Preamble: Why Does Ice Still Exist as a Business?

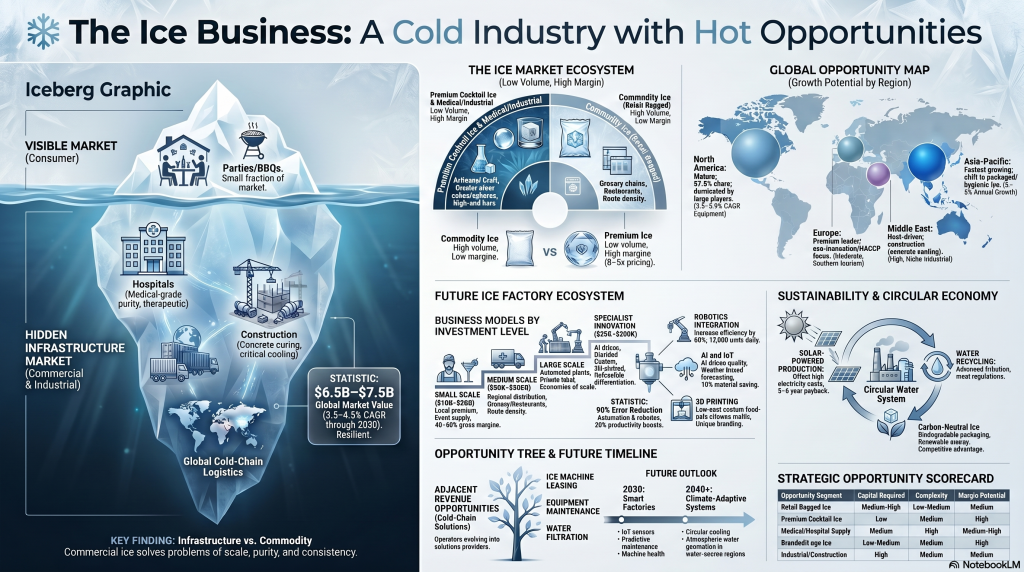

In an age where nearly every household owns a refrigerator with an ice maker, the persistence of the commercial ice industry seems paradoxical. Yet this sector generates between $6.5 and $7.5 billion annually, with projected growth of 3.5-4.5% through 2030. The answer to its survival lies not in competition with home freezers, but in fundamental gaps those appliances cannot fill.

Commercial ice serves needs that transcend simple cooling. A restaurant requires hundreds of pounds daily—far beyond any residential capacity. A hospital needs medical-grade purity. A craft cocktail bar demands crystal-clear spheres that won’t dilute premium spirits. A construction site in Dubai needs tons of ice for concrete curing. These applications share a common thread: they require volume, consistency, specialization, or quality that home production cannot match.

The industry persists because it solves real problems at scale. Food safety regulations mandate specific ice standards. Event planners need reliable supply for gatherings of hundreds. Fishing vessels require industrial quantities for preservation. The premium spirits movement has created demand for artisanal ice that took hours to freeze using directional techniques. Even climate change paradoxically fuels demand, as rising temperatures increase cooling needs across agriculture, construction, and daily life.

This is not a dying industry being displaced by technology. It’s a mature sector experiencing transformation through innovation, premiumization, and diversification into specialized niches that didn’t exist a decade ago.

As usual references: ICE industry references

Global Market Landscape: Where Ice Thrives

North America: Mature Markets with Premium Evolution

North America represents 37.8% of global market share, dominated by established players like Reddy Ice (the world’s largest packaged ice manufacturer) and Arctic Glacier. The region demonstrates mature market characteristics: consolidated players, extensive distribution networks, and high retail penetration.

Yet beneath this stability lies evolution. The craft cocktail movement has created demand for premium ice products—clear cubes and spheres that retail for $10-20 per bag compared to $3-5 for standard ice. Sustainability pressures are driving investment in recyclable packaging and renewable energy. Automation is reshaping production economics, with robotic systems now handling up to 12,000 units daily with 90% reduction in human error.

Asia-Pacific: The Growth Frontier

This region shows the fastest expansion at 6-8% annually, led by China, India, and Southeast Asia. Growth drivers include expanding middle classes, modernization of food service sectors, and infrastructure development supporting cold chain logistics.

The market remains highly fragmented, mixing large players with thousands of small local producers. This creates opportunities for consolidation, quality differentiation, and introduction of Western premium concepts. The shift from traditional block ice to packaged cube and nugget ice represents both cultural change and hygiene advancement, with branded, hygienic ice gaining importance among health-conscious consumers.

Europe: Premium Leadership and Sustainability

European markets emphasize quality over volume, with strong regulatory frameworks (HACCP, ISO 22000) creating barriers to entry but also protecting quality-focused operators. The region leads in eco-innovation, with high demand for energy-efficient production and sustainable packaging.

Southern Europe’s tourism sector and Northern Europe’s premium bar culture drive specialized ice demand. The market increasingly values ice as an ingredient rather than commodity—craft ice for cocktails, specific shapes for particular spirits, even mineral-enhanced varieties for health-conscious consumers.

Emerging Markets: Infrastructure-Dependent Growth

Latin America (particularly Brazil and Mexico), the Middle East, and Africa present varied opportunities. The Middle East shows strong demand driven by extreme heat, construction applications (concrete cooling), and tourism. Latin America’s growth links to climate, tourism seasonality, and modernization of retail infrastructure.

These markets often lack established distribution networks, creating first-mover advantages for well-capitalized entrants. However, infrastructure challenges, regulatory environments, and fragmented customer bases require localized strategies rather than direct transplantation of Western models.

Technology Transformation: Beyond Simple Freezing

Robotics and Automation: The Efficiency Revolution

The integration of robotics represents perhaps the most significant operational transformation. Robotic demoulding systems now increase production efficiency by 80%, handling up to 12,000 units daily in continuous operation. Automated packaging and palletizing systems process 65 bags per minute in the harsh, humid conditions of ice production facilities—environments that challenge both human workers and machinery.

The economic case is compelling. Automation reduces human error by up to 90% while delivering 50% productivity boosts. For medium and large operations, these systems offer 18-24 month payback periods through labor savings, quality improvements, and increased throughput. The technology has matured beyond early-adopter risk into proven, commercially viable solutions.

Artificial Intelligence: From Reactive to Predictive

AI integration extends beyond factory floors into strategic operations. Quality control systems monitor production parameters in real-time, catching deviations before they affect product quality. Predictive maintenance algorithms analyze equipment performance patterns, scheduling interventions before failures occur and reducing costly unplanned downtime.

Weather-based demand forecasting represents particularly powerful application. By analyzing historical sales data against weather patterns, AI systems predict demand spikes 7-14 days ahead, optimizing inventory levels and reducing waste. Smart production optimization can save up to 10% on raw materials—significant when operating at industrial scale.

For entrepreneurs, this technology democratizes capabilities once exclusive to large corporations. Cloud-based AI platforms offer sophisticated analytics without requiring in-house data science teams, allowing smaller operators to compete on intelligence rather than scale alone.

3D Printing: Customization at Scale

Three-dimensional printing transforms the economics of customization. Traditionally, custom ice molds required expensive machining, viable only for large orders. 3D printing enables economical production of unique molds for small batches, opening entirely new business models.

Applications range from practical to whimsical. Bars order custom molds featuring their logos or signature designs. Wedding planners commission unique ice sculptures or branded cubes. Corporate events feature product-shaped ice. The technology produces food-safe silicone molds from 3D-printed masters, combining digital flexibility with production-grade durability.

This capability creates competitive moats. Custom shapes, proprietary designs, and rapid prototyping differentiate premium operators from commodity producers. The barriers to entry remain low—desktop 3D printers start under $500—but the creative application requires design capability and understanding of freezing physics to ensure shapes release cleanly.

Sustainability Technologies: Environmental and Economic Alignment

Solar-powered ice production addresses both environmental concerns and operational costs. In sunny regions, solar arrays can provide significant portions of production energy, with payback periods of 5-8 years and ongoing cost savings thereafter. Water recycling systems improve resource efficiency—critical in water-scarce regions or under increasing regulatory pressure.

Biodegradable packaging solutions address plastic waste concerns while creating marketing advantages. Companies investing in plant-based packaging report positive customer response, particularly from corporate buyers with sustainability mandates. While currently more expensive than conventional plastic, economies of scale are improving economics as adoption spreads.

These investments serve dual purposes: genuine environmental benefit and competitive differentiation. In markets with sophisticated corporate buyers, sustainability credentials increasingly influence purchasing decisions, transforming environmental investments from costs into revenue enablers.

Strategic Entry Points: Scale-Appropriate Opportunities

Small-Scale Artisanal Operations ($10,000-$50,000)

Investment Thesis: Target the premium cocktail and gourmet market with high-quality, customized products that command 40-60% margins through quality differentiation rather than volume competition.

Core Strategy: Start with specialized equipment: a directional freezing system for crystal-clear ice ($2,000-$5,000), commercial-grade ice machines ($3,000-$8,000), basic packaging supplies, and delivery vehicle. Focus on high-end bars, restaurants, and event planners within a tight geographic radius to minimize logistics costs.

The product differentiator is quality: crystal-clear, slow-melting ice produced through techniques that eliminate air bubbles and impurities. Large-format cubes for whiskey, perfect spheres for old-fashioneds, custom shapes for signature cocktails. Utilize 3D printing for custom molds, offering personalization that large producers cannot economically match.

The business model emphasizes relationships over transactions. Visit potential customers, educate bartenders about ice quality’s impact on drink presentation and dilution, offer trial deliveries. Develop subscription models for recurring revenue—weekly deliveries to regular accounts create stable cash flow.

Key Success Factors:

- Obsessive quality focus—every cube must be perfect

- Direct customer relationships built on reliability and service

- Local market knowledge to identify and serve premium establishments

- Willingness to start small and grow organically through reputation

Realistic Expectations: Revenue potential of $75,000-$150,000 annually once established, with 40-60% gross margins. Growth is limited by personal capacity and local market size, but lifestyle businesses generating $50,000-$100,000 in owner income are achievable. Exit opportunities are limited; this is typically owner-operator work rather than scalable enterprise.

Medium-Scale Regional Operations ($50,000-$500,000)

Investment Thesis: Capture market share through operational excellence, technology integration, and regional distribution networks, balancing growth with profitability.

Core Strategy: Invest in commercial production capacity: industrial ice machines capable of 5,000-20,000 pounds daily ($30,000-$100,000), automated packaging equipment ($20,000-$80,000), delivery fleet (2-4 vehicles at $25,000-$50,000 each), and warehouse/production facility lease. Target restaurant chains, grocery stores, event companies, and institutional buyers across a metro region or multi-county area.

Technology integration becomes competitive advantage. IoT-enabled equipment monitors production efficiency and predicts maintenance needs. Route optimization software reduces delivery costs. Quality control systems ensure consistency across high-volume production. These investments, totaling $30,000-$60,000, differentiate professional operators from unsophisticated competitors.

The revenue model emphasizes contracted, recurring business rather than opportunistic sales. Secure supply agreements with regional restaurant chains, grocery distributors, and institutional buyers. Volume creates negotiating power with suppliers while distribution efficiency enables competitive pricing without sacrificing margins.

Key Success Factors:

- Operational excellence—reliability becomes reputation

- Scalable systems allowing growth without proportional cost increases

- Contract relationships providing revenue predictability

- Cost management maintaining margins as volume scales

Realistic Expectations: Revenue potential of $500,000-$3,000,000 annually at maturity, with 15-25% gross margins typical. Growth is capital-intensive but achievable through reinvestment and debt financing. Exit opportunities include acquisition by larger players consolidating regional markets—the ice industry has active M&A driven by major players seeking geographic expansion.

Large-Scale Industrial Operations ($500,000+)

Investment Thesis: Leverage economies of scale, comprehensive automation, and market-leading technology for regional or national distribution dominance.

Core Strategy: Establish full-scale production facilities with capacity exceeding 50,000 pounds daily. Deploy comprehensive robotics for production, packaging, and palletizing. Implement enterprise resource planning systems integrating production, inventory, logistics, and customer management. Build or acquire distribution networks spanning multiple states or regions.

The competitive advantages are structural: per-unit costs below competitors through scale, capital reserves for acquisitions, and sophistication in operations and technology. Large operators serve national chains, develop private-label manufacturing, and potentially license technology to smaller producers.

Strategic priorities include acquisition-driven consolidation (the ice industry remains fragmented with hundreds of regional players), development of proprietary production technologies creating competitive moats, and exploration of adjacent opportunities like ice equipment leasing or ice-as-a-service models.

Key Success Factors:

- Financial resources to sustain multi-year investment cycles

- Management capability to operate complex, multi-site businesses

- Strategic vision balancing current operations with future positioning

- Acquisition execution capability to consolidate fragmented markets

Realistic Expectations: Revenue potential exceeding $10,000,000 annually, with 8-15% gross margins typical at scale. Lower margins reflect competitive pressure but are offset by volume. Exit opportunities include public markets (though few pure-play ice companies are publicly traded), acquisition by private equity or strategic buyers, or transition to next-generation family management.

Specialty Technology-Focused Operations ($25,000-$200,000)

Investment Thesis: Pioneer novel technologies and premium products for high-value market segments, accepting higher risk for potentially transformative returns.

Core Strategy: Focus on innovation rather than volume. Develop proprietary production techniques—perhaps flash-freezing methods creating unique textures, or mineral infusion creating functional ice products. Build intellectual property portfolios through patents and trade secrets. Target ultra-premium segments willing to pay significant premiums for differentiated products.

Examples include developing AI-powered production systems optimizing ice clarity and density, creating custom 3D-printed mold marketplaces connecting designers with ice producers, or pioneering sustainable production methods (solar-powered, zero-waste facilities) positioning for future regulatory environments.

The business model may emphasize licensing and technology sales over direct ice production. Develop proprietary systems, prove them in owned operations, then license to others. Or create specialized equipment sold to industry operators. Revenue streams diversify beyond commodity ice into higher-margin intellectual property.

Key Success Factors:

- Technical innovation capability, either in-house or through partnerships

- Understanding of market needs creating demand for innovation

- Intellectual property development protecting competitive advantages

- Patience to develop unproven concepts with uncertain timelines

Realistic Expectations: High variance in outcomes. Many specialty ventures fail to find sustainable markets. Successful ones may generate $200,000-$1,000,000+ annually with exceptional margins (50-80% for technology licensing). Exit opportunities include acquisition by established players seeking innovation or private equity interested in disruptive potential.

Emerging Opportunities: Where Innovation Meets Demand

Functional and Enhanced Ice

The wellness trend creates opportunities for ice products beyond simple cooling. Vitamin-infused ice cubes designed for health-conscious consumers. Mineral-enhanced varieties claiming hydration benefits. Caffeine-infused ice for cold brew coffee. Herbal or fruit-infused products adding subtle flavor.

The market remains nascent, with uncertain consumer willingness to pay premiums. However, parallel trends in functional beverages and premium food products suggest potential. Regulatory complexity around health claims requires careful navigation, but successful products could command 100-200% premiums over standard ice.

Ice-as-a-Service Models

Rather than selling ice, provide machines, maintenance, and supply for monthly fees. This creates recurring revenue streams and deeper customer relationships. Particularly attractive for high-volume customers (hotels, hospitals, large restaurants) where equipment investment, maintenance burden, and supply reliability concerns create demand for outsourced solutions.

Economics require careful modeling. Equipment costs, maintenance expenses, and supply logistics must be balanced against monthly revenue. However, successful implementation creates highly sticky customers with predictable revenue—valuable both operationally and in exit valuations.

Smart Ice and IoT Integration

Connected ice machines monitoring production quality, predicting maintenance needs, and optimizing energy consumption. Customer-facing applications tracking deliveries, managing orders, and providing usage analytics. Integration with building management systems for large facilities.

The technology exists; the question is market readiness and willingness to pay. Early adoption likely comes from sophisticated corporate buyers valuing operational efficiency and data visibility. As costs decline and benefits prove, adoption may spread to mid-market customers.

Climate-Adapted Production

In water-scarce regions, atmospheric water generation technology extracts moisture from air for ice production. In areas with unreliable electricity, solar-powered or hybrid systems ensure production continuity. In extreme climates, specialized insulation and cooling technologies maintain efficiency.

These adaptations address real constraints while creating competitive advantages. Operators solving local challenges—water scarcity, power reliability, extreme heat—build defensible positions resistant to conventional competitors unable to match specialized capabilities.

Pragmatic Action Plan: From Concept to Operation

Phase 1: Research and Validation (Weeks 1-8)

Market Analysis: Identify specific customer segments you could serve. Visit potential customers—bars, restaurants, event venues, grocery stores—and conduct informal interviews. What are their current ice sources? What problems do they experience? What would they value in ice products or service?

Analyze local competitors. Who supplies ice currently? What do they charge? What service levels do they provide? Where are gaps—geographic areas underserved, customer segments ignored, product varieties unavailable?

Research regulatory requirements. Food safety regulations vary by jurisdiction. What licenses, inspections, or certifications are required? What water quality standards must be met? What health department approvals are necessary?

Financial Modeling: Develop detailed cost projections for your chosen scale. Equipment costs, facility lease, utilities, insurance, transportation, packaging, water, initial inventory. Calculate break-even volumes. Model different pricing scenarios and their margin implications.

Assess realistic revenue potential. If targeting restaurants, how many could you serve in your geography? What volume would each require? At what price point? Build conservative, base-case, and optimistic scenarios.

Decision Point: Does the opportunity justify the investment and effort? Are margins sufficient to provide desired returns? Is market demand validated through customer conversations? Can you differentiate from existing competitors?

Phase 2: Business Setup (Weeks 9-16)

Legal and Regulatory: Establish business entity (LLC or corporation typically). Secure required licenses and permits. Obtain liability insurance and any specific food production insurance. Pass health department inspections.

Equipment and Facilities: Purchase or lease core equipment based on chosen scale. For small operations, quality commercial ice machine and reliable delivery vehicle. For larger ventures, industrial production equipment, packaging systems, storage capacity, and fleet vehicles.

Secure production facility meeting health and safety requirements. Consider location relative to customers, water access, power availability, and permitting feasibility.

Supply Chain: Establish water source (municipal, well, purification system). Secure packaging suppliers (bags, labels, ties). Arrange waste disposal. For larger operations, negotiate equipment maintenance contracts.

Phase 3: Customer Acquisition (Weeks 17-26)

Initial Outreach: Begin with direct sales to early-adopter customers. Offer trial deliveries at reduced rates to establish relationships and gather feedback. Focus on quality, reliability, and service rather than price competition.

Develop referral systems. Satisfied customers in hospitality or events sectors provide credibility for approaching similar prospects. Ask for testimonials and referrals explicitly.

Marketing Development: Create basic marketing materials—website, business cards, product photos. For premium positioning, invest in professional photography showing product quality. For B2B focus, develop case studies demonstrating reliability and value.

Consider targeted advertising in industry publications or associations (restaurant associations, event planner networks, catering companies). Attend local hospitality or food service trade shows.

Operational Refinement: Use early customers to refine operations. How long does production take? What’s optimal delivery scheduling? Where are quality issues emerging? What feedback do customers provide?

Iterate quickly on problems. In competitive markets with commodity alternatives, reliability and quality create differentiation. Early operational excellence builds reputation enabling growth.

Phase 4: Scale and Optimization (Months 7-18)

Growth Strategies: Expand customer base through proven channels. If direct sales work, hire additional salespeople. If partnerships prove effective, develop more. Focus on what’s working rather than experimenting with unproven approaches.

Consider geographic expansion. Once operations are refined in initial territory, adjacent regions offer lower-risk growth than distant markets requiring new infrastructure.

Evaluate adjacent opportunities. Can you serve related customer needs—perhaps event equipment rental, beverage consultation, or custom ice displays? Diversification within existing customer relationships often proves easier than entirely new customer acquisition.

Technology Integration: Invest in operational improvements. Route optimization software reducing delivery costs. Quality monitoring systems ensuring consistency. Customer relationship management tracking orders and enabling automated reordering.

For growing operations, consider automation where it improves economics. Automated packaging may justify investment at 5,000+ pounds daily production. Robotic handling systems make sense at larger scales. Calculate payback periods honestly—technology for technology’s sake destroys value.

Financial Management: Maintain strong financial controls as complexity increases. Understand unit economics intimately. Know exactly what each pound of ice costs to produce and deliver. Track margins by customer, product, and geography.

Build financial reserves for equipment replacement, market downturns, or unexpected challenges. Ice production equipment operates in harsh conditions; maintenance and replacement costs are significant and inevitable.

Phase 5: Strategic Positioning (Months 19-36)

Market Position Refinement: Are you competing on price, quality, service, or innovation? Ensure operations, marketing, and sales align with chosen positioning. Commodity players need operational efficiency. Premium brands need consistent quality and customer experience. Service differentiators need reliability and responsiveness.

Exit Planning or Long-term Strategy: For entrepreneurs seeking exits, position attractively for acquisition. Establish contracted revenue, demonstrate operational excellence, build competitive advantages (proprietary technology, exclusive contracts, brand recognition). Research comparable transactions to understand valuation parameters.

For those building long-term businesses, consider succession planning, professional management transition, or strategic partnerships. Family businesses must address next-generation involvement. Growth-focused operators should identify strategic partners or investment sources for expansion capital.

Innovation Initiatives: Reserve capacity for exploration. Test new products with existing customers. Experiment with service models. Evaluate emerging technologies. Balance core business stability with innovation positioning for future growth.

Critical Risk Analysis: The Ice Business Reality Check

Operational Risks and Points of Failure

Energy Cost Volatility

Energy represents 30-40% of ice production operating costs, creating devastating exposure to utility price fluctuations. A 20% electricity cost increase directly translates to 6-8% margin compression in an industry where net margins typically run 8-15% for larger operators and 15-25% for smaller ones.

Failure Scenarios:

- Unexpected utility rate increases making contracts unprofitable mid-term

- Peak demand charges in summer months (when ice demand is highest) creating cost spikes

- Equipment inefficiency compounding energy costs as machines age

- Geographic markets with deregulated energy creating price unpredictability

Mitigation Limitations: While solar power and energy-efficient equipment offer partial solutions, they require substantial capital investment (5-8 year payback periods). Small operators often lack capital for these investments precisely when they’d provide most protection. Fixed-price energy contracts exist but typically command premiums and have limited terms (1-3 years), merely deferring rather than eliminating risk.

Equipment Failure and Maintenance

Ice production equipment operates continuously in harsh conditions—extreme cold, high humidity, constant freeze-thaw cycles. Failure rates are significant, and replacement costs are substantial.

Failure Scenarios:

- Compressor failure requiring $5,000-$25,000 replacement (depending on scale)

- Refrigerant leaks creating both immediate repair costs and potential environmental penalties

- Water filtration system failures affecting product quality across entire production runs

- Automated packaging equipment breakdowns during peak demand periods

- Delivery vehicle refrigeration failures destroying product in transit

The Maintenance Trap: Preventive maintenance requires discipline and capital reserves many operators lack. Deferred maintenance creates cascading failures—one component breakdown stresses related systems, accelerating their deterioration. The brutal economics: a $2,000 maintenance item deferred can become a $15,000 emergency replacement plus lost revenue during downtime.

Seasonal Cash Flow Volatility

Ice demand can fluctuate 300-400% between winter lows and summer peaks. This creates operational nightmares:

Winter Challenges:

- Fixed costs (facility lease, base utilities, insurance, debt service) continue while revenue plummets

- Equipment sitting idle still requires maintenance

- Staff retention difficult if hours are cut dramatically

- Cash reserves depleted covering negative cash flow months

Summer Challenges:

- Equipment and staff stretched beyond optimal capacity

- Quality control harder during maximum production pressure

- Delivery logistics stressed by volume, creating service failures

- Customer acquisition costs wasted if you can’t reliably serve peak demand

The Failure Pattern: Undercapitalized operators survive first winter on initial reserves, scale up for second summer, then fail during second winter when reserves are exhausted and summer revenue didn’t build sufficient buffer. This pattern claims many startups in years 2-3.

Water Quality and Regulatory Compliance

Ice is food. Regulatory standards are stringent, inspections frequent, and violations severe.

Critical Requirements:

- Regular water quality testing (bacterial, chemical, mineral content)

- Health department inspections with unannounced visits

- HACCP (Hazard Analysis Critical Control Points) compliance

- Proper sanitation protocols and documentation

- Employee health and hygiene standards

- Equipment cleaning and maintenance logs

Failure Scenarios:

- Bacterial contamination requiring production stoppage and product recall

- Failed health inspections resulting in temporary closure

- Regulatory violations creating legal liability

- Equipment contamination from inadequate cleaning

- Employee health violations (working while ill) contaminating product

The Compliance Cost: Meeting standards requires time, attention, and money. Testing costs $200-$500 monthly. Proper cleaning takes hours daily. Documentation creates administrative burden. For small operators, compliance represents significant operational overhead that commodity pricing may not support.

Market Competition and Pricing Pressure

The ice industry combines high competition with commodity economics in traditional segments.

Competitive Threats:

- Established players with scale advantages and lower cost structures

- New entrants with low barriers to entry (especially in commodity segments)

- Grocery stores increasingly viewing ice as loss leader, pricing at or below cost

- Large customers (restaurant chains, distributors) exerting pricing pressure

- Home ice makers improving in quality, reducing some market segments

The Margin Squeeze: Commodity ice pricing is largely transparent—customers know market rates. Differentiation is difficult in standard products. Service quality matters but often isn’t sufficient to command significant premiums. Result: persistent pressure on margins requiring operational excellence to maintain profitability.

Customer Concentration Risk

Small and medium operators often rely heavily on few large customers.

Danger Zones:

- Top customer representing >25% of revenue creates existential risk if lost

- Contract renewals with major customers becoming periodic crises

- Customer financial difficulties creating receivables risk

- Seasonal customers (event companies, seasonal restaurants) creating concentration within already volatile demand

Failure Pattern: Operator secures major contract representing 40% of revenue. Builds capacity to serve it. Customer switches to competitor offering 5% lower price. Operator suddenly has excess capacity, insufficient revenue covering fixed costs, and insufficient working capital to survive while rebuilding customer base.

Geographic and Climate Risk

Ironically, climate change creates both opportunities and risks.

Emerging Risks:

- Extreme weather events disrupting production and distribution

- Water restrictions during droughts affecting production ability

- Increasing regulations on water usage and energy consumption

- Infrastructure failures (power outages) during extreme weather precisely when demand peaks

- Flooding or storm damage to facilities and equipment

The Adaptation Cost: Building resilience requires investment: backup generators, water storage capacity, structural improvements. These costs hit precisely when margins are compressed by other climate-related pressures.

Environmental Impact: The Uncomfortable Truth

Energy Consumption and Carbon Footprint

Ice production is energy-intensive. The physics are unforgiving—removing heat energy from water requires substantial electricity input.

Scale of Impact: A medium-sized ice operation producing 10,000 pounds daily consumes 3,000-5,000 kWh monthly. At U.S. average carbon intensity (0.92 pounds CO₂ per kWh), this generates 33,000-55,000 pounds of CO₂ annually—equivalent to 3-5 passenger vehicles.

Large industrial operations producing 100,000+ pounds daily have carbon footprints comparable to small manufacturing facilities. The industry collectively generates millions of tons of CO₂ annually.

The Efficiency Paradox: Modern equipment has improved efficiency 20-30% over older systems, but overall energy consumption continues rising as production volumes grow. Efficiency gains are real but insufficient to offset industry expansion.

Renewable Energy Limitations: Solar power offers genuine carbon reduction but faces practical constraints:

- Works only in sunny regions with favorable utility policies

- Requires substantial upfront capital (typical payback: 5-8 years)

- Production often peaks when solar generation is highest (summer days) but ice is also needed at night and in winter

- Battery storage to truly match production with solar generation remains economically prohibitive for most operators

Realistic assessment: solar can provide 30-50% of energy needs in ideal conditions, reducing but not eliminating carbon footprint.

Water Consumption and Resource Impact

Water usage extends beyond the obvious (water frozen into ice).

Direct Water Use:

- Product water (frozen into ice): 8.34 pounds per gallon

- Cooling water for refrigeration systems: 2-4 gallons per gallon of product water

- Cleaning and sanitation: 50-200 gallons daily depending on operation scale

- Total water consumption: roughly 3-5 gallons per gallon of ice produced

Hidden Water Impacts:

- Water treatment (filtration, purification) generates wastewater requiring disposal

- Reverse osmosis systems (used for premium ice) waste 3-5 gallons for every gallon purified

- Cleaning chemicals entering wastewater streams

- Infrastructure water (employee facilities, general facility maintenance)

Regional Context Matters: In water-abundant regions (Pacific Northwest, Great Lakes, Northeastern U.S.), water consumption is less problematic. In water-stressed areas (Southwest U.S., parts of California, Middle East), ice production competes with agriculture and residential use for scarce resources.

Plastic Packaging Pollution

Standard ice bags are plastic—typically polyethylene. The industry generates massive plastic waste.

Scale of Problem: A medium operation selling 5,000 bags monthly generates roughly 1,200 pounds of plastic packaging annually. Nationally, the U.S. ice industry produces tens of millions of plastic bags yearly.

Most ice bags aren’t recycled:

- Contamination from water/moisture reduces recycling viability

- Thin plastic film is difficult to recycle economically

- Consumer recycling rates for any plastic film are extremely low (typically <5%)

- Result: the vast majority ends in landfills or, worse, as environmental litter

Alternative Packaging Reality: Biodegradable or compostable alternatives exist but face challenges:

- Cost premiums of 50-200% over conventional plastic

- Performance limitations (less puncture-resistant, shorter shelf life)

- Requires proper composting infrastructure (not landfill) to actually biodegrade

- Industrial composting facilities accepting these materials are limited

- Consumer confusion about proper disposal

Current biodegradable packaging often represents “greenwashing”—technically compostable but practically ending in landfills where they don’t actually biodegrade due to lack of oxygen and proper microbial conditions.

Refrigerant Environmental Impact

Ice production equipment uses refrigerants. While older, ozone-depleting refrigerants (CFCs, HCFCs) are being phased out, replacements have their own issues.

Current Refrigerants:

- HFCs (hydrofluorocarbons): No ozone depletion but high global warming potential (GWP)—hundreds to thousands of times more potent than CO₂

- HFOs (hydrofluoroolefins): Lower GWP but more expensive and performance limitations

- Natural refrigerants (ammonia, CO₂): Lower GWP but safety concerns, equipment complexity, and higher capital costs

The Leak Problem: Equipment leaks are inevitable. Seals deteriorate, connections loosen, accidents occur. Even well-maintained systems leak 2-10% of refrigerant charge annually. Poorly maintained systems leak far more.

Each pound of leaked HFC refrigerant equals 1,000-4,000 pounds of CO₂ equivalent warming impact. A medium-sized system containing 50-100 pounds of refrigerant can have massive climate impact if poorly maintained.

Transportation and Distribution Emissions

Ice is heavy, bulky, and requires refrigerated transport.

Logistics Carbon Cost:

- Delivery trucks consume 6-12 MPG depending on size and conditions

- Refrigeration units add 20-30% to fuel consumption

- Ice’s weight-to-value ratio is terrible—transporting heavy product with relatively low retail value

- Typical delivery routes: 50-150 miles daily

- Carbon footprint: 0.5-2 pounds CO₂ per pound of ice delivered (depending on distance and route efficiency)

The Efficiency Challenge: Route optimization helps but faces limits. Customers require specific delivery windows. Ice melts, limiting how long it can sit on trucks. Geographic dispersion of customers creates inherently inefficient routes.

Electric delivery vehicles offer future carbon reduction but currently face limitations (cost, range, refrigeration power draw reducing range further, charging infrastructure).

Water Resource Challenges: Regional Variations

Water-Abundant Regions: Hidden Costs

Even in water-rich areas, ice production has impacts:

Infrastructure Stress:

- Municipal water systems sized for average demand face peak loads from ice producers

- Treatment facility capacity consumed by high-volume commercial users

- Sewer systems handling wastewater discharge from cleaning and purification

Opportunity Costs: Water used for ice could serve other economic purposes. In competitive markets, water allocation decisions have real economic implications.

Water-Scarce Regions: Fundamental Conflicts

In arid regions, ice production faces ethical and practical challenges.

Competition with Essential Uses:

- Residential consumption (drinking, sanitation)

- Agricultural irrigation

- Industrial processes

- Environmental flows (maintaining ecosystem health)

Regulatory Risk: Water restrictions during droughts can directly prohibit or severely limit ice production. California drought restrictions, for example, have periodically impacted commercial water users.

Cost Escalation: Water pricing in scarce regions increasingly reflects true scarcity. Tiered pricing structures penalize high-volume users. Long-term trends point toward continued water cost increases in arid regions.

The Fundamental Question: Is producing ice—essentially a convenience product—a justifiable use of scarce water? In extreme scarcity scenarios, society may decide it isn’t. Las Vegas or Phoenix ice producers face existential questions about business viability under future water restriction scenarios.

Groundwater Depletion

Operators using well water may contribute to aquifer depletion.

The Problem: Many aquifers are drawn down faster than natural recharge. The Ogallala Aquifer (U.S. Great Plains) is being depleted at unsustainable rates. Individual operators may view well water as “free,” but collectively they’re consuming non-renewable resources.

Long-term Impact:

- Declining water tables increasing pumping costs

- Well failures requiring deeper, more expensive drilling

- Regional water availability declining for all users

- Potential future regulations restricting groundwater extraction

Honest Assessment: Should You Enter This Industry?

The Uncomfortable Reality

Ice production has genuine environmental costs that aren’t fully reflected in pricing. Energy consumption, carbon emissions, water usage, and plastic waste are externalities costs borne by society rather than producers or consumers.

Future regulatory trends likely increase these costs:

- Carbon pricing or increased energy costs

- Water usage restrictions and pricing

- Plastic packaging bans or taxes

- Refrigerant regulations requiring expensive equipment upgrades

Operators ignoring these trends face future regulatory shocks. Those preparing face competitive disadvantages versus less responsible competitors today.

For Prospective Entrepreneurs: Critical Questions

Environmental Conscience Check: Can you operate this business consistent with your environmental values? If you care deeply about climate change or environmental impact, ice production creates cognitive dissonance. The physics demand energy consumption. Current economics favor plastic packaging. These aren’t easily resolved.

Risk Tolerance Assessment: The industry has numerous failure points: equipment breakdown, customer loss, seasonal cash flow gaps, energy cost spikes, regulatory violations, competition. Success requires capital reserves, operational excellence, and some luck. Most small businesses fail within five years—ice businesses face all typical small business risks plus industry-specific challenges.

Capital Reality: Undercapitalization kills more ice businesses than any other factor. You need reserves for:

- Equipment replacement (not if, but when)

- Seasonal cash flow gaps (winter losses)

- Working capital (receivables, inventory, operating expenses)

- Emergency repairs

- Marketing and customer acquisition

Rule of thumb: have 6-12 months operating expenses in reserves beyond initial equipment investment.

Market Honesty: Can you differentiate, or are you entering commodity competition? Unless you have genuine advantages—proprietary technology, exclusive contracts, operational excellence, or premium positioning—you’re competing on price against established players with superior cost structures. That’s a losing game.

Paths Forward: Responsible Operation

If proceeding despite these risks and concerns:

Minimize Environmental Impact:

- Invest in most efficient equipment available, even at cost premium

- Implement solar power where viable

- Explore biodegradable packaging aggressively as economics improve

- Optimize logistics to minimize transportation emissions

- Maintain equipment religiously to prevent refrigerant leaks

- Use water recycling where feasible

- Choose renewable energy providers where available

Build Resilience:

- Maintain substantial financial reserves

- Diversify customer base to reduce concentration

- Develop premium segments less vulnerable to price competition

- Build strong customer relationships creating switching costs

- Plan for seasonal volatility from day one

- Budget conservatively, hope for the best but plan for challenges

Stay Informed:

- Monitor regulatory trends affecting water, energy, refrigerants, packaging

- Anticipate rather than react to regulatory changes

- Build relationships with regulators, demonstrating commitment to compliance

- Consider industry association membership for collective advocacy

Eyes Wide Open

The ice business offers real opportunities but demands realistic assessment of significant risks and environmental costs. Success isn’t impossible but requires capital, operational excellence, market positioning, and honestly good luck.

Environmental impacts are real and growing in regulatory visibility. Future operators face increasing pressure to internalize currently externalized costs. Building these costs into financial planning today avoids unpleasant surprises tomorrow.

Anyone entering this industry should do so with clear understanding of risks, genuine commitment to operational excellence, sufficient capital reserves, and realistic expectations about both financial returns and environmental responsibility.

The ice business isn’t inherently immoral or impossible, but it’s far from the simple opportunity it might appear. Proceed carefully, plan conservatively, and maintain honest awareness of both business risks and environmental costs.

Conclusion: Cold Calculations for Hot Opportunities

The ice business defies simple categorization. It’s simultaneously a mature commodity industry and an emerging premium market. It’s both traditional manufacturing and technology-enabled innovation. It serves essential needs while creating space for artisanal craftsmanship.

Opportunities exist across scales, from artisan producers serving craft cocktail bars to industrial operations distributing millions of pounds monthly. Technology—robotics, AI, 3D printing, sustainable energy—creates both competitive threats and strategic opportunities. Market dynamics vary dramatically by geography, creating localized advantages for those understanding regional specifics.

Success requires matching opportunity to capability and capital. Small operators thrive on quality, relationships, and specialization. Medium players compete on operational excellence and technology integration. Large enterprises leverage scale, automation, and market power. Specialists pioneer innovation in products or processes.

The fundamental question isn’t whether opportunity exists—clearly it does, evidenced by steady growth and ongoing innovation. Rather, the question is whether you have the specific capabilities, capital, and commitment to capture available opportunities against incumbent competitors and emerging threats.

For those answering affirmatively, the ice business offers stable demand, multiple differentiation paths, and clear scaling opportunities. It won’t make you wealthy overnight, but it can build profitable, sustainable enterprises for entrepreneurs willing to think creatively about serving fundamental needs in differentiated ways.

The ice business persists not despite refrigeration ubiquity, but because of gaps between universal need and household capacity. Those gaps create opportunity. Your task is identifying which gaps you’re uniquely positioned to fill.

{kind=link}

{kind=link}

{kind=link}

{kind=link}