PREAMBLE

This Intelligence Brief is published by the Creator Economy Intelligence Group as a synthesised, evidence-grounded assessment of the global creator and social media economy as of Q1 2026. It draws on proprietary platform data, industry research, creator income surveys, AI tool analytics, and cross-sector convergence analysis to provide a comprehensive strategic picture.

The Brief is designed for three primary audiences: (1) creators and creator-entrepreneurs seeking evidence-based strategy; (2) brands, agencies, and investors allocating resources to the creator economy; and (3) platform operators and technology providers building infrastructure for the next phase of creator-driven commerce.

| SCOPE | This document covers market scale and trajectory, creator income realities, platform dynamics, AI tool strategy, regulatory context, cross-sector convergence with gaming, film, and television, the AI vs. human influencer landscape, and short-, medium-, and long-term horizon projections to 2035. |

| METHODOLOGY | Findings are drawn from: Influencer Marketing Hub 2025–2026 datasets; TikTok 2026 Trend Report; Goldman Sachs creator economy projections; Ogilvy Influencer Trends 2026; Twimbit Virtual Influencer State 2025; BCG Global Gaming Survey 2026; Creator IQ Brand Report; and primary case study analysis across 40+ creator businesses. |

All financial figures are presented in USD unless otherwise noted. UK/EU figures are denominated in GBP where sources specify. Year-over-year comparisons reference full-year 2024 against 2025 actuals or 2026 projections as available.

As usual references and supporting documents: Creator Artifacts

EXECUTIVE SUMMARY

The creator economy is no longer an emerging sector — it is a structural pillar of the global media, commerce, and technology landscape. The following brief documents its scale, dynamics, risks, and strategic implications across a ten-year horizon.

Five Headlines That Define the 2026 Creator Economy:

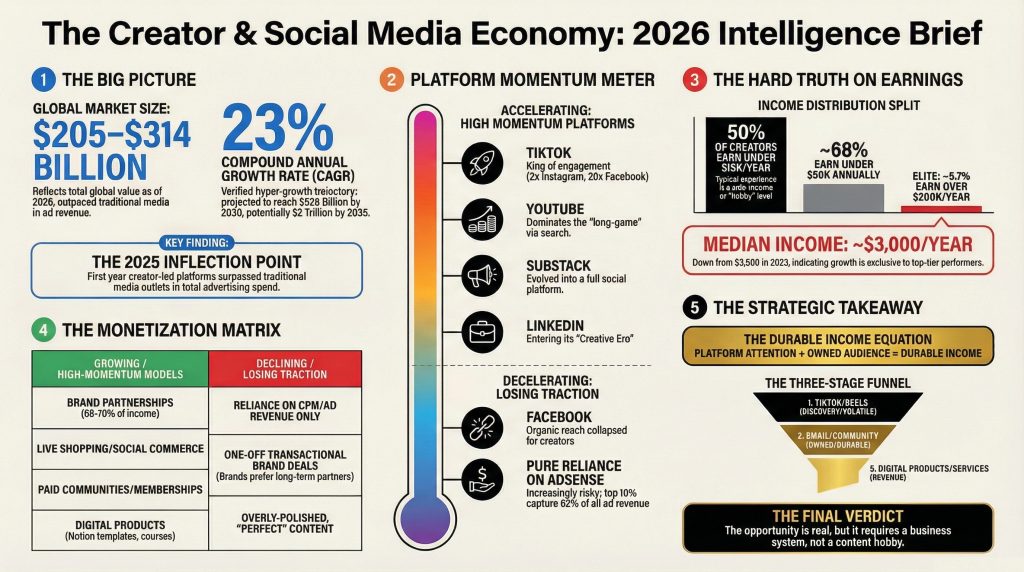

- The market is enormous but deeply unequal. Valued at $205–314 billion in 2026 and projected toward $2 trillion by 2035, the creator economy simultaneously rewards its top 10% with 62% of all ad revenue while leaving the median creator earning approximately $3,000 per year.

- AI has crossed from experimental to operational. 84% of creators now use AI tools; brands deploying full AI stacks report 38% annual revenue growth versus partial adopters. AI is no longer a competitive differentiator — it is table stakes.

- Platforms have structurally converged. YouTube surpassed Netflix in US television share in 2025. TikTok entered the Hollywood value chain at Sundance 2026. Gaming studios now operate as creator payout platforms. The boundary between entertainment industry and social media has dissolved.

- Human creators are not being replaced by AI — they are licensing themselves to it. Khaby Lame’s $975M AI avatar deal signals that top human creator identity is now a bankable asset class, not a headcount. Commodity content will be AI-generated; trust and lived experience remain human moats.

- The dominant risk is not competition — it is dependency. Any creator or brand building exclusively on a single rented platform, whether TikTok, Instagram, or YouTube, is one algorithm change or regulatory ruling from structural disruption. Owned audiences (email, community, IP) are the only durable infrastructure.

| $314B Market Size 2026 ↑ 22% CAGR | 207M Active Creators Global | $32.6B Brand Influencer Spend 2026 est. | $3K/yr Median Creator Income Down from $3.5K |

SECTION 1: MARKET SCALE & TRAJECTORY

1.1 Global Market Sizing

The global creator economy is currently valued at $205–314 billion depending on methodology. The wide range reflects differing definitions the lower bound captures direct creator income and platform-mediated brand spend; the upper bound includes the full ecosystem of creator tooling, infrastructure, agencies, and adjacencies. For strategic purposes, the consensus figure used by Goldman Sachs and Influencer Marketing Hub approximately $250 billion in 2026 represents the most defensible midpoint.

The sector is on a confirmed hypergrowth trajectory. Independent forecasts place the market at $528 billion by 2030 and potentially $2 trillion by 2035, driven by platform maturation, AI-enabled content scale, and the integration of creator commerce into mainstream retail infrastructure. The CAGR across all major forecasts consistently lands between 22–23.4%, making the creator economy one of the fastest-growing economic sectors globally — outpacing cloud computing, fintech, and most consumer goods categories.

| STRUCTURAL INFLECTION | 2025 marked the first year that creator platforms (Instagram, TikTok, YouTube) surpassed traditional media in advertising revenue. This is not a trend — it is a structural shift in where commercial attention is priced. |

1.2 Creator Population & Demographics

There are now over 207 million active content creators globally, with 162 million in the US alone of whom 45 million consider themselves professional creators. Amateur creators represent 75.1% of the global market, confirming that the creator economy remains a democratised, accessible entry point despite concentrated earnings at the top.

| Segment | Global Estimate | US Share | Professional Status |

| Total Active Creators | 207 million+ | 162 million | — |

| Professional Creators | ~45 million | ~28 million | Treat content as primary business |

| Amateur / Hobbyist Creators | ~162 million | ~134 million | Side income or passion-driven |

| Nano Influencers (1K–10K) | Largest single cohort | — | Growing fastest in brand deals |

| Mega Influencers (1M+) | <1% of total | — | Declining share of brand spend |

1.3 Influencer Marketing Market

The influencer marketing sector specifically representing brand-funded creator activity reached $32.55 billion in 2026. 94% of brands now report that creator content outperforms traditional digital advertising in measurable ROI. This has accelerated the shift from campaign-based transactional partnerships to long-form co-creation relationships, with brands moving spend from mega-influencers toward nano and micro creators for authenticity, engagement depth, and cost efficiency.

TikTok Shop alone generated $26.2 billion in Gross Merchandise Value in H1 2025, growing 120% year-over-year, establishing that the commerce infrastructure layered on top of creator content has now reached genuine scale. Live social commerce — the intersection of creator broadcasting and real-time retail — is normalising in UK and EU markets following proven adoption patterns in Southeast Asia.

SECTION 2: CREATOR INCOME REALITIES

2.1 The Income Distribution Problem

The most important analytical truth about the creator economy is one that is systematically obscured by popular media: the income distribution is deeply, structurally skewed. The average creator income of approximately $44,000 per year in the US creates a false impression of accessibility. The median creator income a more honest signal is approximately $3,000 per year, down from $3,500 in 2023. The modal experience is sub-$15,000.

| Income Bracket | % of Creators | Trend vs. 2023 |

| Under $15,000/year | >50% | Stable — entry-level saturation |

| Under $50,000/year | ~68% | Growing — income concentration accelerating |

| $50,000–$75,000/year | ~13.5% | Flat |

| Over $100,000/year | ~4% | Slight decline |

| Over $200,000/year | ~5.7% | Down from 7.2% in 2023 |

| KEY INSIGHT | The top 10% of creators captured 62% of all ad revenue in 2025, up from 53% in 2023. Income concentration is accelerating, not moderating. The creator economy is enormous in total scale but deeply inequitable in distribution — a structural characteristic, not a temporary imbalance. |

2.2 Revenue Streams & Income Architecture

Brand partnerships dominate creator income, representing 68–70% of total creator revenue. This creates systemic fragility: creators dependent on brand deals are exposed to brand sentiment cycles, platform algorithm shifts, and advertiser budget consolidation. The creators earning $132,000+ annually share a common characteristic they have diversified across at least three revenue streams and treat their content as a business system, not a creative output.

The most resilient income architectures in 2026 combine: (1) platform ad revenue as a base signal layer; (2) brand partnerships for amplified income; (3) owned digital products (courses, templates, communities) for margin; and (4) email list and direct-to-audience commerce as the non-rented layer. Creators with this structure report median incomes 4–7x higher than those dependent on any single revenue channel.

2.3 Creator Personas & Stakeholder Profiles

| Persona | Followers | Annual Income | Primary Revenue | Key Risk |

| Hobbyist | <10K | <$15K | Affiliates, gifts | Monetisation friction |

| Nano/Micro Influencer | 1K–100K | $15K–$75K | Brand deals, affiliates | Undervalued by brands |

| Professional Creator | 100K–1M | $75K–$200K+ | Multi-stream | Burnout, algorithm dependency |

| Creator-Entrepreneur | Varies | $200K–$1M+ | Products, licensing, SaaS | Operational complexity |

| Mega Influencer | 1M+ | $1M+ | Enterprise brand deals | Declining relatability premium |

SECTION 3: PLATFORM DYNAMICS & ALGORITHM INTELLIGENCE

3.1 TikTok — Discovery Commerce & Algorithm Shifts

TikTok’s strategic positioning in 2026 is best understood through the concept of Discovery Commerce: content that creates purchase intent rather than capturing existing intent. This is fundamentally different from search-based commerce and represents TikTok’s competitive moat against Amazon, Google, and traditional retail.

TikTok announced significant algorithm changes in late February 2026 that alter distribution mechanics in ways creators must understand. The most critical shift is the elevation of Sends Per Reach (SPR) the rate at which viewers share a video with someone else as the primary virality signal, replacing raw view count. A video shared to a friend carries dramatically higher algorithmic weight than a passive watch.

| ALGORITHM SIGNAL | TikTok’s 2026 Trend Report identifies three durable macro content themes: Reali-TEA (authentic, unfiltered behind-the-scenes content), Curiosity Detours (niche expertise rabbit holes), and Emotional ROI (content that ties genuine feeling to a product or transformation). These are building frameworks, not passing trends. |

Critical strategic note: TikTok ban dynamics in the US remain unresolved as of Q1 2026. Any TikTok-dependent business without a parallel presence on Instagram Reels and YouTube Shorts carries unquantified regulatory risk. Email list building from day one is non-negotiable: a TikTok audience is rented infrastructure, not owned capital.

3.2 YouTube — The Compounding Asset Engine

YouTube’s structural advantage over short-form competitors is temporal compounding: a video posted three years ago continues generating revenue today. YouTube CEO Neal Mohan confirmed in early 2026 that YouTube remains the ‘original and largest creator economy’ and is expanding its monetisation infrastructure — Partner Program, Shopping integrations, and AI-powered tools. YouTube now represents 13% of all US television time, surpassing Netflix, Disney+, and every other streaming service.

The highest-performing YouTube business models in 2026 are: search-optimised tutorial channels in B2B niches (finance, legal, software, healthcare) commanding CPMs of $8–$35 versus $1–$3 for entertainment content; the YouTube-to-digital-product funnel (tutorial content to free resource to paid course or template); and the podcast-to-YouTube pipeline, which YouTube is now actively promoting as a category.

3.3 Platform Positioning Matrix

| Platform | Primary Strength | Creator Revenue Model | 2026 Strategic Priority |

| TikTok | Discovery Commerce, virality | Shop affiliates, Creator Fund, brand deals | Live commerce EU/UK expansion |

| YouTube | Search compounding, long-form | AdSense, memberships, Shopping | Podcast category, AI tools |

| Visual brand, Reels reach | Brand deals, Subscriptions, Shop | AI Reels editing, broadcast channels | |

| B2B, professional authority | Thought leadership → consulting/SaaS | Newsletter + algorithmic discovery | |

| Substack | Owned audience, subscription | Paid newsletters, Recommendations | Social layer, podcast integration |

SECTION 4: AI STRATEGY — TOOLS, WORKFLOWS & COMPETITIVE DYNAMICS

4.1 AI Adoption Landscape

AI has crossed from competitive advantage to operational baseline. 84% of creators now use AI tools, with over half reporting time savings of 53.7%. Over 91% of professional creators use generative AI to scale output. Brands deploying full AI stacks are reporting up to 38% annual revenue growth versus partial adopters.

The strategic imperative is not which AI tools to use — it is how to deploy them in the correct sequence. The discipline of AI adoption for creators follows a three-stage hierarchy: (1) Eliminate replace pure time drains with zero creative value (transcription, captioning, formatting, scheduling); (2) Augment enhance the creative process through ideation, first drafts, and variation testing; (3) Scale replicate proven content formats at volume through repurposing, faceless variants, and multilingual adaptation.

4.2 The AI Tool Stack by Creator Scale

| Scale Tier | Monthly Cost | Core Tools | Primary Goal |

| Solo (0–10K followers) | £30–£80/mo | ChatGPT, Canva AI, Buffer, Opus Clip | Replace 8–10 hrs/week of manual work |

| Medium (10K–100K) | £150–£400/mo | + Descript, Castmagic, Modash, ActiveCampaign AI | 3x content output, no headcount addition |

| Large (100K+ / £10K+/mo) | £500–£2,000/mo | + HeyGen, AdCreative.ai, Jasper, n8n automations | Operate as a media company with team of 3–5 |

4.3 Featured Tool Intelligence: Virlo

Virlo has been independently rated the leading TikTok trend discovery and prediction platform for 2025–2026. Serving over 40,000 users who have collectively generated 9 billion views, Virlo uniquely integrates three functions normally requiring separate tools: predictive trend monitoring, cross-platform analytics (TikTok + YouTube Shorts), and AI content generation using Veo 3 video technology, ElevenLabs voice synthesis, and AI scriptwriting.

| TOOL NOTE | Virlo plans range from $20.30/mo (Researcher) to $195.30/mo (Scale), with 500 free credits on signup sufficient to test one complete trend scan cycle. The Pro tier at $104.30/mo adds AI script generation, audio synthesis, and Runway/Veo 3 video generation — the only single tool combining all three functions. |

4.4 The Authenticity Paradox

The central tension of AI adoption is commercially quantifiable: 30% of consumers are less likely to purchase from brands using purely AI-generated content. Consumer enthusiasm for AI content has declined from 60% to 26% over two years. The winning formula validated across case studies is the ‘AI bones, human voice’ model: AI handles structure, research, formatting, and distribution; the human provides opinion, lived experience, and personality. This architecture is the creative moat that pure AI cannot replicate.

SECTION 5: AI INFLUENCERS vs. HUMAN CREATORS

5.1 The Competitive Landscape

The AI influencer market is a live competitive force in 2026, not a future concern. 62% of human creators are already concerned about increased competition from virtual influencers, and 59% are worried about long-term relevance. The concern is commercially rational: virtual creators frequently outperform human influencers in raw engagement metrics because they are algorithmically optimised, always available, never controversial, and infinitely scalable.

TikTok’s position is unambiguous under its 2026 AIGC framework: AI creativity is supported and permitted when disclosed; AI impersonation is prohibited. Misleading or unlabelled AI influencer content results in reach suppression and content removal. The regulatory direction across EU and UK markets is toward mandatory AI content labelling creating a disclosure compliance requirement that will become a structural cost of AI creator operations.

5.2 Competitive Positioning Matrix

| Dimension | AI / Virtual Influencer | Human Creator |

| Scale & Speed | Unlimited content at zero marginal cost | Time-constrained; burnout risk |

| Brand Safety | Zero scandal risk; always on-brand | Reputational exposure; unpredictable |

| Purchase Intent | Lower — audiences discount AI recommendations | Higher — peer trust effect drives conversion |

| Emotional Connection | Limited; audiences identify non-human signal | Core irreplaceable moat at depth |

| Multilingual Scale | Instant 175+ language deployment | Localisation cost and time barrier |

| Regulatory Risk | Rising — EU/UK labelling mandates tightening | Lower compliance burden if disclosed |

5.3 The Five Human Creator Moats

Ogilvy’s 2026 Influencer Trends Report identifies the equilibrium: AI influencers will supplement human creators with scale and speed, while AI Agents will execute operations and analyse performance. The practical prediction is that AI takes over commodity content (product demos, FAQs, standardised tutorials) while humans dominate trust-dependent content (personal recommendations, vulnerable storytelling, niche expertise). The five moats AI cannot replicate:

- Lived experience — credentials, context, and scars that can only come from actually doing the thing

- Real-time cultural fluency — the ability to feel a cultural moment and respond with genuine emotion, not optimised imitation

- Community co-creation — audiences who feel they are building something with the creator, not consuming from them

- Moral accountability — humans bear consequences; AI bears none, and audiences increasingly understand this

- Legal personhood — AI influencers cannot enter contracts, hold copyright, or provide FTC-compliant endorsements as principals

5.4 The Khaby Lame Precedent

The most instructive single data point of 2026: Khaby Lame TikTok’s most-followed human creator globally signed a $975 million licensing deal in January 2026 authorising the creation of AI-generated multilingual and multi-version content of his likeness, projected to generate $4 billion in annual sales. This reframes the entire AI vs. human creator debate.

| STRATEGIC REFRAME | The most valuable human creators will not fight AI — they will license themselves to AI at extraordinary valuations. Creator identity, at scale, is now a bankable asset class with leverage multiples previously reserved for major entertainment IP. This is the end-state of the human-AI creator relationship for top-tier operators. |

SECTION 6: CROSS-SECTOR CONVERGENCE — GAMING, FILM & TV

6.1 The Convergence Thesis

2026 marks the inflection point at which the creator economy, gaming, film, and television stop being parallel industries and begin operating as a single attention market. Netflix now defines its competitive landscape as the ‘global entertainment market’ one pool of attention competed for simultaneously by streaming services, social media, user-generated content, gaming, and creator platforms. The boundary lines have dissolved.

6.2 Gaming × Creator Economy

Gaming is the most structurally advanced convergence point. Fortnite and Roblox alone paid out $1.5 billion to UGC creators in 2025 — a creator economy operating entirely within game engines. BCG’s 2026 Global Gaming Survey found that 40% of gamers now watch gaming content online, establishing that watching others play has become as culturally valuable as playing itself. Advertisers are treating in-game creators as a mainstream media channel equivalent to television spots, layered with precision targeting and creator trust.

| Gaming Platform | Creator Economy Role | Revenue Potential |

| Roblox | Virtual item creation, world design, avatar accessories | $936B metaverse market by 2030 |

| Fortnite Creative | Brand activations, virtual events, map design | $1.5B UGC payout combined with Roblox |

| VRChat | Virtual worlds, avatar commissions, events | 30% of users report income from VR activities |

| GTA VI (2025/2026) | Streaming content, clip culture, virtual economy | Potentially largest entertainment launch in history |

6.3 Film & TV × Creator Economy

TikTok’s presence at Sundance Film Festival 2026 marks the clearest institutional signal that the platform has formally entered the Hollywood value chain as a co-equal partner in film discovery, talent development, and audience building — not merely a promotional tool. TikTok co-hosted the Sundance creator welcome event with A24, the most prestigious independent studio in the world, deploying 10 embedded creator-correspondents to produce real-time content from the festival.

The Warner Bros. Spotlight Model already live at scale illustrates the emerging four-party value exchange: studios pay TikTok for distribution; TikTok pays creators in non-cash incentives (profile frames, filters, merchandise, red-carpet access); creators receive organic reach amplification; audiences receive curated fan content. The House of the Dragon Season 2 campaign generated 260,000+ fan-created posts in two weeks pre-premiere via this mechanic.

The most significant structural shift: for the first time, premium Hollywood talent is moving toward creator platforms rather than away from them. YouTube represents the largest share of US television usage at 13% of all TV time, outpacing Netflix, Disney+, and every other streaming service. Studios are building creator-led IP franchises rather than hiring creators as promotional vehicles the creator is now the IP.

SECTION 7: MONETISATION FRAMEWORKS & DIGITAL COMMERCE

7.1 Digital Product Platform Intelligence

The digital product platform market has consolidated around distinct models serving different creator stages. The correct platform selection is not about which is best in the abstract it is about matching creator stage, product type, and technical appetite to the right infrastructure.

| Platform | Best For | Fee Model | Key Strength |

| Gumroad | Solopreneurs, first product launch | 10% per sale, no monthly fee | Zero setup friction; live in under 10 minutes |

| Lemon Squeezy | SaaS founders, subscriptions | 5% + payment processing | Merchant of Record; handles VAT globally |

| Payhip | UK/EU creators needing VAT compliance | Free plan + 5%; paid from $29/mo | Auto-handles EU and UK VAT; affiliate tools |

| Kajabi | Serious creator businesses at £5K+/month | $69–$399/mo | Most powerful pipeline tools; integrated CRM |

| Stan Store | TikTok-first creators | $29/mo flat | Integrates natively with TikTok bio link |

| Whop | Community-first, Discord-integrated products | 3% transaction fee | Best for community access and SaaS tools |

| STAGE STRATEGY | Stage 1 (0–£1K revenue): Gumroad or Payhip free plan — test whether anyone will pay, not how to build the perfect storefront. Stage 2 (£1K–£5K/mo): Migrate to Podia or Lemon Squeezy. Stage 3 (£5K+/mo): Invest in Kajabi as the operating system for a full creator business. |

7.2 The Scalable Business Models

The four TikTok-native business architectures generating consistent, documented revenue in 2026 are:

(1) TikTok Shop Brand — source a product aligned to a viral trend, build a creator affiliate army, and repeat with new SKUs (live selling conversion in Southeast Asia is 5x higher than traditional ads).

(2) Short-Form Editing Agency — charge £500–£2,000/month per client for clipping and distributing podcast or YouTube content.

(3) UGC Creator Service — brands pay £150–£500 per UGC video, with no following required.

(4) Trend Forecasting Newsletter — aggregate TikTok trends into a B2B intelligence product.

7.3 The ‘Make Money Online’ Surge — Risk Assessment

The explosion of creators teaching monetisation is a structurally predictable response to three forces: platform income concentrating at the top leaving most creators seeking alternative revenue; AI making course creation trivially cheap; and financial content consistently earning the highest CPMs on YouTube, TikTok, and Instagram. The result is a market where the primary product being sold is the hope of making money, not a transferable methodology for doing so.

Creators and consumers should apply three forensic questions to any monetisation education product: (1) When did the instructor make the money, they are teaching? Strategies that worked in 2018 before competition intensified are not reproducible today; (2) What is the instructor’s primary current income — the product, or the business they teach? A business model where the primary revenue is teaching that business model is a pyramid of hope; (3) Can the instructor produce verifiable, third-party audited proof of income from the underlying activity?

SECTION 8: TRENDS ANALYSIS — SWOT, FORCES & STRUCTURAL THEMES

8.1 SWOT Analysis: The Creator Economy 2026

| Positive | Negative | |

| Internal | STRENGTHS: Democratised access; AI-enabled scale; global audience reach; diversified revenue architectures; compounding content assets on YouTube; growing brand ROI evidence base | WEAKNESSES: Median income of $3K/year; 68%+ earn below $50K; platform algorithm dependency; burnout rates; no labour protections; skills gap in business operations |

| External | OPPORTUNITIES: TikTok Shop EU/UK expansion; B2B creator economy on LinkedIn; gaming × creator convergence; owned community infrastructure; AI-licensed identity deals (Khaby model) | THREATS: Regulatory risk (TikTok US ban unresolved); mandatory AI labelling costs; income concentration accelerating; platform fee extraction; consumer fatigue with AI content; guru market fraud undermining trust |

8.2 Ten Defining Trends for 2026

- Community over audience —brands and creators shifting from mass follower counts to smaller, higher-density verified communities with premium engagement and lower churn

- B2B creator economy emergence — professional expertise on LinkedIn and domain-specific platforms commanding the highest CPMs and sponsorship rates per follower of any content category

- Micro-drama monetisation — serialised short-form fictional storytelling projected to generate $7.8B in 2026, creating a new genre between film and social media

- Live social commerce normalisation — real-time creator broadcasting and retail converging in UK and EU following proven Southeast Asia adoption patterns

- Owned audience infrastructure imperative — email list, community platform, and direct-to-consumer commerce becoming survival infrastructure, not premium differentiation

- AI-labelling as trust premium — human-verified creator badges becoming a commercial differentiator as mandatory AI content disclosure rolls out across all major platforms

- Creator CRM as a distinct software category — purpose-built platforms managing brand relationships, deal pipelines, and audience monetisation in a single view

- Spatial computing integration — Apple Vision Pro and competing devices reaching 40M+ annual shipments, entering creator production and consumer content workflows

- Agentic AI media systems — autonomous content agents growing from $1.76B market in 2025 to $8.17B by 2030, becoming commercially available to mid-tier creators

- Cross-sector IP development — creators serialising content into episodic formats, pitching to Netflix and studios after audience validation, inverting the traditional development funnel

8.3 Porter’s Five Forces — Creator Economy

| Force | Intensity | Key Dynamics |

| Competitive Rivalry | HIGH | 207M+ creators; AI lowering content production costs to near-zero; winner-take-most algorithm dynamics |

| Threat of New Entrants | HIGH | Barrier to entry approaching zero with AI tooling; however, trust and community are durable moats |

| Supplier Power (Platforms) | VERY HIGH | Platforms control distribution, algorithm, and monetisation rules unilaterally; creators have limited recourse |

| Buyer Power (Brands) | MEDIUM | Shifting left toward nano/micro creators; but top creator rates command premium pricing |

| Threat of Substitutes | HIGH | AI-generated content, virtual influencers, and gaming entertainment compete for same attention pool |

SECTION 9: FORWARD OUTLOOK — THREE HORIZONS TO 2035

9.1 Horizon 1: Short-Term (2026–Mid 2027)

Consumer & Creator Behaviour

The dominant behavioural shift of 2026 is the rejection of dopamine-loop content in favour of meaningful, calming, and honest media. Gen Z is actively reducing device time yet paradoxically consuming more short-form content — indicating demand not for less content but for better-quality, less manipulative content. Audiences are gravitating toward smaller, verified communities over algorithmic mass feeds. Consumers are penalising overtly AI-generated content, with enthusiasm declining from 60% to 26% over two years.

Platform & Technology Developments

Substack and LinkedIn are completing their transformation into full social platforms with algorithmic discovery — first-mover creators building there now will have compounding SEO and network advantages. TikTok Shop is expanding natively in EU and UK. Mandatory AI content labelling is rolling out across all major platforms. Agentic AI media tools — valued at $1.76B in 2025 — are growing at 35.91% CAGR toward $8.17B by 2030, with autonomous content agents becoming commercially available to mid-tier creators.

9.2 Horizon 2: Medium-Term (2027–2029)

The creator-entrepreneur model becomes the default operating architecture. Hobbyist creators who do not build a business system around their content will be structurally marginalised by those who do. B2B creators on LinkedIn and domain-specific platforms become the highest-earning category per follower, as professional expertise commands premium CPMs and sponsorship rates that entertainment content cannot match.

The shift from audience to community becomes the organising principle of platform design. Spatial computing enters consumer and creator workflows at meaningful scale. AI-generated creator agents — digital replicas operating autonomously — become standard infrastructure for scaling top creator output. Creator licensing deals at the Khaby Lame scale proliferate as brands and studios formalise identity-as-IP frameworks.

9.3 Horizon 3: Long-Term (2030–2035)

By 2035, the creator of 2026 is unrecognisable. The convergence of AI, spatial computing, agentic systems, and — at the frontier — brain-computer interface technology fundamentally alters content creation, distribution, and consumption. The market, projected at $2 trillion by 2035, will have absorbed entertainment, e-commerce, education, and professional services as integrated creator-economy verticals.

| 2035 SCENARIO | The creator of 2035 operates a personal media-commerce-AI hybrid: licensing their identity to autonomous AI agents; running permanent virtual presences in spatial environments; selling directly to global audiences without platform intermediaries; and commanding economic leverage previously reserved for major corporations. The platform era ends; the creator-infrastructure era begins. |

| Horizon | Timeframe | Defining Technology | Creator Economy Signal |

| Short | 2026–2027 | Agentic AI tools, mandatory AI labelling | AI operational baseline; community over audience |

| Medium | 2027–2029 | Spatial computing, creator licensing at scale | Creator-entrepreneur default; B2B creators dominant |

| Long | 2030–2035 | BCI, autonomous AI agents, full spatial media | $2T market; platform disintermediation; creator-as-IP |

SECTION 10: CONCLUSION & STRATEGIC TAKEAWAYS

The creator economy of 2026 is defined by a central paradox: unprecedented scale and structural inequality operating simultaneously. The market generates hundreds of billions of dollars while the median participant earns $3,000 per year. AI is democratising production while accelerating income concentration. Platforms are offering more tools while extracting more control. The opportunity is real; the path to capturing it is narrower than popular narrative suggests.

The creators, brands, and investors who will prosper through 2030 share a common characteristic: they are building systems, not placing bets. They treat AI as infrastructure, not novelty. They cultivate owned audiences as the non-negotiable foundation beneath any rented platform presence. They understand that the platform era is transitional and are positioning for the infrastructure era that follows.

10.1 Strategic Takeaways by Stakeholder

For Creators & Creator-Entrepreneurs

- Build email list from day one. No exception. A TikTok audience is borrowed infrastructure; email is owned capital.

- Diversify revenue to at least three streams. Brand deals alone create systemic fragility. Owned digital products generate margin; communities generate retention.

- Deploy AI in the correct sequence: eliminate waste first, augment creativity second, scale proven formats third. Tool sprawl without discipline produces noise.

- Invest in platform-adjacent B2B positioning. LinkedIn creators earn the highest income per follower. Professional expertise commands premium CPMs that entertainment content cannot match.

- Protect and develop your authentic voice. As AI content volume increases, human specificity the scar, the opinion, the lived experience becomes increasingly scarce and commercially valuable.

For Brands & Agencies

- Shift from mega-influencer spend toward nano and micro creators. Authenticity premium and engagement depth justify the coordination cost, and the ROI evidence base now supports it.

- Move from campaign-based to relationship-based creator partnerships. Long-term co-creation delivers better brand equity and more defensible attribution than one-off posts.

- Build AI measurement infrastructure now. 94% of brands report creator content outperforms traditional digital advertising, but measurement frameworks remain nascent. First-mover advantage in attribution technology is significant.

- Treat creator identity as a licensable asset class. The Khaby Lame model is the blueprint for the next wave of major creator partnerships at brands with global multilingual distribution needs.

For Platform Operators & Technology Providers

- Creator CRM is an underserved category. The largest unmet need in the creator stack is a single view of brand relationships, deal pipeline, audience monetisation, and performance data.

- AI labelling infrastructure is becoming a compliance requirement. Platforms that provide seamless, creator-friendly disclosure tools will have regulatory and trust advantages.

- Owned audience portability is the next frontier. Creators are increasingly sophisticated about platform dependency; those building tools that help creators own their audience relationships will win the next generation.

10.2 The Governing Principle

| “The creator economy rewards systems-builders, not content-posters.” Creator Economy Intelligence Group, Q1 2026 |

DISCLAIMER: This Intelligence Brief is produced for informational and strategic planning purposes only. It does not constitute financial, legal, or investment advice. All market size figures represent a range of third-party estimates and should be verified independently before use in financial modelling or investment decisions. Creator income data reflects survey-based self-reporting and is subject to selection and response bias. Forward-looking projections involve material uncertainty. The Creator Economy Intelligence Group accepts no liability for decisions made on the basis of this document.

© 2026 CEIAG Creator Economy Intelligence Group. All rights reserved. Reproduction or distribution requires prior written consent.

{kind=link}

{kind=link}

{kind=link}

{kind=link}