Strategic Options, Market Size, Business Drivers, and the New Ownership Model Reshaping Who Controls the Factory Floor

This is Part Two of a two-part series. Part One Jeff Bezos $100Billion Bet: THE INDUSTRIAL AI INTELLIGENCE PLATFORM covered the market context, the technology architecture, the stakeholder map, and the economics of the Industrial Intelligence Platform. Part Two turns to a specific and underexamined strategic consequence: what happens when this manufacturing OS collides with the $915 billion global private label industry and the $686 billion contract manufacturing market and what the three ownership positions available to large retailers means in practice.

Most of the coverage around Jeff Bezos’ reported $100 billion Prometheus investment has focused on the obvious angles: reshoring, job displacement, humanoid robots, and the geopolitical race against China’s manufacturing supremacy.

These are real. But they miss the more commercially immediate story.

There is a $915 billion global market growing at 5.9% annually toward $1.6 trillion by 2034 where every major retailer on earth is already competing, already exposed, and almost entirely dependent on a contract manufacturing base they do not control, cannot fully see into, and cannot rapidly reconfigure. That market is private label. And the Prometheus investment, if deployed coherently, is a direct play into the production layer that sits underneath every Kirkland Signature, Great Value, Amazon Basics, and own-brand product line on the planet.[1][2]

The question is not whether the Manufacturing OS changes private label economics. It will. The question is which position large retailers, contract manufacturers, and the Prometheus entity itself should take — and what the game theory looks like across a market producing 68.7 billion units a year in the US alone.[3]

The Market Nobody Compares Correctly

The instinct when reading “$100 billion investment” next to “$282.8 billion US private label market” is to frame it as a size comparison. It is not. That framing is built on a category error.[1]

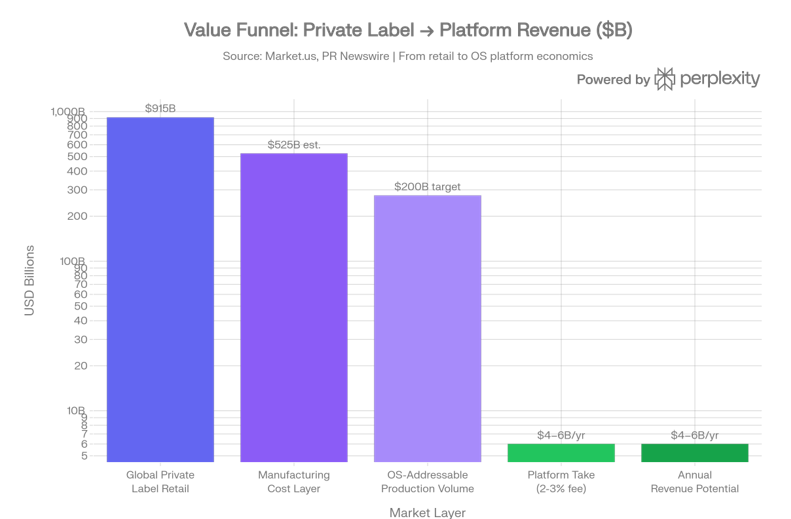

The $282.8 billion figure is the retail value of private label products the price consumers pay at the shelf. The figure that matters for Prometheus is the manufacturing cost base that produces those goods: approximately 30–60% of retail value, putting the true US own-label production economy at $85–$170 billion. Against that number, $100 billion is not a wedge into the market. It is near parity with the entire US production cost base.[3]

Globally, the $915 billion private label retail market has a manufacturing cost layer of roughly $275–$550 billion. Against that, $100 billion represents 18–36% of the production economy that Prometheus can structurally disrupt a genuinely dominant entry position if deployed with discipline.[3]

But the structurally more important comparison is the $686 billion global contract manufacturing market (2025), growing to $969 billion by 2030. This is the industry that produces own-label goods the anonymous factories behind every retailer’s brand. Prometheus does not need to own all of it. It needs to own the operating system that runs on top of it.[3]

The value funnel above illustrates the layering: from $915 billion in retail value, through the manufacturing cost base, down to the OS-addressable production volume, and finally to the platform economics a $4–6 billion annual recurring revenue business running on a 2–3% take rate across $200 billion of instrumented production.[1][3]

Why Private Label Is the Right Entry Sector

Private label is not just growing it is accelerating structurally. In 2025, US store brand unit sales reached a record 68.7 billion units, growing nearly three times faster than national brands, while national brand volumes declined 0.6%. In Europe, own brand now holds 42% value share across EU6 supermarkets. Walmart alone operates 21 private brands each exceeding $1 billion in annual sales, with five exceeding $5 billion.[1]

This is not a trade-down story driven by recession. It is a structural shift toward retailer-controlled brand architecture, driven by three forces that compound together:[2]

- Margin logic. Own label consistently earns higher margins than equivalent branded resale. Costco explicitly states that Kirkland Signature products “generally carry higher margins than national brands.” Walmart’s five-plus-billion-dollar private brands are a multi-year, intentional margin strategy, not an opportunistic one.

- Trust shift. Consumers no longer equate private label with compromise. Circana’s 2025 data shows growth is now tied to quality, sustainability, premiumisation, and retailer trust — not just price. The category has graduated.

- Data advantage. Marketplaces and large-format retailers hold something contract manufacturers do not: demand intelligence. They see what sells, what doesn’t, what price point converts, what gap exists. Private label is the direct monetisation of that data advantage through product ownership.

The combination high volume, accelerating margins, growing trust, retailer-controlled data makes private label the most logical starting point for any Manufacturing OS that wants to prove its economics quickly and replicate them at scale.[4]

The Prometheus Thesis Applied to Own-Label Production

Project Prometheus is, at its core, a simulation and physical-intelligence platform: systems that can predict how materials behave, how production lines will perform, and how product designs will hold up all digitally, before a single unit is physically produced.[5]

Applied to private label manufacturing, this changes the production economics across five vectors that compound into a decisive structural advantage:[1]

1. Design compression. An own-brand product brief today takes 12–18 months to go from specification to shelf, largely because physical prototyping, supplier qualification, and trial production runs consume the cycle. Simulation-first validation testing formulations, packaging tolerances, manufacturing parameters, and yield characteristics digitally before any physical commitment — compresses this to weeks. For a retailer launching 50 new own-label SKUs per year, this is not marginal improvement. It is a capital weapon.

2. Just-in-time private label. The traditional own-label model requires large forward-buy commitments from contract manufacturers. Digital twins and AI-driven scheduling enable a fundamentally different posture: responsive, demand-signal-driven production that releases working capital currently trapped in pre-built inventory. The OS turns the factory into a demand-following system rather than a forecast-driven one.

3. Multi-SKU flexibility. Seasonal variants, regional formulations, premium-tier extensions — these are all currently expensive because line changeovers at CMO facilities are slow, under-instrumented, and poorly planned. An OS that governs scheduling, sequence optimisation, and changeover management at the plant level turns line reconfiguration from a margin cost into a margin opportunity.

4. Quality at the brief stage. Own-label quality failures land directly on the retailer’s brand — there is no supplier name on the package to absorb the blame. Physics-informed simulation that catches specification failures before physical production is not just an efficiency tool; it is a brand protection instrument and a legal liability management system.[6]

5. Cost capture upstream. Today, manufacturing efficiency gains accrue to the CMO. The OS changes this. When the retailer or OS entity owns the intelligence layer running on top of the factory, it can capture efficiency rent through platform fees, shared savings arrangements, or direct production margin without owning the physical plant.[5]

Three Strategic Positions: The Ownership Geometry

The Prometheus investment does not create one strategic option. It creates three distinct positions, with fundamentally different capital requirements, risk profiles, and long-term moat structures. Large retailers and the Prometheus entity itself face a choice architecture, and the right answer depends on which stakeholder you are.

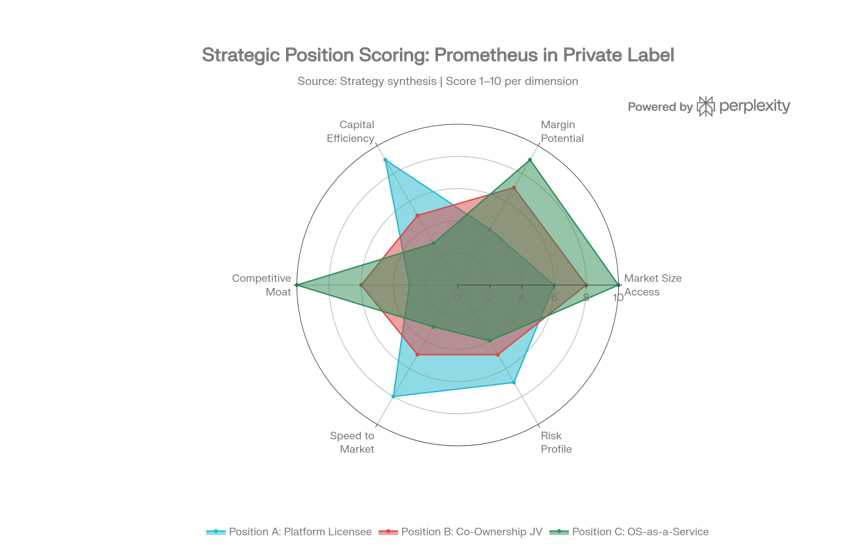

The radar chart above scores each position across six dimensions: market access, margin potential, capital efficiency, competitive moat, speed to market, and risk profile. Position C the OS-as-a-Service contract manufacturing model scores highest on moat and margin but lowest on speed and capital efficiency. Position A scores highest on speed and capital efficiency but builds the weakest long-term moat. The right choice depends on time horizon and risk appetite.[1]

Position A — The Platform Licensee (Hybrid Manufacturer)

The model: The retailer does not own any factory. Instead, it licenses or co-invests in a Manufacturing OS Prometheus-adjacent that runs on top of its existing contract manufacturing base. The CMO operates the plant. The OS, owned or governed by the retailer, runs across it.

What the retailer captures:

- Scheduling transparency and JIT triggers across the CMO network

- Simulation-validated formulation and specification data

- Quality governance audit trails that reduce brand liability exposure

- Predictive cost modelling against raw material and energy price signals

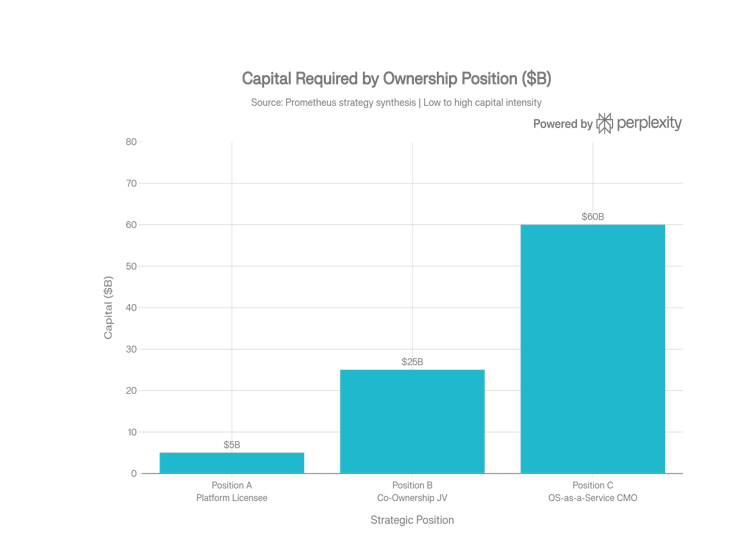

Capital requirement: Low to moderate ($5–10 billion for a Walmart-scale deployment across 20–30 key CMO relationships)

Moat: Weak to moderate. The OS creates informational advantage and switching costs on both sides, but the retailer does not own the production data flywheel. A competitor can license the same OS.

Best fit for: Retailers who want the efficiency gains without manufacturing complexity. This is the right first position for any retailer that has never had OT integration experience. It is the entry point, not the endgame.[1]

Position B — The Co-Ownership Model (Joint Manufacturing Venture)

The model: A large retailer Walmart, Amazon, Costco co-owns a purpose-built AI-native manufacturing facility alongside a Prometheus-model entity. The retailer brings demand data, brand specifications, compliance architecture, and distribution. The OS entity brings capital equipment, plant operations, AI simulation, digital twin infrastructure, and robotics orchestration.

What both parties capture:

- Shared cost savings from throughput improvement and waste reduction

- Flexible capacity that can absorb own-label demand swings without forward-buy commitments

- Third-party contract manufacturing revenue from excess capacity a new P&L line that does not cannibalise the core retail business

Capital requirement: Significant ($20–30 billion at scale, but staged across 5–10 pilot facilities before full portfolio commitment)

Moat: Strong. Shared production data creates a proprietary dataset that neither party can fully replicate independently. The JV structure also creates political protection in reshoring markets — domestic job creation with a credible industrial narrative.[1]

Best fit for: Retailers with strategic intent to enter manufacturing economics without full operational ownership. This is the model that converts a large retailer from a brand owner into a partial infrastructure owner — a genuinely new category of industrial actor.[7]

Position C — The Contract Manufacturing Entry (OS as a Service)

The model: This is the most structurally ambitious option, and the one most consistent with the full Prometheus investment thesis. The OS entity Bezos or a Prometheus-adjacent vehicle builds AI-native factories, proves the production model using its own private label output (Amazon Basics being the most obvious proof-of-concept vehicle), then opens those factories as contract manufacturing-as-a-service for any retailer’s own-brand portfolio.

What the OS entity monetises:

- Production fees structured like SaaS subscriptions per SKU, per unit run, per capacity block

- Simulation-as-a-service: design validation and formulation testing before physical production

- Data products: raw material optimisation models, yield prediction, failure forecasting, and scheduling intelligence sold back to the retailer

- Platform licensing: the OS stack itself, licensed to CMOs who want the certification and premium positioning that comes with it

The flywheel logic: Every plant instrumented adds to the training dataset. Every SKU validated through simulation improves the surrogate models. Every quality event logged tightens the defect prediction algorithms. The OS gets smarter with scale, and scale becomes defensible because the data moat is not replicable from scratch.[5]

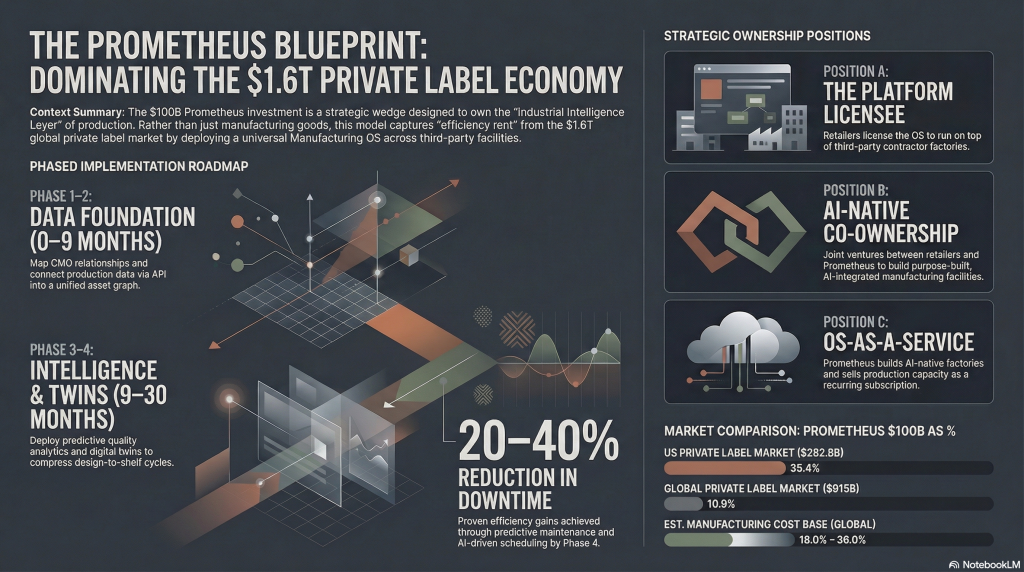

Capital requirement: Very high ($50–70 billion to build, acquire, and instrument the 40–80 manufacturing facilities needed to prove the model across key categories). But your attached documents are explicit: this is “the highest capital requirement, but the strongest structural moat once operational”.[1]

Moat: Maximum. This is the Amazon Web Services model applied to physical manufacturing — own the infrastructure, sell access to it, and earn platform economics on every unit produced through the network.[5]

Understanding the strategic logic requires holding the full picture not just the upside.

Strengths

The structural advantages are real and compounding. Retailers already own the three assets that matter most: the brand, the customer relationship, and the demand data. The OS does not create these assets it makes them actionable upstream, into the production layer where they have historically had no leverage. Own label is already growing at three times the rate of national brands, which means the volume justification for OS investment grows automatically. The Manufacturing AI market itself is on a trajectory from $5.3 billion in 2024 to $47.9 billion by 2030 a structural tailwind, not a bet on a new category. And critically, there is still no dominant non-Chinese industrial AI operating system. The window for a new entrant to define the platform standards is open now.[1][4][5]

Weaknesses

Most large retailers have zero operational technology integration experience. They have never connected a data pipeline to a PLC, never governed an asset graph across a contract manufacturer’s plant floor, never managed the IT/OT security boundary in a brownfield factory. This is not a capability that can be acquired quickly it has to be built or bought through talent and acquisitions. CMO data quality is also a structural problem. Most contract manufacturers operating in the private label supply chain run partially documented plants with inconsistent sensor coverage and fragmented data histories. The asset graph that underpins every higher-level AI capability has to be constructed from poor raw material. And the Siemens-NVIDIA industrial OS partnership announced January 2026 is building the same capability from the inside, with decades of incumbent customer relationships that Prometheus cannot replicate quickly.[4][5][6]

Opportunities

The private label market’s trajectory to $1.6 trillion by 2034 means OS-enabled cost reduction compounds at scale for every year of early adoption. The contract manufacturing market growing toward $969 billion by 2030 creates the external monetisation surface for Position C. Simulation-first new product development compresses own-label innovation cycles from 18 months to weeks a competitive advantage that national brands, operating on traditional physical development timelines, cannot easily match. And the political environment reshoring mandates, tariff volatility, onshoring incentives actively favours domestic AI-native manufacturing capacity as a strategic hedge against Asia-dependent CMO networks.[3][7][1]

Threats

CMO pushback remains the most immediate tactical friction. Third-party manufacturers resist for three rational reasons: the OS exposes their margin and inefficiency structures, reduces their switching leverage, and transfers the capital burden of instrumentation onto them. This resistance is manageable shared savings arrangements, federated data architecture, and volume guarantees are the resolution pathways, but it cannot be ignored or dismissed as irrational. It is structurally rational from the CMO’s perspective. Beyond that, a single high-profile safety or quality incident during the AI transition particularly one that escapes into consumer hands carrying a retailer’s own-brand label is a brand catastrophe with no external manufacturer to absorb the liability. The governance layer is not optional. It is the condition under which any of these positions is commercially viable.[6][1]

The CMO Friction Map and the Path Through It

The third-party manufacturer is simultaneously the essential partner and the primary point of resistance in every deployment scenario. Understanding the friction is prerequisite to navigating it.

| Resistance Type | Root Cause | Resolution |

| Margin exposure | OS makes production inefficiencies visible to the retailer | Frame as joint cost-reduction; CMO retains 40–50% of efficiency gains |

| Data sovereignty | Fear that production data becomes a weapon used against them | Federated architecture — data stays at the plant; only aggregated KPIs flow upstream |

| Capital burden | Instrumentation cost (sensors, edge compute, MES integration) lands on the CMO | Retailer or OS entity funds instrumentation in exchange for long-term supply commitment |

| Competitive exposure | Fear that instrumented data will be shared with competing retailers | Contractual exclusivity clauses — SKU-level production data is ring-fenced |

| Fear of replacement | OS makes CMO more substitutable once its processes are documented | Position OS integration as a quality certification — OS-certified CMOs access preferred supplier tier with volume guarantees |

The key message to every CMO in this market is simple: the OS makes you more competitive, not more replaceable. A contract manufacturer with Prometheus-adjacent OS certification can charge a production premium the same model Machina Labs uses, where AI-native metal forming capability shortens lead times from months to days and commands premium positioning in defence and aerospace procurement.[5]

The CMO that resists instrumentation remains opaque, unverifiable, and increasingly hard to justify to a retailer under margin pressure. The CMO that embraces the OS becomes a certified, data-validated, AI-enhanced production partner harder to replace precisely because the integration runs deep.

The ROI Architecture: Three Horizons

The financial case is not linear. It is a three-horizon model where each phase unlocks the next.

Horizon 1 — 0 to 18 months: Prove the cost case

The entry point is quality and maintenance. Vision-based defect detection on high-volume own-label lines (payback 6–24 months, high confidence). Predictive maintenance on critical CMO assets (payback 6–18 months, high confidence). AI-assisted scheduling to reduce changeover waste and improve line utilisation (12–24 months, medium-high confidence). These use cases require no deep factory ownership — they require sensor access, data connectors, and a governed analytics layer.[4]

Target metrics: 20–40% reduction in unplanned production failures. 6–15% scrap reduction. 15–30% working capital release through JIT scheduling.[7]

Horizon 2 — 18 to 36 months: Expand the intelligence layer

With the data foundation proven, the twin and simulation layer comes online. New own-label SKU development shifts to simulation-first — product twins test formulations, packaging tolerances, and manufacturing parameters before physical commitment. Engineer and operator copilots go live at key CMO facilities. Robot-cell orchestration begins in bounded, validated production environments.[6]

Target metrics: 30–50% reduction in design iteration time. 5–15% capex avoidance through simulation-first validation. 10–20% throughput improvement.[7]

Horizon 3 — 36 months and beyond: Enter the contract manufacturing market

The platform economics confirm. The playbook is replicable. The OS entity now has the data, the proof cases, and the operational credibility to open AI-native manufacturing capacity as a service. Third-party retailers access the platform. The contract manufacturing revenue line opens.[4]

Target economics: 2–3% platform take rate on $200 billion of OS-instrumented production volume = $4–6 billion annually. Strongest long-term moat.[3]

What This Means for the Strategic Landscape

The implications of this model extend well beyond Amazon, Walmart, and Costco. Any retailer that produces own-label products at scale in grocery, household, beauty, home, fashion, or electronics accessories faces a version of the same strategic choice over the next three to five years.

The companies that move first into Position A will not build a permanent advantage the OS is licensable. But they will build operational fluency: data integration experience, CMO partnership architectures, and OT governance capabilities that are genuinely hard to replicate quickly. That fluency is the precondition for moving to Position B and C.

The companies that wait for the technology to mature further are making a category error. The window for early positioning in the data flywheel where every instrumented plant, every quality event logged, every twin model calibrated compounds into a proprietary advantage — is not indefinitely open. Platform moats in industrial systems, like platform moats in software, close as incumbents consolidate.[5]

The Siemens-NVIDIA partnership is already building this from the industrial software side. The Prometheus investment is building it from the capital and acquisition side. The retailers who co-own the intelligence layer rather than merely licensing it from whoever wins the OS race will hold the best position in a $1.6 trillion market where production economics are about to be restructured from the ground up.[7]

The Manufacturing OS play in private label and contract manufacturing is not primarily a technology story. It is an ownership story. It is about who controls the intelligence layer between the retailer’s brand and the factory floor and what that ownership is worth as the market grows toward $1.6 trillion over the next decade.

Bezos’ $100 billion is not 35% of the US private label market. Against the production cost base that actually matters, it is near parity a structural entry position that, if executed with discipline, can define the production layer of modern retail for a generation.

The execution principles have not changed from Part One of this series. Build the data layer before the AI layer. Prove ROI at one line before scaling to the portfolio. Govern every model-driven action before it touches the real factory. Bring the CMOs into the value equation rather than treating them as obstacles.

The primary gap is not ambition. It is delivery readiness.

In manufacturing AI, that has always been the case. The private label market is simply the most commercially immediate place to prove it.[4]

Part One of this series Jeff Bezos $100Billion Bet: THE INDUSTRIAL AI INTELLIGENCE PLATFORMcovering the full market context, technology stack, stakeholder map, and economics of the Industrial Intelligence Platform is available in the previous issue. The supporting document set includes the Industrial Intelligence Vision Document v2, the BRD v2, the Architecture Blueprint v2, the Layer Analysis, and the Success Criteria and Checklists v2, all prepared March 2026.[6][7][8][4]

References

1 How-does-100B-investment-compare-to-private-label-2.docx

2 If-you-look-at-the-attached-document-how-do-you-ap.docx

3 ownbrand.docx

4 how-does-he-leverage-this-in-the-contract-market-3.docx

5 industrial_intelligence_article-2.docx

6 industrial-intelligence-layer-3.docx

7 industrial_intelligence_brd_v2-7.docx

8 industrial_intelligence_vision_document_v2-8.docx

9 industrial_intelligence_architecture_blueprint_v2-6.docx

10 what-are-drivers-to-apply-apply-to-differnt-indus-4.docx

11 Author-Persona-The-Industrial-Intelligence-Strategist-5.docx

{kind=link}

{kind=link}

{kind=link}

{kind=link}