Preamble

Cargo drones are moving from experimentation into early commercial reality, but the market is still segmented by payload class, route type, and regulatory maturity. China is currently the clearest example of scaled deployment in urban and regional drone logistics, while the United States and Europe are building toward larger middle-mile and heavy-lift use cases through certification-led pilots and limited operations.

This document follows the analytical flow used in the airship series Navigating the Skies Pt1 Navigating the skies Pt 2 , Navigating the skies Pt3 , Navigating the skies Pt4 and reframes it for cargo drones: what they are, how the market is evolving, where they fit, what infrastructure and precursors are needed, who the stakeholders are, what the technology stack looks like, where AI and GPS matter, and what a plausible deployment timeline looks like.

Reintroducing the cargo drone

Definition and evolution

A cargo drone is an unmanned aircraft system designed to transport physical goods rather than capture imagery or perform inspection alone. Depending on the mission, it can be a multirotor, fixed-wing aircraft, tilt-rotor, or hybrid VTOL platform, with different trade-offs in payload, speed, runway dependence, endurance, and cost.

The sector has evolved in three broad waves. The first wave focused on small parcel and medical delivery, usually under visual line of sight or tightly controlled beyond visual line of sight corridors. The second wave introduced more capable middle-mile and regional aircraft, including hybrid and fixed-wing designs intended to move tens to hundreds of kilograms between logistics nodes. The current wave is about system integration: regulation, fleet operations, remote supervision, digital airspace coordination, automated loading, and economics at repeatable route density.

Why cargo drones now

The underlying demand drivers are faster fulfilment expectations, pressure to decarbonize logistics, shortage of reliable access in remote geographies, and the need for resilient point-to-point transport that is less dependent on roads. At the same time, battery systems, autopilot software, communications links, remote operations software, and digital traffic management have improved enough to support real commercial service on selected corridors.

Market landscape

Market size and direction

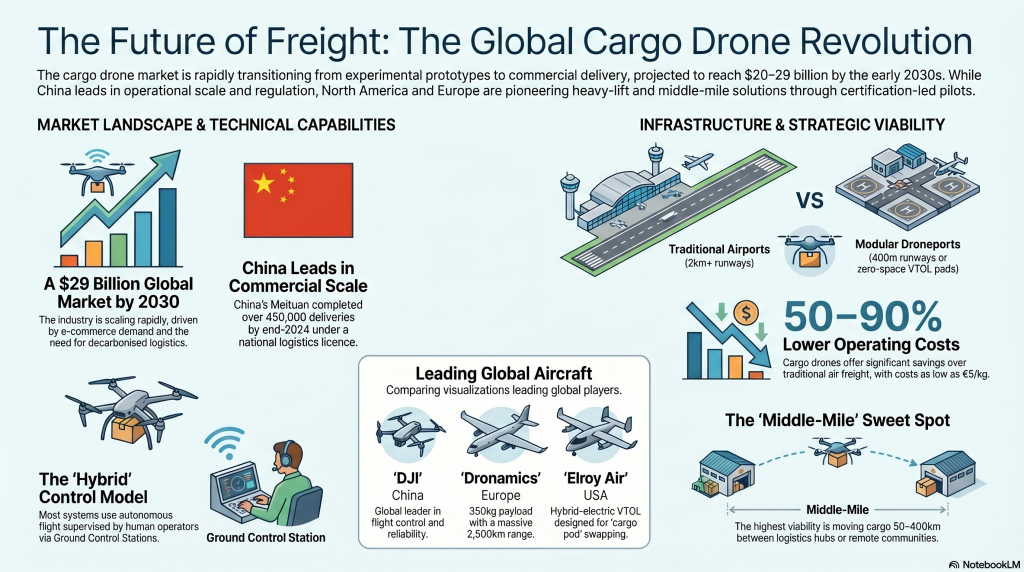

Forecasts vary, but multiple market trackers place the broader drone delivery and cargo drone market on a steep growth curve into the early 2030s, with estimates commonly reaching the tens of billions of dollars globally. These projections should be treated as directional rather than precise, because definitions differ across reports: some include last-mile delivery drones, some include heavy-lift systems, and some combine software and services with aircraft sales.

Geographic dynamics

China is a leading performer in manufacturing capacity, commercialization pace, and policy support for low-altitude logistics. Meituan secured China’s first nationwide low-altitude logistics operating license and reported more than 450,000 completed deliveries on 53 routes by the end of 2024, which makes China the strongest proof point for scaled routine operations rather than isolated pilots.

North America remains important because the United States has major e-commerce demand, defense spending, startup funding, and aircraft developers pushing into larger cargo applications. Europe’s role is strongest in certification-first regional logistics, with Dronamics and Wingcopter showing that the continent is building credible platforms for middle-mile and rural delivery rather than only small urban parcel drones.

The market is best understood by payload class and mission profile rather than by one generic “cargo drone” category. A practical segmentation is shown below.

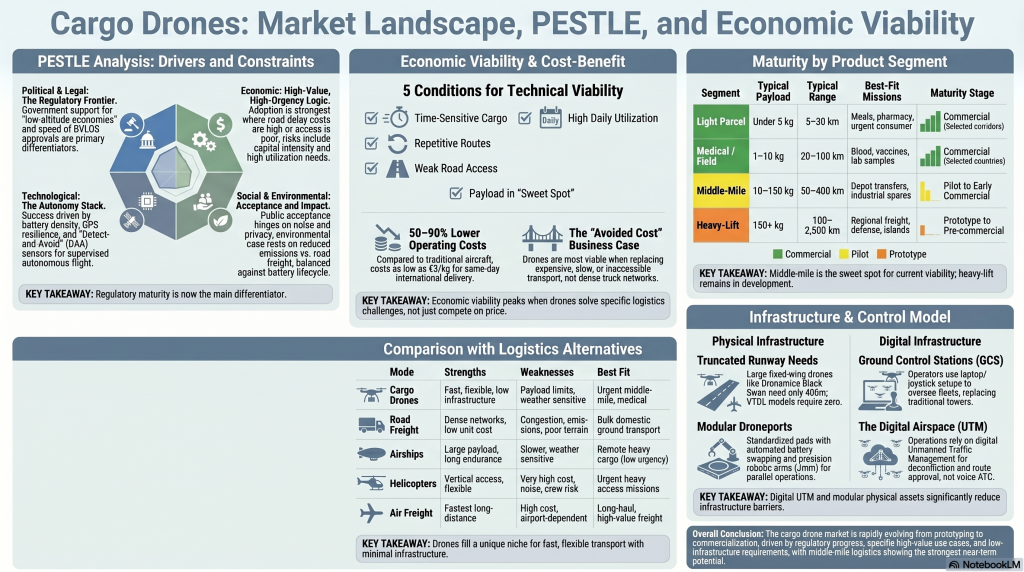

| Segment | Typical payload | Typical range | Best-fit missions | Maturity |

| Light parcel | Under 5 kg | 5–30 km | Meals, pharmacy, urgent consumer items | Commercial in selected corridors |

| Medical / field logistics | 1–10 kg | 20–100 km | Blood, vaccines, lab samples, emergency medicines | Commercial in selected countries |

| Middle-mile cargo | 10–150 kg | 50–400 km | Distribution center transfers, industrial spares, offshore supply, remote communities | Pilot to early commercial |

| Heavy-lift cargo | 150 kg+ | 100–2,500 km depending on architecture | Regional freight, defense resupply, remote infrastructure, island logistics | Prototype to pre-commercial |

Multirotor aircraft offer the simplest vertical takeoff and landing profile, making them useful where there is no runway and missions are short. Fixed-wing aircraft offer much better range and payload efficiency but usually need launch, recovery, or runway support unless they use VTOL transition. Hybrid VTOL systems aim to combine both advantages, though this adds mechanical and certification complexity.

Battery-electric drones are quiet, mechanically simpler, and attractive for short routes, but range and payload are constrained by battery energy density. Hybrid-electric systems extend range and mission flexibility and are therefore common in larger cargo concepts. Hydrogen fuel-cell systems are increasingly discussed because they can improve endurance relative to batteries, although the ground handling and fuel ecosystem are less mature.

Dronamics’ Black Swan is one of the clearest middle- to heavy-cargo examples in Europe, with publicly cited specifications of 350 kg payload, 2,500 km range, and operations from a roughly 400 m runway. MightyFly has publicly discussed a cargo aircraft capable of carrying roughly 500 lb over long distance, while Wingcopter has focused on delivery systems suited to regional and rural logistics. In China, Meituan and EHang illustrate the split between dense-network delivery systems and larger autonomous aircraft development.

Cargo drones do not serve one buyer group. The market is a multi-stakeholder system shaped by cargo owners, operators, regulators, infrastructure providers, and communities.

- E-commerce platforms and parcel integrators that want faster replenishment or lower-cost service to hard-to-reach areas.

- Healthcare systems, laboratories, hospitals, and ministries of health that need reliable transport of time-sensitive medical items.

- Industrial operators in mining, energy, offshore, agriculture, and construction that need spare parts or tools delivered to remote sites.

- Defense and civil protection agencies that value access, resilience, and reduced risk to crews in difficult terrain.

- Regulators, air navigation authorities, telecoms providers, insurers, and local communities that determine whether operations can scale safely.

The end user is often not the same as the payer. A consumer receiving food or medicine may be the visible beneficiary, but the economic buyer may be a logistics operator, a hospital network, a mining company, or a government program. That distinction matters because procurement criteria differ: healthcare prioritizes reliability and cold-chain integrity, e-commerce prioritizes service level and cost, while defense prioritizes resilience and mission assurance.

In developed markets, the most viable use cases are usually constrained by service-level economics rather than physical access alone. Strong examples include suburban and rural last-mile delivery, pharmacy replenishment, inter-facility medical logistics, offshore and energy-site supply, and middle-mile transfer between warehouses when roads are slow or unreliable.

Global South and emerging markets

In the Global South, the strongest use cases often arise from infrastructure gaps rather than convenience demand. Cargo drones can help move blood, vaccines, diagnostics, agricultural inputs, emergency supplies, and critical documents where roads are poor, seasonal, insecure, or absent. They can also support island logistics, mining corridors, humanitarian response, wildlife protection, and government service delivery in dispersed geographies.

Why the middle-mile matters most

The current commercial sweet spot is middle-mile logistics: routes long enough that road transport is slow or costly, but short enough that drone payload and energy limits still work. In practice, that often means 50–400 km routes moving high-value or time-sensitive cargo between depots, clinics, ports, airstrips, industrial sites, or small communities.

Technology stack: people, process, and tech

A working cargo drone service still needs substantial human infrastructure even when the aircraft itself is autonomous. Core roles include remote pilots or supervisors, flight operations managers, maintenance technicians, payload and dispatch staff, safety managers, software and network engineers, regulatory liaison staff, trainers, and customer success or commercial teams.

Successful operations depend on repeatable process design more than on aircraft novelty alone. Critical processes include route planning, flight approval, loading and manifesting, battery or fuel handling, weather go/no-go checks, pre-flight and post-flight inspections, exception handling, cargo chain-of-custody, cybersecurity response, maintenance scheduling, and incident reporting.

The enabling technology stack typically includes the aircraft, flight computer, autopilot software, detect-and-avoid sensors, command-and-control links, navigation modules, weather data feeds, a ground control station, fleet management software, payload handling systems, and digital integration with warehouse or hospital logistics systems. For scale, operators also need identity and access controls, telemetry storage, predictive maintenance analytics, documentation systems, and integration into unmanned traffic management workflows.

The role of AI, GPS, and autonomy

AI is increasingly central to autonomy, route optimization, fleet health monitoring, anomaly detection, object recognition, and detect-and-avoid support. In practice, however, the near-term commercial model is usually supervised autonomy rather than unsupervised full autonomy: the aircraft flies much of the mission itself, but humans monitor the operation and can intervene when needed.

GPS or GNSS is foundational for route planning, positioning, geofencing, return-to-home logic, and synchronization with digital airspace systems. Yet GPS alone is not enough for safe scaled cargo operations. Mature systems add inertial navigation, terrain data, communications redundancy, onboard sensing, and in some cases visual navigation or other backup methods to mitigate signal loss, spoofing, or urban canyon effects.

Remote, AI-controlled, or hybrid

The sector is not cleanly divided into human-controlled versus AI-controlled systems; it is mostly hybrid. Aircraft may navigate autonomously between waypoints, while remote operators supervise fleets, approve exceptions, monitor weather and telemetry, and coordinate takeoff and landing windows. This hybrid model is commercially important because it usually reduces labor intensity without asking regulators to accept fully detached accountability.

Cargo drones are not all at the same maturity level. The sector should be viewed across three stages rather than one headline market status.

| Stage | What it looks like | Typical examples |

| Planning | Concept design, early fundraising, lab tests, route modeling, regulatory engagement | Many heavy-lift and long-range concepts |

| Prototype / pilot | Flight testing, BVLOS trials, route demonstrations, limited customer pilots | Wingcopter rural pilots; heavy-lift testing by multiple developers |

| Delivery / early commercial | Repeated service on defined routes, operational licenses, integrated logistics workflow | Meituan network deliveries; selected medical and rural logistics services |

The market has therefore already passed the “just planning” stage, but it has not yet reached broad universal deployment. Small and medium systems are operational today in selected geographies, while larger regional cargo aircraft remain mostly in advanced testing, early certification, or pre-commercial launch phases.

Do cargo drones need airports?

Usually not in the conventional sense. Many eVTOL or multirotor systems can use droneports, rooftop pads, fenced logistics yards, hospital grounds, or compact launch-and-recovery areas, while fixed-wing cargo drones may need only a short strip compared with conventional aircraft.

A practical cargo drone network still needs dedicated support infrastructure, even if it is lighter and cheaper than traditional airport infrastructure. The baseline stack often includes:

- Landing pads, micro-airstrips, or droneports with clear safety perimeters.

- Ground handling and secure cargo loading systems, including cold-chain capability for medical use.

- Charging, battery swap, or fuel handling facilities depending on propulsion type.

- Maintenance bays, spare parts, and field service tools.

- Network connectivity, telemetry backhaul, and operations software.

- Weather monitoring, local obstacle data, and emergency procedures.

Digital infrastructure is as important as the pad itself. Operators need UTM integration, digital approvals, remote identification, fleet management dashboards, cybersecurity controls, and clean data exchange with dispatch systems, customers, and sometimes customs or public authorities.

Controllers, navigation, and airspace management

Cargo drones do not usually depend on traditional tower-centric control in the way crewed aircraft do. Instead, the operating core is a ground control station or remote operations center that supervises one or more aircraft and interfaces with regulators or traffic systems as required.

At scale, routine operations require a form of unmanned traffic management to handle separation, conflict detection, approved corridors, contingency routing, and operational visibility. In less mature markets, this may begin as a corridor-specific or operator-specific workflow before evolving into broader shared low-altitude traffic systems.

Cargo drones are not automatically cheaper than all alternatives. Their strongest economics appear where they replace expensive, slow, dangerous, or highly unreliable transport rather than where they compete head-on with dense truck networks on commoditized routes.

For some use cases, Dronamics has claimed prices as low as €5 per kg and operating costs 50–90 percent lower than conventional aircraft, illustrating the type of cost advantage that may be possible on selected routes. Those figures should be interpreted as route-specific commercial claims rather than universal industry averages.

What scale makes drones viable

Technical viability improves when five conditions align.

- Cargo is time-sensitive, high-value, or mission-critical.

- Payload is within the aircraft’s sweet spot rather than near its maximum every flight.

- Routes are repetitive enough to amortize infrastructure and regulatory setup.

- There is weak road access, poor terrain, congestion, or service unreliability.

- Utilization is high enough that the aircraft, team, and landing sites are not idle most of the day.

This is why a 2 kg blood pack can be economically justified in one geography, while a 50 kg consumer freight shipment may not be justified in another. The business case depends on avoided costs, avoided delays, service criticality, and network density rather than payload alone.

Major risks include weather sensitivity, collision risk, GPS interference or spoofing, communications loss, battery or propulsion failure, cyber intrusion, payload security, and weak emergency procedures. In urban or mixed airspace settings, integration with helicopters, general aviation, and other drones adds complexity.

Safety and compliance requirements

Operators need airworthiness assurance, route approvals, remote pilot procedures, maintenance programs, training standards, emergency playbooks, and cyber resilience. Public trust also matters: noise, privacy, perceived safety, and visible reliability shape whether communities and regulators support scale-up.

- Fast point-to-point delivery for urgent, high-value cargo.

- Lower infrastructure burden than conventional aviation for many missions.

- Potential emissions benefits, especially for electric systems and road-avoiding routes.

- Access to remote, island, mountainous, congested, or disaster-affected areas.

- Payload limits remain tight for many platforms.

- Weather, battery performance, and communications reliability constrain operations.

- Regulation and certification can slow commercialization.

- Network economics depend heavily on route density and utilization.

- Healthcare logistics, e-commerce, defense, industrial parts, humanitarian relief, and rural connectivity.

- National low-altitude logistics networks, especially in countries actively modernizing regulation.

- Integration with warehouse automation, predictive logistics, and AI-enabled dispatch.

- New logistics models for islands, mining, offshore energy, and climate-vulnerable areas.

- Competition from trucks, vans, helicopters, conventional cargo aircraft, and in some long-range bulk niches, airships.

- Slow regulatory harmonization across jurisdictions.

- Public backlash around safety, privacy, or noise.

- Rapid technology shifts that can obsolete current platforms before full scale-up.

Government support for low-altitude economy development, public procurement, and clearer BVLOS policy can accelerate adoption materially. Conversely, fragmented rules and slow inter-agency coordination can suppress scaling even when the technology works.

The business case is strongest where delay costs are high or access problems are severe. Rising e-commerce demand and pressure on healthcare delivery networks support growth, but capital intensity and uncertain utilization can weaken investor confidence.

Public acceptance depends on visible safety, low noise, privacy protection, and fairness in where services are deployed. In emerging markets, social value can be easier to demonstrate because cargo drones may solve obvious access problems rather than mere convenience.

Autonomy, batteries, detect-and-avoid, fleet software, communications redundancy, and GPS resilience are all decisive enablers. Weakness in any one of these layers can limit system-wide performance more than aircraft design alone.

Regulatory maturity is now one of the main differentiators between performer markets and laggard markets. Certification, liability, insurance, privacy, airspace access, and cross-border permissions remain major gating factors.

Cargo drones can reduce emissions in some route profiles and reduce dependence on road-building in fragile environments. But battery lifecycle, energy source, noise footprint, and wildlife interactions still need proper management.

| Mode | Strengths | Weaknesses | Best fit |

| Cargo drones | Fast, flexible, relatively low infrastructure, good for urgent or hard-to-reach cargo | Limited payload, weather and regulation constraints | Urgent middle-mile, medical, remote access |

| Conventional air freight | Highest speed over long distance, mature airport system [cite:48] | High cost, airport dependence, weaker economics for small dispersed loads [cite:48] | Long-haul, high-value freight |

| Road freight | Dense networks, low unit cost at scale, strong last-mile reach [cite:48] | Congestion, road quality limits, emissions, slow in remote terrain [cite:48] | Bulk domestic ground transport |

| Ships | Very low cost for bulk cargo, huge capacity [cite:48] | Slow, port dependence, limited inland access [cite:48] | Bulk international freight |

| Helicopters | Vertical access and flexible deployment | Very high cost, noise, crew risk, lower sustainability | Urgent heavy access missions |

| Airships | Potentially large payload and long endurance, good for bulky low-urgency cargo [cite:48] | Slower, weather sensitivity, lower commercial maturity today [cite:48] | Heavy cargo to remote regions where time is less critical |

Airships are the most relevant comparison when the question is not “Can a drone fly there?” but “What aerial mode best serves remote logistics over weak infrastructure?” In general, cargo drones are ahead in near-term deployability for light to medium urgent cargo, while airships may become more compelling for slower, heavier, or oversized freight if their own commercialization hurdles are solved.

Companies and competitive landscape

China’s ecosystem combines manufacturers, platform operators, and low-altitude policy momentum. Meituan is the clearest logistics-scale operator, while EHang and other Chinese firms show broader autonomous aircraft ambition, including larger aircraft categories adjacent to cargo logistics.

Dronamics positions itself around regional same-day cargo, using a larger fixed-wing unmanned aircraft for middle-mile freight. Wingcopter has pursued rural, medical, and regional logistics models and partnered on delivery pilots in Germany and beyond.

United States and North America

The United States has several technically ambitious entrants, including Elroy Air and MightyFly, focused on higher-payload and longer-range middle-mile networks. Their challenge is less the absence of need than the slower path from successful test program to routine, certified, scaled service.

A realistic MVP for cargo drones is a narrow corridor service with a limited aircraft type, one or two landing sites, clear demand, and tightly defined cargo categories. The ideal first deployment is repetitive, politically supportable, operationally simple, and visibly valuable, such as medical logistics, remote site resupply, or warehouse-to-warehouse middle-mile transfer.

- Feasibility phase: route mapping, stakeholder alignment, regulatory engagement, site assessment, and cargo demand validation.

- Pilot phase: controlled operations, safety case development, limited customer onboarding, and operating data collection.

- Operational phase: repeatable schedules, digital workflow integration, stronger uptime, and formal service-level agreements.

- Network phase: multi-route scaling, fleet optimization, cross-site maintenance, and deeper integration with logistics systems and public infrastructure.

The near-term period is likely to be dominated by more BVLOS approvals, more corridor-based operations, better remote supervision tools, and wider deployment of medical and rural logistics networks. China will probably remain ahead on scaled urban and peri-urban commercial routine delivery, while the US and Europe continue converting advanced prototypes into certified commercial systems.

This period is likely to bring more middle-mile route economics, more autonomous ground handling, deeper UTM integration, and early regional freight services using heavier aircraft. Commercial separation will become clearer between operators that built repeatable networks and those that built impressive aircraft without reliable demand density.

By the early 2030s, the most likely outcome is not universal drone freight but a stratified market: small drones in dense local delivery, medium drones in healthcare and rural logistics, and selected heavier systems in regional freight corridors. The winning companies will probably be those that combine aircraft capability, regulatory credibility, operational software, and real customer workflow integration rather than those relying on hardware alone.

Cargo drones are no longer a speculative concept, but they are also not a one-size-fits-all replacement for existing freight systems. Their highest value is emerging where terrain, urgency, resilience, or weak infrastructure make conventional logistics perform poorly.

For developed markets, this means niche but growing roles in middle-mile, medical, offshore, and rural service. For the Global South, the upside is potentially larger because cargo drones can function as logistics leapfrog infrastructure, especially when paired with digital health, e-government, agricultural support, and emergency response networks.

The decisive question is therefore not whether cargo drones are technically possible. The decisive question is where the aircraft, infrastructure, regulation, and demand can be combined into repeatable route economics and trusted public operations.

{kind=link}

{kind=link}

{kind=link}

{kind=link}