy.

The digital platform strategy

The SRS is one of the most important parts of the concept because it shows how the business becomes scalable. The Just Pickles platform is designed as more than an ecommerce storefront. It has four pillars: shop, learn, discover, and community. This is exactly the right architecture for the business model described in the strategy documents.

The shop layer supports products, brines, subscriptions, samplers, gifting, and reorder behavior. That handles direct revenue. The learn layer supports guides, preservation content, FAQs, ingredient pages, and product-linked education. That handles trust and traffic. The discover layer supports the pickle profile, search, filters, region pages, and world pickle exploration. That handles differentiation and conversion. The community layer supports curated content, reviews, saved lists, and future creator or user engagement. That handles retention and brand depth.

The SRS also gets the sequencing right. It recommends website first, then mobile app later. That matters because the website should be the primary SEO, content, and conversion engine in the early stage. The app becomes more useful once repeat purchase, subscription management, saved preferences, and deeper engagement patterns are proven. Launching a full app too early would add cost before the core commercial model is validated.

Several digital features stand out as strategically strong. One is the Pickle Profile, which captures taste preferences such as sourness, heat, sweetness, crunch, and funkiness, then uses them to recommend products and recipes. Another is the World of Pickles feature, which turns the platform into a destination for global pickle discovery. Another is the recipe and brine ecosystem logic, which expands product usage rather than limiting it to sandwiches and sides. Together these features help Just Pickles become a food discovery platform rather than a simple grocery cart.

The AI layer should remain supportive, not central. The documents are correct to place AI in roles such as demand forecasting, catalog tagging, recommendation logic, review summarization, and customer support triage. AI should not drive health claims, unsupervised regulatory content, or anything that bypasses food safety review. That keeps the platform useful without creating avoidable governance or trust problems.

Why subscriptions and sampler boxes matter

Sampler packs and subscriptions are not side ideas. They are central to the Just Pickles model.

Pickles are highly varied in taste, texture, acidity, sweetness, crunch, spice, and cultural style. That makes them hard to choose online if the user only sees a product photo and name. Samplers solve that problem. They reduce buyer uncertainty, support gifting, improve discovery, and create a bridge from curiosity to repeat purchase.

Subscriptions matter for a different reason. They introduce recurring revenue and provide a structure for curation. A pickle of the month, world pickle club, seasonal flavor flight, or guided sour to spicy discovery series can all turn one-time buyers into long-term customers. That said, the documents rightly warn that not everyone who likes pickles will subscribe to premium imported or experimental formats. Subscription must be tested, not assumed. It works best once the business already understands its hero SKUs and customer segments.

A good model is to start with one sampler product and one subscription offer, then expand only if retention and upsell data justify it.

Why brine products are more than a gimmick

Brine products could easily be dismissed as novelty, but the business case suggests otherwise. They serve several roles at once.

They improve margin by creating add-on products from a category asset that many brands ignore. They deepen brand identity because they make Just Pickles feel inventive rather than conventional. They create content opportunities through recipes, cocktails, marinades, and reuse guides. They also align well with sustainability language because they encourage fuller product utilization rather than waste.

The best approach is to keep early brine SKUs focused and useful. Original cooking brine and a spicy cocktail or marinade brine are sensible starting points. That gives the brand room to test cross-sell and reorder patterns before expanding into a larger brine line.

Critique of the concept

The Just Pickles idea is strong, but it also has clear risks that should not be hidden behind the excitement of the brand concept.

The first critique is breadth. The idea is naturally expansive. It wants jars, brine, content, discovery, subscriptions, global education, physical experiences, community, and maybe later even deli or hospitality extensions. That ambition is part of its appeal, but it also creates a real danger of overbuilding too early. The documents repeatedly point to this. The business will only work if the early version stays narrow and proves demand before layering on more complexity.

The second critique is operational reality. Shipping liquids in glass is hard. Leakage, breakage, packaging cost, and cross-border duties can quietly damage the economics of an otherwise attractive DTC brand. That is why packaging, fulfillment, and hero SKU discipline matter so much.

The third critique is behavioral. People may enjoy pickles, but that does not automatically mean they will subscribe, buy premium tiers repeatedly, or care about global pickle education. Some will. Many will not. The business must distinguish between occasional novelty buyers and customers with real repeat-purchase potential.

The fourth critique is regulatory and category discipline. The concept should avoid overreaching into higher-risk areas too soon, especially products with more demanding food safety requirements. The documents are right to avoid launching with pickled meats. The early product line should stay in categories with clearer operational control.

The fifth critique is channel confusion. A deli, tasting bar, ecommerce business, content platform, and B2B supplier are all different businesses in practice. They can connect over time, but they should not all be treated as day-one activities.

None of these critiques kill the concept. They simply show that the strength of Just Pickles depends on sequencing and restraint.

Risk analysis and mitigation

Several risk groups stand out from the documents.

Strategic risk comes from trying to do too much at once. The mitigation is a phased model. Launch with DTC packaged pickles, one sampler, one subscription, basic content, and a small brine line. Add wholesale, tasting experiences, global expansion, and deeper community features later.

Operational risk comes from packaging, leakage, breakage, quality assurance, and co-packer dependence. The mitigation is to use a tight launch assortment, validate packaging thoroughly, choose production partners carefully, and monitor damage rate as a core KPI.

Regulatory risk comes from labeling, traceability, shelf-life, and any health-adjacent messaging. The mitigation is strong compliance review, conservative claims, and clear governance over both product data and content.

Economic risk comes from excessive SKU count, expensive acquisition, and weak reorder behavior. The mitigation is to focus on hero products, bundles, and attach-rate friendly adjacencies such as brine, rather than launching a sprawling catalog.

Technology risk comes from building too much software too soon. The mitigation is to make the website the core engine, keep AI assistive rather than mission-critical, and phase advanced app and community features after product-market fit.

Market expansion risk comes from assuming that every country with pickles is a good next market. The mitigation is to prioritize countries with proven imported-food demand, premium ecommerce maturity, or low localization friction, starting with markets such as Canada and Australia before broader rollout.

Recommended execution path

The attached documents converge on a sensible launch model.

Phase one should focus on an online-first hybrid business. That means ecommerce, subscriptions, sampler packs, content, recipe pages, and selective physical trial through pop-ups, festivals, food halls, or tasting events. No full deli. No broad retail rollout. No excessive SKU spread.

The initial assortment should stay disciplined. Six to ten hero SKUs, two brine products, one sampler box, one subscription offer, and a strong set of content pages is enough for launch. This gives the brand enough variety to feel interesting without turning operations into chaos.

The website should launch first with core ecommerce, content hub, recipes, pickle profile, subscriptions, and admin analytics. The mobile app should come later once the team has evidence that people reorder often enough to justify an app-based loyalty layer.

Geographically, the cleanest starting choice is the USA if the goal is commercial scale. The UK is also viable if the goal is premium positioning and content-led brand development. Europe should come later. Outside those regions, Canada and Australia look like the strongest early export tests.

Execution criteria

A strong execution plan needs clear gates. Just Pickles should move forward only if these criteria are met:

The first is product clarity. The launch range must be tight, distinctive, and operationally manageable. If the business cannot explain why each opening SKU exists, there are too many.

The second is margin viability. Packaging, fulfillment, and breakage economics must work for direct orders before scaling traffic or adding countries.

The third is repeat purchase evidence. The business needs proof that at least a few hero products and one bundle or sampler drive genuine reorders.

The fourth is content usefulness. The education and recipe layer must drive traffic, engagement, or conversion. If the content hub does not help discovery or trust, it is not yet earning its keep.

The fifth is subscription performance. Subscription should be measured through retention, churn, and gift-to-repeat conversion, not launched on faith.

The sixth is brine attach rate. Brine should prove that it increases average order value or repeat behavior, not just create catalog clutter.

The seventh is readiness for physical touchpoints. Pop-ups and tasting events should show real conversion or footfall quality before any permanent site is considered.

The eighth is expansion readiness. New geographies should only be opened when unit economics, packaging performance, compliance, and localized demand signals are clear.

Conclusion

Just Pickles has real potential because it is not trying to win as a cheaper pickle brand. It is trying to build a better category model. The strongest version of the business combines premium products, sampler logic, brine extensions, education, and digital discovery into one ecosystem. That gives it a stronger moat than a simple jar line and more room to scale across channels and markets.

The concept works best when it respects a simple rule. Be broader in vision than incumbents, but narrower in launch than your imagination wants. That means hero SKUs before endless variety, website before app sprawl, pop-ups before permanent retail, and evidence before expansion. If Just Pickles follows that logic, it can become more than a novelty food brand. It can become the leading digital destination for pickle culture, discovery, and commerce.

Next steps

- Define the phase-one assortment, six to ten hero SKUs, two brine products, one sampler, one subscription.

- Choose the launch market, USA for scale or UK for premium culture-led testing.

- Validate packaging, breakage control, shelf-life, and fulfillment economics.

- Build the website MVP with shop, content hub, recipes, pickle profile, subscriptions, and analytics.

- Create 20 to 30 high-quality educational and recipe pages to support SEO and trust.

- Run pop-ups or tasting events to test flavor preference, sampler uptake, and in-person conversion.

- Measure repeat purchase, damage rate, AOV, subscription retention, and brine attach rate before broadening the model.

- Only after those signals are positive, test wholesale, physical retail, or export expansion.

Market analysis

Here is a breakdown of the market sizes for the USA, UK, and Europe based on the available reports.

United States Pickles Market

The US market shows a notable split in data, with one estimate being significantly higher, likely due to a broader market definition.

| Source | Market Size (2024/2025) | Forecast (2033/2034) | CAGR | Notes |

| IMARC Group | USD 3.2 Billion (2025) | USD 4.0 Billion (2034) | 2.57% | This is a highly credible estimate from a major research firm and likely represents the most widely referenced figure for the total US market. |

| Deep Market Insights | USD 576.87 Million (2024) | USD 803.77 Million (2033) | 3.69% | This significantly lower figure suggests the report has a more narrow scope, possibly focusing only on specific pickle types like cucumber pickles, excluding others. |

| Market Research Intellect | USD 9.16 Billion (2025) | USD 18.03 Billion (2033) | 8.83% | This extremely high value and growth rate likely points to a very broad definition of the market, possibly including all packaged pickled vegetables, relishes, and other related products. |

- Key Takeaway for the US: The most reliable and commonly cited estimate for the broader US pickles market is approximately $3.2 billion . The market is mature but steady, with growth driven by trends like probiotic foods, global flavors, and clean-label products .

United Kingdom Pickles Market

The UK market estimates are more consistent, though some variance exists.

| Source | Market Size (2024) | Forecast (2033) | CAGR | Notes |

| Deep Market Insights | USD 139.92 Million | USD 198.11 Million | 3.89% | This likely represents a more conservative estimate of the core pickle market. |

| Consegic Business Intelligence | USD 325 Million | USD 550 Million | 6.05% | This higher figure suggests a broader scope, possibly including chutneys, relishes, and other pickled condiments that are popular in the UK. |

| 6Wresearch | No specific 2024 value provided | Not specified | 4.93%-6.60% (2025-2029) | The report confirms a mature market with growth driven by artisanal and gourmet products . |

- Key Takeaway for the UK: The UK market is well-established and is being energized by a surge in demand for artisanal, gourmet, and globally-inspired pickles . Depending on the product definition, the market size ranges from $140 million to $325 million.

🇪🇺 Europe Pickles Market

The European market represents a large, diverse landscape with strong regional traditions.

| Source | Market Size (2025) | Forecast (2034) | CAGR | Notes |

| IMARC Group | USD 3.4 Billion | USD 4.6 Billion | 3.44% | A highly credible estimate for the total European market. |

| Market Data Forecast | USD 3.41 Billion | USD 4.25 Billion | 2.48% | A very similar estimate to IMARC’s, adding confidence to the overall market size. |

| Deep Market Insights | USD 614.71 Million (2024) | USD 867.99 Million (2033) | 3.91% | This figure is dramatically lower and, like its US counterpart, is likely focused on a much narrower product segment, possibly just cucumber pickles. |

- Key Takeaway for Europe: The total European pickles market is valued at approximately $3.4 billion . Growth is fueled by a deep culinary heritage, the rising popularity of fermented foods for gut health, and a trend toward premiumization . The market is fragmented, with strong players in Germany, France, and the UK .

📊 Market Size Comparison Summary

To help you visualize the scale of each market, here is a comparison chart based on the most credible estimates:

- Note: The bar for the UK represents the broader estimate of $325 million , which is likely more comparable to the scope of the US and Europe totals. The $3.2B for the US is from IMARC , and the $3.4B for Europe is from IMARC .

🔍 How to Reconcile Conflicting Numbers

You will encounter different figures when researching markets. This happens because:

- Scope of “Pickles”: Some reports include only cucumber pickles (gherkins, kosher dills), while others include all pickled vegetables (onions, cauliflower, beets, kimchi), relishes, chutneys, and olives.

- Geographic Coverage: “Europe” can be defined as the EU, the wider continent, or a selection of key countries.

- Distribution Channels: Some reports focus on retail sales, while others may include the foodservice industry (restaurants, cafes).

For your business plan, it is best practice to:

- Cite the most credible source (like IMARC Group, a well-known firm).

- Acknowledge the variance by stating, “Estimates for the US market vary between $0.6 billion and $9.2 billion depending on product scope, with a widely cited figure of $3.2 billion representing the core market .”

- Focus on the trends. The exact size matters less than the direction. All reports agree on key trends: premiumization, health & wellness (probiotics), global flavors, and convenience are driving growth across all three regions .

{kind=link}

{kind=link}

{kind=link}

{kind=link}