Preamble: The Transit Trilemma

Every city that has ever tried to move large numbers of people quickly has faced the same cruel triangle: speed, cost, and coverage. You can usually pick two. Rail is fast and high-capacity but brutally expensive to build. Surface buses are cheap and flexible but prone to the mercy of traffic. And somewhere in between for decades, largely ignored sits elevated Bus Rapid Transit (BRT): grade-separated, electrically powered, flexibly operated, and priced at a fraction of metro construction costs.

Mexico City has quietly become the world’s most ambitious proving ground for this middle-ground solution. Its Trolebus Elevado programme —beginning with Line 10 in 2022 and expanding with Line 11 in May 2025 represents not just a transit investment but a live engineering experiment that the world’s urban planners, infrastructure investors, and policymakers are beginning to pay serious attention to.

This issue of The Elevated BRT Dispatch takes a deep dive: the engineering case, the financial structure, the global comparators, the investor thesis, a full PESTLE and SWOT analysis, and the hard critiques that boosters often skip. We close with a forward-looking synthesis on where elevated BRT sits in the broader urban mobility stack and which cities, corridors, and capital structures are next.Why Mexico City’s Elevated Trolleybus Is More Than a Transit Project It’s a Global Template for the Infrastructure Decade Ahead

I. What Is Elevated BRT? Engineering Fundamentals

Elevated BRT is, at its core, a bus rapid transit system that operates on a viaduct or elevated guideway physically separated from surface traffic. It combines the civil engineering logic of a light rail viaduct with the operational flexibility of a bus fleet. The key structural elements are:

- A dedicated elevated running way, typically pre-cast concrete box girder or beam-and-slab, supported by columns set in the median or roadside of a major arterial.

- Stations perched on the structure, usually accessed by stairs, ramps, and (in newer designs) elevators and escalators.

- An overhead power supply (for trolleybus-based systems) or depot-based charging (for battery-electric variants), or a hybrid In-Motion Charging (IMC) configuration.

- Articulated or bi-articulated electric buses with right-hand or left-hand platform doors depending on configuration.

What distinguishes elevated BRT from a simple overpass is the system design: off-board fare collection, signal priority at grade transitions, real-time passenger information, and integration with surface transit networks. Done well, it approaches light rail in passenger experience; done poorly, it becomes an expensive, underused eyesore.

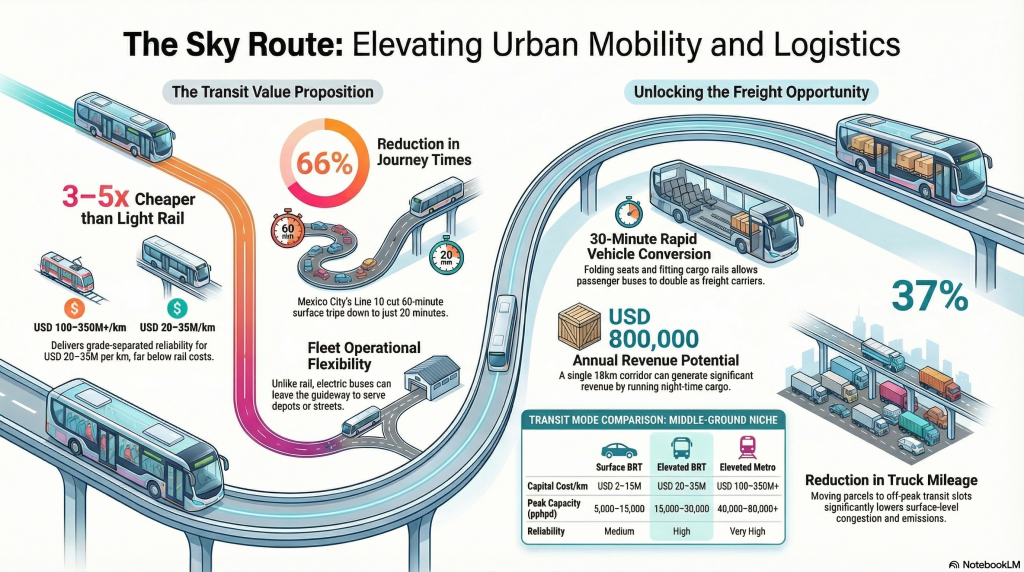

Mexico City’s Line 10 (Eje 8 Sur), the first phase opened in September 2022, runs 7.4 km with 9 stations from Constitución de 1917 (Metro Line 8 interchange) to UACM Casa Libertad, through the densely populated district of Iztapalapa. It operates left-hand traffic on a central elevated guideway, using Yutong ZK5180C articulated trolleybuses with a 100 km battery reserve for off-wire operation. The entire route takes approximately 20 minutes — compared to 60+ minutes on the former surface route.

Line 11 (Elevado Chalco), inaugurated on 18 May 2025, is a 18.5 km corridor — with a 6.7 km elevated section — extending from Constitución de 1917 to the municipality of Chalco in Estado de México. Its total construction cost was approximately 11.3 billion Mexican pesos (roughly EUR 520 million), equating to about EUR 28 million per kilometre. The line is designed for up to 100,000 passengers per day, with a long-term ceiling of 230,000 passengers per day.

| Parameter | Line 10 (Eje 8 Sur) | Line 11 (Elevado Chalco) |

| Opening | September 2022 | May 2025 |

| Total Length | 7.4 km | 18.5 km (6.7 km elevated) |

| Stations | 9 intermediate | 15 stops |

| Journey Time Saving | ~60 min → 20 min | ~2 hrs → 45 min |

| Fleet | 25 Yutong trolleybuses | 108 Yutong articulated trolleybuses |

| Expected Daily Ridership | ~76,000 | Up to 100,000 (design cap: 230,000) |

| Estimated Cost/km | ~USD 27 million | ~EUR 28 million (~USD 31 million) |

| Propulsion | Overhead wire + battery IMC | Overhead wire + 100 km battery reserve |

II. Global Comparators: How Does Elevated BRT Stack Up?

Mexico City is not alone. A handful of cities around the world have attempted various forms of grade-separated BRT. The table below summarises the key benchmarks:

| System | Country | Type | Length | Notable Feature |

| Xiamen BRT | China | Elevated busway | 67 km (multi-line) | China’s first elevated BRT; fully electric; integrates with metro |

| Transjakarta Corridor 13 | Indonesia | Elevated busway | 9.3 km elevated section | 18-24m high viaduct; 24-hour service; accessibility gaps at launch |

| Adelaide O-Bahn | Australia | Guided busway | 12 km | Track-guided; buses fan out onto city streets post-corridor |

| Cambridgeshire Guided Busway | UK | Ground-level guided | 25 km | World’s longest guided busway; connects Cambridge to St Ives |

| Istanbul Metrobüs | Turkey | Grade-separated (median) | 52 km | World’s busiest BRT by pphpd; carries 800,000+ daily |

| Ottawa Transitway | Canada | Segregated busway | 31 km | Backbone since 1983; partly converted to LRT in 2019 |

| Pittsburgh East Busway | USA | Segregated busway | 9.6 km | Former rail ROW; strong ridership model for US cities |

| Mexico City Line 10 & 11 | Mexico | Elevated trolleybus BRT | 7.4 + 18.5 km | World’s only elevated electric trolleybus BRT programme |

Key Observation: Mexico City’s programme is unique in combining true viaduct elevation with overhead electric trolleybus propulsion — a configuration that no other system in the world has deployed at scale. Xiamen uses elevated busways but with depot-charged battery-electric buses. Jakarta’s Corridor 13 is elevated but diesel-based. Mexico City’s IMC trolleybus approach offers continuous charging during operation, lower battery weight penalties, and near-zero tailpipe emissions — making it arguably the most technically advanced elevated BRT in operation globally.

III. PESTLE Analysis: The Macro Environment for Elevated BRT

Political

- Strong enabling factor: Mexico City’s elevated BRT programme benefited from direct political championship under Mayor Claudia Sheinbaum (2018–2024), whose platform explicitly prioritised electric public transport as a climate and equity commitment. Her subsequent rise to the Mexican presidency (October 2024) creates a nationally supportive environment for replication.

- Risk factor: BRT projects globally are vulnerable to political discontinuity. Ottawa’s Transitway was partly dismantled in favour of LRT under a different administration. New mayors often prefer ribbon-cutting on new rail projects over operational improvements to bus systems.

- Global trend: Multilateral development banks (World Bank, IDB, ADB) have increased infrastructure allocations for sustainable urban transport. The C40 Cities Finance Facility actively co-funded the Eje 8 Sur feasibility study with GIZ and Deutsche Gesellschaft für Internationale Zusammenarbeit.

Economic

- Capital cost advantage: Elevated BRT costs in the USD 20–35 million per km range — 3 to 5x cheaper than elevated light rail (USD 70–120 million/km in Latin America) and 8 to 15x cheaper than metro tunnelling (USD 150–350+ million/km in complex urban environments).

- Operating cost structure: Electric trolleybus fleets benefit from lower energy costs than diesel and lower maintenance costs over lifecycle. Total Cost of Ownership (TCO) studies for Mexico City’s Eje 8 Sur, conducted by IDOM and GIZ over a 30-year horizon, identified trolleybus as the most economically feasible option across all alternatives studied.

- Ridership economics: Line 10 targets 76,000 daily boardings; Line 11 targets 100,000. At current Mexico City fare levels (~MXN 7–10 per trip), farebox recovery will not cover capital debt service — as is typical globally for urban transit. The economic case rests on congestion reduction, emissions savings, and agglomeration productivity gains — not farebox revenue.

- Employment: Fleet procurement (Yutong vehicles) has generated supplier linkages, though the lion’s share of vehicle value is captured in China, not Mexico. Local construction, operations, and maintenance are domestically sourced.

Social

- Equity logic: Both Lines 10 and 11 serve Iztapalapa and Chalco — among Mexico City’s most densely populated and economically marginalised districts. Cutting the Chalco commute from 2 hours to 45 minutes delivers an enormous effective wage gain for low-income workers.

- Gentrification risk: Improved transit access can accelerate land value appreciation and displacement of existing low-income residents — a well-documented pattern in BRT corridors globally (e.g., Bogotá’s TransMilenio corridor).

- Accessibility gaps: Jakarta’s Corridor 13 serves as a cautionary tale — opened with 117-step station access and minimal disabled infrastructure. Mexico City’s newer lines have incorporated lifts and ramps, but full universal access compliance remains a work in progress.

- Public acceptance: The elevated format can generate NIMBY opposition (visual intrusion, shadow, noise) and equity concerns if viewed as ‘just a better bus for the poor.’ Station-area placemaking — lighting, green space, local retail — is critical to social licence.

Technological

- In-Motion Charging (IMC): The IMC trolleybus model — where vehicles charge continuously from overhead wire on the trunk corridor and operate on battery for short off-wire segments — is emerging as the optimal propulsion architecture for high-frequency elevated BRT. UITP’s 2025 knowledge briefs explicitly frame IMC as best suited to long vehicles, high frequencies, and demanding duty cycles.

- Battery technology: Yutong’s ZK5180C delivers a 100 km off-wire range. As battery energy density improves, the economic advantage of full overhead wiring shrinks, but the operational reliability advantage of combined IMC remains significant for trunk corridors.

- Autonomous bus readiness: No commercial elevated BRT currently uses autonomous or platooning bus technology, but the fixed-guideway nature of elevated corridors makes them ideal candidates for Level 4 automation. Siemens, Volvo, and BYD all have urban bus automation programmes that could apply within 5–10 years.

- Digital twin and predictive maintenance: Real-time structural monitoring of viaducts using IoT sensor arrays and digital twin software can dramatically reduce maintenance costs and extend asset life — a capability now commercially available from Bentley Systems, Autodesk, and Siemens.

- MaaS integration: Elevated BRT corridors operating as part of Mobility-as-a-Service (MaaS) platforms — with seamless fare integration, real-time data feeds, and first/last mile integration with e-bikes, ride-hail, and microtransit — can serve as the high-throughput spine of a fully integrated urban mobility network.

Legal and Regulatory

- Procurement frameworks: Mexico City’s programme relied on direct public procurement of Chinese-manufactured vehicles, which simplified tendering but limits local content and competitive tension. International markets requiring open competitive tender (EU, World Bank funded projects) will need different procurement architectures.

- Environmental permitting: Elevated viaducts require Environmental Impact Assessments (EIAs) covering visual impact, noise, vibration, and construction phase disruption. In dense urban environments, EIA timelines can add 18–36 months to project schedules.

- Land use regulation: TOD (Transit-Oriented Development) around elevated BRT stations requires coordinated zoning changes — upzoning for density, parking reform, active frontage requirements. Most cities lack the regulatory toolkit to capture value at elevated BRT stations as effectively as they do around metro stations.

- Interoperability: Trolleybus systems require standardised catenary voltages and vehicle specifications. International standards (IEC, EN) provide frameworks, but proprietary variations (Chinese DC systems vs European AC standards) can create lock-in and interoperability barriers.

Environmental

- Zero direct emissions: Electric trolleybus elevated BRT produces zero tailpipe emissions at the point of operation — a major advantage in cities exceeding WHO PM2.5 and NO₂ thresholds. Mexico City’s air quality context makes this particularly salient.

- Grid carbon intensity: Well-to-wheel emissions depend on grid carbon intensity. Mexico’s grid (still ~60% fossil fuel) means current trolleybus operations are not carbon-neutral at the system level, though far better than diesel alternatives. Grid decarbonisation improves this over the asset’s 30–40-year life.

- Construction phase impacts: Viaduct construction is carbon-intensive (concrete, steel, construction equipment). Life-cycle analysis (LCA) needs to account for embodied carbon — a factor increasingly required by multilateral development bank climate finance standards.

- Biodiversity and urban heat island: Elevated structures reduce at-grade impervious surface compared to surface road expansion, and can incorporate green elements (planted columns, solar panels on station roofs) to partially offset urban heat island effects.

IV. SWOT Analysis: Elevated BRT as an Investment Asset

| Strengths | Weaknesses |

| Grade separation delivers rail-like reliability Lower capital cost vs. elevated rail (3-5x) Electric propulsion = zero tailpipe emissions Fleet flexibility: buses can operate off-guideway Proven technology (Yutong fleet, standard catenary) Faster construction vs. metro tunnelling Strong equity/social impact case in underserved corridors | High capital cost vs. surface BRT Not scalable beyond ~100,000 pphpd without full rail upgrade Visual intrusion and NIMBY risk Station accessibility challenges (height) Vehicle procurement currently China-dominated No established farebox revenue model Political vulnerability to mode-switching by successors |

| Opportunities | Threats |

| Rapidly falling battery costs improving off-wire economics MaaS integration potential as trunk corridor spine TOD value capture at stations if zoning is reformed Multilateral DFI financing increasingly available for green transport Autonomous bus technology in 5-10 year horizon Replication pipeline: Global South megacities (Nairobi, Lagos, Manila, Dhaka, Lima) IMC trolleybus infrastructure as EV charging backbone | Rail lobby competition for scarce urban transport capex Political discontinuity risk (new admin, mode preference change) Chinese supplier dominance (geopolitical risk for western markets) Grid decarbonisation pace risk (embodied + operational carbon) Ridership cannibalisation if metro network expands on same corridor Earthquake/structural failure risk (elevated structures) Construction cost inflation (concrete, steel, labour) |

V. Mode Comparison: Where Does Elevated BRT Fit in the Stack?

| Criterion | Surface BRT | Elevated BRT | Light Rail / Tram | Elevated Metro |

| Capital Cost/km | USD 2–15M | USD 20–35M | USD 30–80M | USD 100–350M+ |

| Peak Capacity (pphpd) | 5,000–15,000 | 15,000–30,000 | 20,000–45,000 | 40,000–80,000+ |

| Speed (avg commercial) | 15–25 km/h | 25–40 km/h | 20–35 km/h | 35–55 km/h |

| Service Reliability | Medium (traffic dependent) | High (grade-separated) | High (grade-separated) | Very High |

| Construction Timeline | 1–3 years | 2–5 years | 3–7 years | 7–15 years |

| Fleet Flexibility | Very High | High (off-wire capable) | Low (track-bound) | Very Low |

| Environmental Profile | Varies (diesel to EV) | Zero tailpipe (electric) | Zero tailpipe | Zero tailpipe |

| Land Use Disruption | High (lane removal) | Low (above traffic) | Medium–High | Low (tunnelled) |

| Rider Perception | Low–Medium | Medium–High | High | Very High |

| Optimal Corridor Demand | Low–Medium | Medium (40k–100k/day) | Medium–High | Very High (200k+/day) |

| INVESTMENT THESIS SUMMARY Elevated BRT is the optimal transit investment for corridors carrying 40,000–100,000 daily passengers in cities where: (1) surface BRT is politically or operationally compromised; (2) metro or LRT capex is unavailable or oversized for actual demand; and (3) electric propulsion can be delivered via overhead wire or IMC. The Mexico City programme demonstrates this thesis at scale. |

VI. Investment Criteria and Financial Architecture

A. Project Finance Fundamentals

Elevated BRT projects are typically structured as public sector infrastructure assets with government-guaranteed financing, not private concessions. This is because farebox revenues alone cannot service the capital debt in most Global South contexts. The investment framework therefore involves:

- Government or municipal bond issuance (Mexico City: direct government budget allocation)

- Multilateral Development Finance Institution (DFI) loans: IDB, World Bank, AFD, AIIB, EIB — all have active urban transport windows

- Green/Climate bond structuring: Eligible under ICMA Green Bond Principles for sustainable transport; opening access to ESG-focused institutional capital

- PPP concessions for operations and maintenance: While construction is typically public, O&M can be concessioned to private operators under performance-based contracts (gross cost or net cost models)

- Land Value Capture (LVC): Station-area TOD can generate significant uplift — typically 10–30% above baseline land values within 800m of BRT stations — which can be partially captured via betterment levies, density charges, or TIF mechanisms

B. Key Investment Metrics

| Metric | Elevated BRT Benchmark | Notes |

| Capital Cost/km | USD 20–35M | 2024/25 reference; varies with topography, soil, urban density |

| O&M Cost/km/year | USD 0.8–1.5M | Electric fleet; includes overhead line maintenance |

| Vehicle Cost (artic. trolleybus) | EUR 550,000–700,000 | Yutong ZK5180C class; 18m articulated with IMC battery |

| Farebox Recovery Ratio | 30–60% | Typical range in Global South; subsidised by government |

| Economic IRR (with externalities) | 12–22% | Including congestion relief, emissions savings, productivity |

| Financial IRR (farebox only) | Negative to 4% | Requires subsidy/DFI blended finance |

| Asset Useful Life | 30–40 years (structure) | Fleet replacement cycle: 12–15 years |

| Green Bond Eligibility | Yes (ICMA Category 3) | Sustainable transport; enables concessional pricing |

C. Investor Positioning

For institutional investors, elevated BRT infrastructure is not a direct equity play — it is a public asset. The investable opportunity set sits in:

- Infrastructure debt: Project bonds or DFI co-lending for construction; long-duration, investment grade when backed by sovereign or sub-sovereign guarantee

- Green bonds: Mexico City and peer cities are increasingly tapping green bond markets. DFI-backed first-loss tranches de-risk senior tranches for private institutional buyers

- Supplier equity: Vehicle manufacturers (Yutong, BYD, Volvo), catenary system suppliers (Furrer+Frey, Kummler+Matter), and digital operations platforms (Siemens, Cubic) are publicly traded or investable via private equity

- TOD real estate: Commercial and residential development within 800m of elevated BRT stations offers the most direct, investable upside, particularly in corridor zones undergoing land use reform

- Operations concessions: O&M PPP concessions, structured as gross-cost contracts with performance bonuses, are investable by infrastructure asset managers (Macquarie, Meridiam, Vinci Concessions)

VII. Hard Critiques: What the Boosters Don’t Say

| CRITIQUE 1: The Capacity Ceiling Problem Elevated BRT in its current form tops out at roughly 20,000–30,000 passengers per hour per direction — well below major metro lines. For corridors where demand is already near this ceiling, elevated BRT is a temporary solution, not a permanent one. Mexico City’s Line 11 targets 100,000 daily passengers; at two-directional peak loading, this is achievable. But if Chalco grows as projected, a rail upgrade conversation begins within 15–20 years. The infrastructure is not easily retrofitted for rail: different structure widths, turning radii, and platform heights. Cities must plan for mode upgrade at the corridor level from the outset. |

| CRITIQUE 2: The Chinese Supplier Lock-In Mexico City’s elevated BRT programme is 100% dependent on Yutong vehicles, built to Chinese DC catenary standards. This creates long-term vendor dependency for spare parts, software, and fleet renewal. For cities in jurisdictions with active geopolitical tensions with China (e.g., India, United States, Taiwan, some EU member states), or cities seeking to maximise local content and industrial policy objectives, this is a structural constraint. European alternatives (Solaris, Skoda, Van Hool) exist but at higher cost and without the full-system track record. |

| CRITIQUE 3: The ‘BRT Creep’ Risk Global experience shows that BRT systems, once built, often have their dedicated running ways eroded by political pressure — lanes converted back for general traffic, stations opened for non-transit vendors, signal priority removed. Elevation physically prevents this creep, which is a genuine advantage. But station areas can still degrade, and the ‘elevated’ label can mask poor-quality BRT at-grade sections (as seen in Jakarta’s Corridor 13, where the at-grade section in Tangerang remains congestion-prone). Elevation of the trunk section is necessary but not sufficient for system quality. |

| CRITIQUE 4: Ridership Demand Assumptions The Mexico City lines serve established, dense demand corridors. Projecting elevated BRT success to greenfield or low-density corridors based on Mexico City data is a category error. The demand case must be demonstrated for each specific corridor — not assumed from a global template. Elevated BRT built ahead of demand (a common infrastructure political trap) will have poor performance metrics and poison the concept for future applications. |

| CRITIQUE 5: The Accessibility Gap Elevated stations are inherently less accessible than surface-level platforms. Even with lifts, the step-count and transfer distance from street level to platform significantly disadvantages wheelchair users, elderly passengers, parents with prams, and passengers with luggage. Jakarta’s Corridor 13 was rightly criticised for near-total inaccessibility at launch. Mexico City has improved its design standards with Line 11, but universal access compliance to modern standards (e.g., UK Equality Act, ADA) adds cost and complexity that is often underestimated in project budgets. |

VIII. Novel Ideas and Engineering Frontiers

1. Solar-Integrated Elevated Stations

Station rooftops on elevated BRT are one of the most underutilised renewable energy assets in urban infrastructure. A 500 sqm station roof fitted with bifacial solar panels at 22% efficiency can generate 150–200 MWh per year — enough to power the station’s lighting, ventilation, CCTV, and passenger information systems entirely. Integrated battery storage at the station level can provide grid balancing services, generating additional revenue. Pilot programmes in Singapore and Mumbai metro stations are demonstrating the model; elevated BRT stations are an even better case due to consistent unshaded exposure.

2. Autonomous Platooning on Elevated Corridors

The fixed-guideway nature of elevated BRT — combined with the absence of crossing traffic — creates near-ideal conditions for autonomous bus platooning. Three or four vehicles operating in tight convoy under unified control could effectively triple throughput on a given elevated corridor without additional structure. Volvo, Scania, and ZF are all commercially active in highway platooning; applying this to an urban elevated BRT corridor is a logical next step. The controlled environment reduces the sensor and liability complexity that hampers urban autonomous vehicles on mixed-traffic streets.

3. Overhead Wire as EV Charging Infrastructure

As urban EV adoption accelerates, the overhead catenary infrastructure of trolleybus elevated BRT corridors has a second use case: opportunity charging for compatible electric trucks, taxis, and even private EVs at station interchange points. This convergence — transit infrastructure doubling as urban EV charging spine — dramatically improves the financial return profile of overhead wire investment. UITP’s 2025 policy briefs are beginning to articulate this dual-use case; it is not yet reflected in most project financing models but should be.

4. Hybrid Elevated BRT / Freight Corridor

Some elevated BRT corridors — particularly those running through industrial or port-adjacent zones — have off-peak capacity that could serve urban freight consolidation. Automated cargo pods running during overnight low-frequency windows on the elevated structure could deliver last-mile goods to elevated station ‘micro-depots,’ reducing surface-level delivery vehicle kilometres. This is speculative but technically feasible on a purpose-designed structure, and early-stage research is underway at TU Delft and the Tokyo Metropolitan University.

5. Digital Twin + Predictive Structural Maintenance

Elevated BRT structures require expensive periodic inspection and maintenance. Embedding fibre optic strain sensors, accelerometers, and corrosion detectors in pre-cast concrete elements — then feeding data into a continuous digital twin model — can shift maintenance from time-based to condition-based scheduling, reducing lifecycle costs by 20–35%. This technology is commercially available (Bentley Systems iTwin, Siemens MindSphere) and should be specified at the design stage for new elevated BRT projects.

6. Climate-Adaptive Design

Elevated BRT structures face long-term risk from climate change: increased storm water runoff, higher peak temperatures affecting concrete and catenary insulation, and extreme wind events affecting overhead wire stability. Forward-looking structural design should incorporate climate scenario modelling (RCP 4.5 and 8.5) into load calculations, drainage design, and material specifications — standard practice for coastal infrastructure but not yet routine for urban transit viaducts.

IX. Way Forward: Strategic Recommendations

For City Governments and Transport Planners

- Apply elevated BRT selectively: The business case is strongest on corridors with 40,000–100,000 daily passengers, severe surface congestion, and politically difficult lane removal. Do not over-apply the model to low-demand corridors.

- Design for mode upgrade: Structure widths, column spacing, and foundation loads should be specified from the outset to accommodate future rail conversion, even if rail is 20+ years away. The marginal cost of ‘rail-ready’ design is 5–8% of structure cost; the retrofit cost if not done is 40–60%.

- Mandate universal access compliance: Build to full ADA/UK Equality Act/CRPD standards from day one. Retrofitting accessibility is 3–4x the cost of designing it in.

- Integrate TOD from the planning stage: Zone-in density uplift and value capture mechanisms before construction begins. TOD value is created by the announcement, not the ribbon-cutting; early rezoning maximises public capture of value.

- Procure diversified: Consider multi-supplier procurement (Chinese and European/Japanese vendors) to build competitive tension and reduce long-term vendor dependency. Slightly higher upfront cost; significantly lower lifecycle lock-in risk.

For Development Finance Institutions

- Develop a dedicated elevated BRT financing window: Current DFI urban transport programmes treat elevated BRT and surface BRT identically. Given the different risk profile, capex requirement, and lifecycle economics, a dedicated product (with differentiated tenor, grace periods, and blended finance structures) would be more market-relevant.

- Mandate embedded LVC frameworks: All DFI-financed elevated BRT projects should require a Transit-Oriented Development Value Capture plan as a loan condition. Even partial LVC implementation can generate 10–15% of capital costs over the first 10 years.

- Support green bond certification: Work with ICMA and Climate Bonds Initiative to develop standardised certification criteria for elevated electric BRT, enabling access to EUR 1 trillion+ in ESG-labelled institutional capital.

For Investors

- Focus on the supplier chain: Yutong (HK: 3321), BYD (HK: 1211), Siemens Mobility (part of Siemens AG), and Furrer+Frey (private) are the primary beneficiaries of elevated BRT expansion. Track order pipelines in Mexico, Indonesia, and emerging African markets (Nairobi, Dar es Salaam) for leading indicators.

- TOD real estate: Identify corridors where elevated BRT is in planning stage; acquire station-proximate land before rezoning. A 3–5 year development horizon from BRT announcement to station opening is typical.

- Infrastructure debt in DFI-blended structures: Seek co-lending positions in World Bank/IDB/ADB-led elevated BRT project finance structures. Senior secured, sovereign-guaranteed debt at commercial-adjacent pricing with long duration is increasingly accessible to institutional investors in these structures.

X. Integration of elevated BRT with existing public transit networks

Integration of elevated BRT with existing public transit networks is one of the most underappreciated challenges in the field. The difficulties span physical, operational, digital, and institutional dimensions. Let me map them out: Integration is genuinely one of elevated BRT’s most persistent weak points, and the challenges cluster into seven distinct layers.

Physical and geometric mismatches are the most visible. When an elevated BRT station sits at 6–10 metres above street level and needs to connect to a surface metro entrance or a ground-level bus terminal, passengers face significant vertical travel — stairs, lifts, or ramps — before they even start their transfer walk. Mexico City’s Constitución de 1917 interchange between Line 10 and Metro Line 8 is a useful example: the connection works, but it requires descending from the elevated platform, crossing a concourse, and re-entering the metro at grade. At peak hours this transfer chain becomes a congestion point.

Fare and ticketing is arguably the highest-impact challenge for riders. Even where a unified smart card exists — as in Mexico City with the Tarjeta de Movilidad — a separate fare charge is typically levied for each mode. The absence of a free or discounted transfer within a timed window effectively penalises interchange, discourages multi-modal journeys, and can push riders back to private vehicles on corridors where a combined trip would be faster. Revenue-sharing agreements between agencies are politically complex and slow to negotiate.

Operational synchronisation is chronically underinvested. Elevated BRT and metro systems typically run on independent control architectures with separate traffic management centres. When a metro delay happens, there is no automatic signal to the BRT control room to hold vehicles or increase frequency; passengers arrive at the interchange and find a 12-minute gap. Timetable co-ordination — even in cities with a unified transport authority — tends to happen at the planning stage and drift apart in real operations.

Digital and data integration should be easier than the physical challenges, but rarely is. Different agencies run different GTFS feeds, different vehicle tracking systems, and different APIs. Journey planners (Google Maps, Moovit, Apple Maps) often model elevated BRT lines inaccurately, with incorrect interchange times or missing connections. Wayfinding signage at multi-level interchange stations is frequently managed by two different agencies with different standards, creating visual confusion for passengers navigating between modes.

Accessibility is a critical fault line. Elevated BRT stations depend on lifts for wheelchair and pram access, and lift reliability in public transit globally averages 85–92% uptime — meaning on any given day, roughly 1 in 10 lifts is out of service. For a passenger who relies on step-free access, a single failed lift at an interchange can make an entire journey impossible. The problem compounds when bus platform edges don’t align precisely with bus door heights, creating boarding gaps that are manageable for most passengers but impassable for wheelchair users without staff assistance.

Institutional fragmentation is the deepest structural problem. In most cities, elevated BRT, surface bus, metro, and light rail are operated by different entities — sometimes different companies, sometimes different arms of the same government, sometimes across municipal or state boundaries. Mexico City’s elevated trolleybus is operated by STE (Servicio de Transportes Eléctricos del DF), while the metro is operated by the Sistema de Transporte Colectivo — two separate agencies under the same city government but with separate budgets, procurement processes, and cultures. Line 11 crosses into Estado de México, adding a state-versus-city governance layer. These institutional seams are extremely difficult to close without a unified transport authority with genuine cross-mode powers.

Power and infrastructure conflicts emerge when elevated trolleybus catenary approaches existing rail infrastructure. Voltage standards differ (Mexican trolleybus systems use 600V DC; metro uses 750V DC traction power); overhead line geometry near covered metro stations creates clearance engineering problems; and depot-sharing between bus and rail fleets is rarely designed in from the start, meaning charging or maintenance facilities are duplicated rather than rationalised.

The way forward on integration typically requires three things that rarely happen together: a unified mobility authority with cross-modal budgetary power, a single fare system with time-based transfer allowances, and interchange stations that are co-designed by all operators from the outset rather than bolted together post-construction. London’s TfL model is the closest global exemplar — but it took decades to consolidate and required genuine political will at the mayoral level to achieve it.

XI. Conclusion: The Decade of the Elevated Corridor

The world’s cities are in the middle of a mobility reckoning. Traffic congestion costs global economies an estimated USD 1 trillion per year. Urban air quality kills millions. Metro networks are prohibitively expensive for most of the Global South’s rapidly urbanising cities. And surface BRT, while cheap, is politically and operationally fragile in the constrained, contested streets of dense megacities.

Elevated BRT does not solve all of this. It is not a universal answer. But for the specific condition — medium-density corridor, politically impossible lane removal, capital-constrained government, electric propulsion commitment — it is a remarkably elegant solution. Mexico City has demonstrated this not once but twice, and is now building a third line while other cities take notes.

The decade ahead will likely see elevated BRT move from niche experiment to mainstream infrastructure category. The enabling conditions are converging: falling battery and catenary costs, maturing DFI financing windows, strengthening ESG capital markets, and the emergence of autonomous platooning technology that could unlock capacity well beyond current design limits.

The sky route is not for every corridor. But for the right corridor, in the right city, it may be the most important transit investment of the coming decade. The question is not whether elevated BRT will spread — it is which cities will move fast enough to capture the first-mover advantage in design knowledge, supply chain relationships, and TOD value.

Mexico City built the model. The next chapter is replication, refinement, and scale.

| “The sky route is not for every corridor — but for the right corridor, it may be the most important transit investment of the coming decade.” |

References

1. Urban Transport Magazine. (2022, September). Mexico City: An Elevated BRT Trolleybus! urban-transport-magazine.com

2. Urban Transport Magazine. (2025, May). First ‘Interstate’ Trolleybus Opened in Mexico. urban-transport-magazine.com

3. Sustainable Bus. (2023, May). What’s New in Mexico City Trolleybus Network? BRT Is Coming. sustainable-bus.com

4. IDOM Consulting. (2022). New Trolleybus Line in Mexico City — Planning Studies. idom.com

5. UITP. (2025, April). In-Motion Charging: Knowledge Brief. uitp.org

6. UITP. (2024, September). Policy Brief: In-Motion Charging Trolleybus. uitp.org

7. ITDP. (2025, November). Sustainable Transport Award Spotlight: CDMX. itdp.org

8. World Bank. (2018). Electric Mobility and BRT — Sector Review. documents1.worldbank.org

9. US Federal Transit Administration. (2009). Characteristics of Bus Rapid Transit for Decision-Making. transit.dot.gov

10. Wikipedia. (2025). Transjakarta Corridor 13. en.wikipedia.org

11. Wikipedia. (2025). Xiamen BRT. en.wikipedia.org

12. Region.nyc. (2025, December). Exploring Xiamen’s Innovative Elevated BRT System. region.nyc

13. Steer Davies Gleave. (n.d.). LRT versus BRT: Which Is the Better Option? steergroup.com

14. ITDP. (2024). BRT Standard Scores. itdp.org/library/standards-and-guides

15. BloombergNEF. (2026, January). Energy Transition Investment Trends 2025. about.bnef.com

16. YouTube. (2022). Elevated Trolleybus BRT — Mexico City Analysis. youtube.com/watch?v=p6dPQh2eAPk

17. Gobierno de CDMX. (2022). Launch material — Trolebus Elevado Line 10. cdmx.gob.mx

{kind=link}

{kind=link}

{kind=link}

{kind=link}