Vehicle Product Definition, Feasibility Study & Investment Business Case

.

Strategic concept dossier for an affordable global small / mid-size modular work truck Document Map

- 1. Executive summary and investment thesis

- 2. What this document is called in the automotive industry

- 3. Source brief, design intent and non-negotiables

- 4. Market thesis and demand signals

- 5. Product architecture: one shell, many souls

- 6. Regional product strategy: North America, Europe, Global South

- 7. Stakeholder and customer deep dive

- 8. Configuration strategy, modularity vs configuration

- 9. Technical, safety, durability and compliance requirements

- 10. Software, hardware, materials and data stack

- 11. Manufacturing, CKD, plant strategy and localisation

- 12. Financial model, profitability and break-even

- 13. Commercial models: ownership, rental, lease, fleet and microfinance

- 14. Go-to-market strategy, brand architecture and naming

- 15. Development timeline, test cycle and programme deliverables

- 16. Risk register, strategic scenarios and version-2 roadmap

- 17. Appendices: matrices, checklists, partner brief and open questions

1. Executive Summary and Investment Thesis

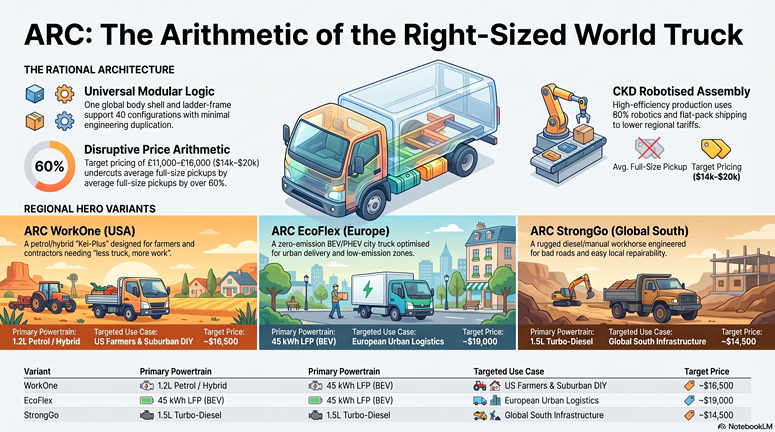

ARC is a proposed affordable, right-sized, globally localised truck platform designed for the gap between Japanese kei-truck utility, Toyota Hilux Champ / IMV 0 modularity, and the increasingly expensive full-size pickup ecosystem. The programme should be treated as a vehicle-programme business case rather than only a styling concept.

The core thesis is that the world does not need one more overpowered status pickup. It needs a configurable work platform that can be bought, leased, financed, repaired, converted, and localised across sharply different infrastructure realities.

The strongest programme definition is not three separate trucks. It is one universal architecture with regional expressions: a North American petrol/hybrid WorkOne, a European BEV/PHEV EcoFlex, and a Global South diesel/manual StrongGo.

Source / basis: Uploaded ARC material defines the platform as a universal stamped body shell with modular ladder-frame architecture and region-specific powertrain packages; it also positions ARC around WorkOne, EcoFlex and StrongGo regional expressions. Refrences including alternatives, lessons and tech stack: World Truck

1.1 Investment decision in one paragraph

Proceed to a formal Gate 1 feasibility programme only if the sponsor accepts a staged business model: a low-cost, non-road or limited-road ARC Basic / CKD utility derivative may target the $6k–$9k band in selected Global South or off-road/agricultural contexts, but a full road-legal North American or European vehicle will likely sit above that band once safety, emissions, warranty, logistics, dealer margin and homologation are included. The realistic high-volume road-legal target is a $10k–$20k ladder of products, with $6k treated as a kit / farm / emerging-market floor rather than a universal retail promise.

1.2 Recommended programme architecture

| Decision area | Recommended answer | Reason |

| Platform | Universal ladder-frame + stamped body shell | Balances repairability, safety, low tooling cost and multi-powertrain flexibility. |

| Vehicle class | Small / compact work truck, not a lifestyle-only EV | Protects global credibility and avoids competing only on image. |

| Launch product | StrongGo or WorkOne first; EcoFlex after BEV cost validation | Diesel/petrol/hybrid variants are more likely to meet affordability targets than BEV first. |

| Price ladder | $6k farm/CKD/limited-use floor; $10k–$14.5k Global South road workhorse; $14k–$19k North America; $18k–$20k Europe BEV/PHEV upper edge | Separates aspirational affordability from road-legal compliance costs. |

| Manufacturing | China/Asia supply chain nucleus + regional CKD final assembly + selective local content | Uses mature supplier base while allowing local jobs, tariffs mitigation and localisation. |

| Software | Safety-critical closed stack; open upfitter APIs and fleet data interfaces | Preserves homologation and liability control while enabling third-party bodies and services. |

| Business model | Sales + fleet lease + seasonal rental + microfinance + body-module financing | Affordability is not only low price; it is access to utility. |

1.3 Decision status

- Approved in this document: none. This is a structured strategic draft.

- Candidate for approval: architecture direction, regional product ladder, programme gates and research plan.

- Not approved: final design, plant location, final naming, production volumes, pricing, partners, financial investment, safety claims, emissions claims or launch markets.

2. Document overview

In automotive language, this pack is a hybrid of several documents because ARC is not yet a locked programme.

| Industry document | What it usually contains | ARC use |

| Vehicle Programme Business Case | Market opportunity, investment requirement, volume forecast, unit economics, break-even, strategic rationale. | Primary document name for investor, OEM or partner discussion. |

| Product Definition Document (PDD) | Vehicle mission, customer targets, regional variants, features, package, price positioning. | Defines WorkOne, EcoFlex, StrongGo and the ARC global platform. |

| Product Requirements Document (PRD) | Must/should/could requirements for safety, comfort, utility, software, service and manufacturing. | Translates the concept into measurable targets. |

| Concept Feasibility Study | Engineering feasibility, supply chain assumptions, manufacturing routes, regulatory constraints. | Assesses universal body shell, ladder frame, CKD and modular powertrains. |

| Gate 0 / Gate 1 Programme Approval Pack | Decision-gate summary for moving from idea to funded feasibility. | Use this dossier to decide whether ARC enters formal feasibility. |

| Investor / OEM Pitch Appendix | Condensed narrative, economics, risks, partner ask and next-step funding. | Included as a partner brief appendix. |

Recommended title: ARC World Truck Programme — Vehicle Product Definition, Feasibility Study & Investment Business Case.

3. Source Brief, Design Intent and Non-Negotiables

The source brief asks for a fused concept using Japanese kei-truck standards, the Toyota Hilux Champ / IMV 0 work-truck strategy, and a compact boxy off-road/SUV emotional reference. It also requests a global strategy covering Europe, North America and Global South markets, powertrain alternatives, configurations, modular manufacturing, profitability and launch planning.

Source / basis: Uploaded prompt and ARC files specify kei-truck + Hilux Champ inspiration, $14k–$20k original price target, basic comfort, single/double cab variants, 2WD/4WD, electric/diesel/hybrid/PHEV options, CKD assembly and the Toyota-meets-Honda / Italdesign / Starck design language.

3.1 Price interpretation

The newer brief asks for a price starting near $6,000 and topping out near $20,000. This should be interpreted as a price architecture rather than one universal retail promise.

| Band | Candidate product | Road-legal status | Reality check |

| $6k–$9k | ARC Basic / Farm Kit / CKD local utility | Off-road, agricultural, campus, closed-site, or limited-market homologation | Possible only with extreme simplification, local assembly, minimal trim, no full US/EU compliance and lower warranty burden. |

| $9k–$12k | Global South petrol/diesel base | Selected road-legal markets after local homologation | Requires high local content, simple ICE, limited electronics, low labour cost and very lean distribution. |

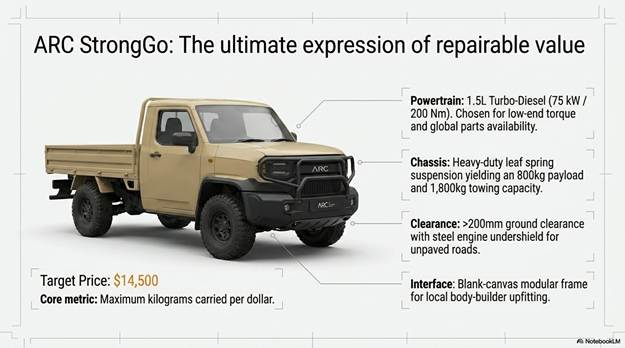

| $12k–$14.5k | StrongGo workhorse | More realistic Global South road product | Diesel/manual/flatbed with repairable hardware and local body building. |

| $14k–$19k | WorkOne North America | Road-legal only if safety and emissions costs are contained | Petrol/hybrid; $16.5k–$19k is more realistic than $14k for the US. |

| $18k–$20k | EcoFlex BEV/PHEV and high trims | EU/urban fleet compliance | Battery cost and ADAS may push above $20k unless subsidised, partner-led or fleet-financed. |

3.2 Non-negotiables

| Category | Baseline requirement | Why it is non-negotiable |

| Safety | Dual airbags, ABS, ESC, side-impact protection, compliant lighting, rear camera where required, engineered crash structure. | Affordability must not mean unsafe or illegal. |

| Comfort | Air conditioning and heating as standard in most markets; USB power; phone mount; durable seats. | A global vehicle must handle heat, cold and daily use without feeling punitive. |

| Utility | Low bed height, tie-downs, flat/dropside/box/service/camper interfaces, 500–800 kg payload band. | The vehicle must be a real work tool, not a style object. |

| Durability | 200 mm target ground clearance, corrosion protection, sealed electrical connectors, skid plate on rugged variants. | Needed for rural roads, flooding, dust, gravel and farm use. |

| Repairability | Replaceable bumpers, lights, front clip, fenders, bed panels; standard fasteners; accessible engine bay. | Global South and work-fleet buyers need local repair without expensive tooling. |

| Configurable not chaotic | Curated packages by region instead of uncontrolled modular complexity. | Customers accept useful configuration; they reject modularity that shifts risk to them. |

4. Market Thesis and Demand Signals

ARC is positioned against a visible market tension: vehicle prices have risen, full-size pickups have become expensive and physically large, and small utility vehicles are gaining cultural and practical attention. Demand does not mean a guaranteed business case; it means there is a plausible white space worth testing.

4.1 North America market signal

The strongest North American signal is not that every buyer wants a tiny truck; it is that affordability, hybrid efficiency and right-sized utility are credible again. Cox Automotive / Kelley Blue Book reported a December 2025 average transaction price of $66,386 for full-size pickups, while Ford reported record 2025 Maverick sales of 155,051 units and strong demand for entry-level trims. These two data points support the ARC thesis: there is a gap between high-price full-size pickups and low-cost utility needs.

4.2 Europe market signal

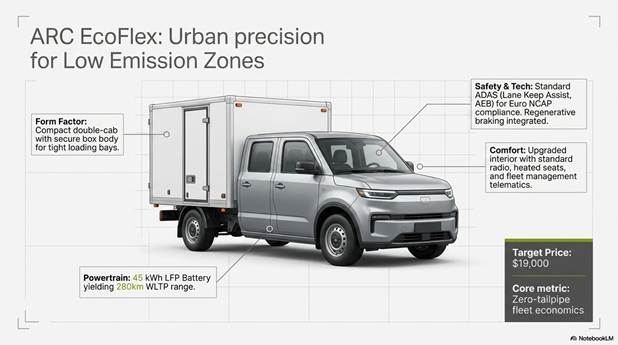

Europe is less about anti-pickup sentiment and more about urban regulation, low-emission zones, fleet efficiency, compact size and total cost of ownership. Euro 7 adds requirements around emissions, energy use, battery durability and non-exhaust pollutants such as brakes and tyres; ARC’s EcoFlex should therefore be BEV/PHEV-first and tuned around city logistics, contractor access and municipal fleets.

4.3 Global South market signal

Global South demand is less about lifestyle and more about economic mobility. A low-cost, repairable, durable vehicle can serve farms, traders, builders, municipalities, NGOs and families. The Hilux Champ / IMV 0 confirms that a stripped-back, modular, affordable work platform can be positioned around customisability and utility in Asian markets.

4.4 Competitive white space

| Competitor / substitute | Strength | Weakness ARC can attack | ARC response |

| Full-size pickup | Payload, image, towing, dealer network | Price, size, fuel use, urban inconvenience | Smaller, cheaper, lower TCO, sufficient payload for many jobs. |

| Ford Maverick / compact pickup | Proof of compact-truck demand; hybrid credibility | Still US-centric and not deeply modular as a world utility platform | More configurable, lower-cost, global work-first positioning. |

| Kei truck import | Low cost, charm, farm utility | Regulatory limits, crash/safety gap, age limits in US | Kei-Plus road-legal adaptation with safety structure. |

| UTV / side-by-side | Off-road work, low weight | Often expensive, less road capable, lower comfort | Road-capable work utility with cab, HVAC, real bed. |

| Small van | Urban cargo efficiency | Less rural/off-road utility, lower emotional appeal | Truck bed and body module ecosystem. |

| Slate-style minimalist EV | Low-cost EV and accessory ecosystem signal | Higher price than ARC target, EV-only limitations | Use Slate-like simplicity and accessory logic without forcing BEV everywhere. |

| Hilux Champ / IMV 0 | Strong work platform, modularity, Toyota credibility | Regionally limited and larger than kei | ARC adapts the idea globally and smaller where needed. |

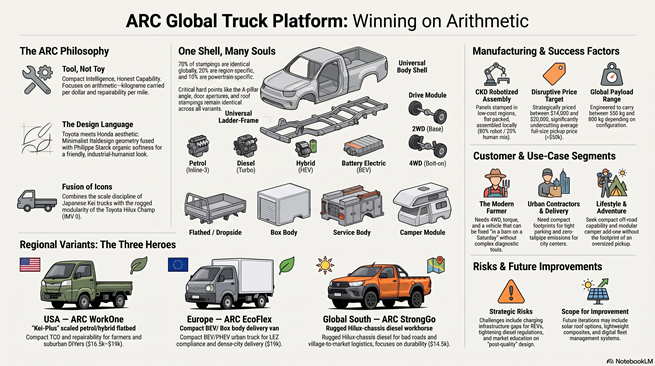

5. Product Architecture: One Shell, Many Souls

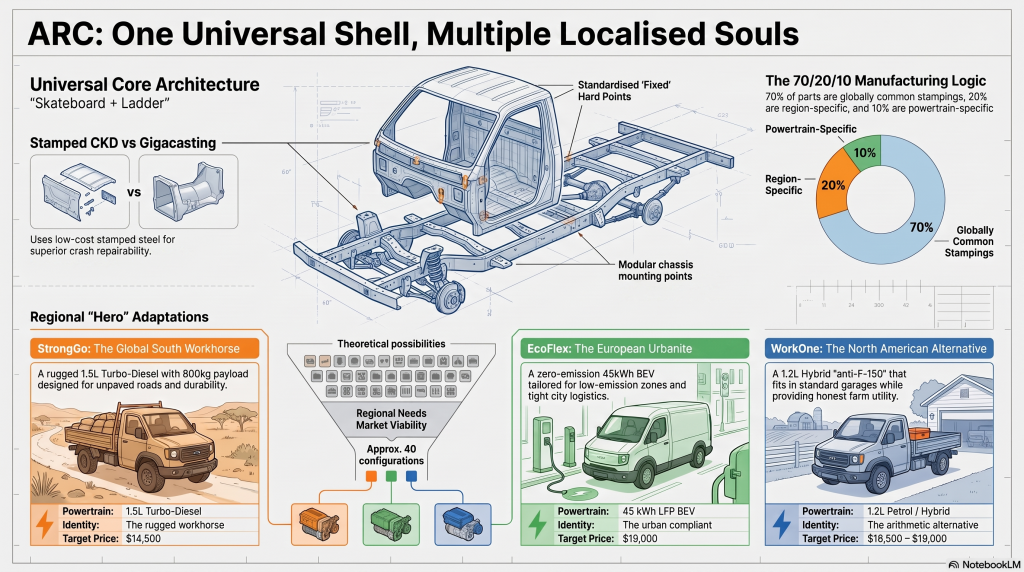

The central engineering answer is a universal architecture that feels modern without becoming unrepairable. ARC should not adopt a Tesla-style gigacasting philosophy for the main work-truck architecture. Gigacasting can reduce parts and labour in high-volume EV programmes, but ARC needs accident repairability, multiple powertrains, regional localisation, rough-road durability and low-capital CKD deployment.

The recommended architecture is a modular ladder-frame platform with a universal stamped body shell, bolt-on powertrain cradles, bolt-on drive modules, and a universal rear mounting grid. The body shell gives design identity and safety hard points; the ladder frame gives repairability and conversion flexibility.

5.1 Architecture stack

| Layer | Component | Global commonality target | Variable elements |

| A | Universal cab shell / body-in-white | 70%+ common | Cab-length insert, LHD/RHD adaptation, ADAS mount pack. |

| B | Universal ladder frame | High commonality | Bolt-on wheelbase/mid-section, rear frame extension, suspension tune. |

| C | Front powertrain cradle | Common interface | Petrol, diesel, hybrid, BEV motor/inverter, cooling pack. |

| D | Floor / tunnel module | Common perimeter | ICE exhaust tunnel, PHEV battery tunnel, BEV underfloor/tunnel pack. |

| E | Drive module | Shared mounting points | 2WD rear drive, 4WD transfer case + front diff / e-axle. |

| F | Rear body module | Universal mounting grid | Flatbed, dropside, box, service, camper, third-party upfits. |

| G | Electrical / data backbone | Common low-cost architecture | Region-specific ADAS, telematics, fleet, charging, emissions. |

5.2 Why stamped panels and ladder frame beat gigacasting for ARC

| Criterion | Gigacasting / single-piece structure | Stamped + modular ladder-frame ARC strategy |

| Repairability | Poor for low-cost accident repair; large casting replacement may total the vehicle. | Replaceable panels, bolt-on front clip, local welding and body repair possible. |

| Powertrain flexibility | Optimised for one architecture, often EV-first. | Petrol, diesel, hybrid, PHEV and BEV can share interfaces. |

| Capital cost | High upfront casting equipment and high-volume dependency. | Lower-risk stamping, welding and CKD deployment. |

| Global South suitability | Weak where skilled casting repair and parts networks are absent. | Better for village garages, local body builders and rough-road adaptation. |

| Crash tuning | Possible but complex; changes can require large structural redesign. | Stamped structures allow controlled crash boxes and replaceable crush members. |

| Third-party bodies | Limited if structure and body are too integrated. | Universal rear mounting grid supports local upfitters. |

6. Regional Product Strategy

ARC should be a single global platform with regional tuning rather than a single fixed global spec. The same body and frame language should produce different powertrain and body packages depending on infrastructure, regulation and buyer expectations.

| Region | Hero name | Powertrain | Size | Price band | Use cases | Critical risk |

| North America | ARC WorkOne / Weekender | Petrol + hybrid; PHEV later | Kei-Plus / Compact | $14k–$19.5k | Farm, ranch, contractor, landscaping, suburban DIY, weekend adventure | Must overcome small-truck perception; needs safety, 4WD option, service network. |

| Europe | ARC EcoFlex | BEV + PHEV | Compact | $18k–$20k+ or fleet financed | Urban contractors, delivery, municipal fleets, low-emission-zone users | Battery/ADAS cost is the largest pricing risk. |

| Global South | ARC StrongGo | Diesel + petrol; hybrid later in urban hubs | Hilux-Chassis / Compact | $6k–$14.5k depending homologation | Farms, market traders, construction, village logistics, NGOs, governments | $6k only plausible as kit/off-road/basic local derivative; road product more likely higher. |

| Asia/China launch nucleus | ARC platform / local name TBD | Petrol, diesel, low-cost EV, hybrid | Compact / Hilux-Chassis | $8k–$16k | Supply-chain and manufacturing ground zero; export base | IP, tariffs, geopolitical risk and brand trust must be managed. |

| Latin America | StrongGo / WorkOne localised | Petrol, ethanol-compatible petrol where relevant, diesel | Compact / Hilux-Chassis | $9k–$16k | Agriculture, construction, SMEs, municipal fleets | Fuel variability, import tariffs and dealer/service setup dominate. |

| Africa | StrongGo Africa | Diesel + petrol; EV only in fleet/campus pilots | Hilux-Chassis | $8k–$14.5k | Agriculture, mining support, health outreach, NGO, logistics | Durability, parts supply and finance access more important than tech features. |

6.1 Hero variants

| Variant | Market | Core configuration | Target price | Strategic role |

| ARC Basic / Local Utility | Global South / closed-site | Single cab, flatbed/dropside, 2WD, petrol or diesel, minimal electronics | $6k–$9k | Price halo; farm/campus/municipal/site utility; not universal road-legal promise. |

| ARC StrongGo | Global South | Single cab, flatbed, diesel, 4WD, manual, 800 kg payload target | $12k–$14.5k | Ruggedness, repairability, high payload, low bed, local body builders. |

| ARC WorkOne | North America | Single/extended cab, dropside/flatbed, petrol/hybrid, 2WD/4WD, 550–650 kg payload | $14k–$19k | Anti-bloat utility for farmers, contractors, landscapers and DIY owners. |

| ARC Weekender | North America consumer | Double/extended cab, hybrid/PHEV, camper/adventure body, 4WD | $18k–$20k+ | Consumer desirability without overpowered full-size truck logic. |

| ARC EcoFlex | Europe | Double cab, box/service body, BEV/PHEV, ADAS, telematics | $18k–$20k+ / fleet lease | Low-emission urban work; TCO and regulatory access. |

6.2 Visual reference and concept imagery

The visuals are reference-level only. They support proportion, stance, modular body logic and customer-facing design language. They are not final styling approvals.

Reference image: Hilux Champ-style modular work-truck logic, upright face and dropside utility.

Concept render: ARC WorkOne X / North America utility expression. Image is illustrative and not an engineering release.

7. Stakeholder and Customer Deep Dive

The ARC stakeholder model must avoid assuming that one buyer represents an entire region. Every market contains commercial, non-commercial, fleet, government, rural, urban and lifestyle buyers. The product should therefore be configured around use cases, not merely geography.

| Stakeholder | Regions | Needs | ARC requirement | Demand signal |

| Rural farmer / rancher | US, LATAM, Africa, Asia | Low cost, repairability, 4WD, payload, low bed height | Diesel/petrol/hybrid depending fuel; dropside/flatbed; basic HVAC; rugged tyres | High if price and repairability are real. |

| Urban contractor | US/EU/China/India cities | Parking, tool security, double cab, low TCO, image acceptable to clients | Hybrid or BEV/PHEV; box/service body; phone-based interface; rear camera | High in fleets, moderate in private sales. |

| Small business delivery | EU, China, US cities, Global South urban hubs | Cargo security, low energy cost, branding surface, uptime | Box body, telematics, lease/maintenance package | High if fleet finance works. |

| Municipal / campus fleet | Global | Low acquisition cost, easy repair, predictable maintenance | 2WD/BEV for campuses; diesel/petrol for rough areas; simple bodies | High with tender-friendly standardisation. |

| NGO / health / field service | Africa, Asia, LATAM | Rugged access, parts supply, easy training, optional clinic body | StrongGo service/ambulance modules; diesel; dust/water sealing | High if parts/finance are bundled. |

| Consumer DIY / suburban owner | US, Europe, Australia-style markets | Cool small truck, garage fit, weekend utility, fuel savings | Weekender; hybrid; camper/rack accessories; improved interior | Moderate to high if design is desirable. |

| Lifestyle / camper / overlanding | US/EU/wealthier urban buyers | Adventure credibility, 4WD, modular camper, low running cost | PHEV/hybrid; camper body; roof rack; higher trim | High margin but should not lead the work-truck brand. |

| Upfitter / body builder | All regions | Stable mounting points, wiring interfaces, CAD data, warranty clarity | Open upfitter guide; mounting grid; body controller API | Crucial ecosystem multiplier. |

| Dealer / service partner | All regions | Simple training, parts margin, predictable warranty, diagnostic tools | Parts bin, service manuals, diagnostic app, regional inventory | Critical for trust. |

7.1 Complaints ARC should solve

- Full-size pickups are too expensive, too large and too fuel-hungry for many daily tasks.

- Kei trucks are useful but often face legal, safety and parts constraints outside Japan.

- UTVs can be costly and are not always road-comfortable or weather-protected.

- Urban contractors need a secure, compact, professional vehicle that does not look like a van by default.

- Global South users need a truck that can survive poor roads, inconsistent fuel quality and informal repair networks.

- Customers accept configuration when it feels like a solution; they reject modularity when it feels like an unfinished product.

8. Configuration Strategy, Modularity vs Configuration

The programme should not advertise itself as modular for modularity’s sake. Many modular products fail because customers are asked to manage complexity, reliability, warranty and compatibility. ARC should instead communicate configuration: curated, warranted, localised product packages selected for real use cases.

8.1 Why people accept configuration but often reject modularity

| Dimension | Unpopular modularity | Accepted configuration |

| Customer burden | User must know which modules fit and what fails. | Factory or dealer presents clear packages. |

| Reliability | Interfaces can loosen, fail or be misused. | Interfaces are engineered, tested and warrantied. |

| Value perception | Feels like a kit or compromise. | Feels like a choice: work, family, fleet, adventure. |

| Service | Dealer may blame modules or third parties. | Service plan defines responsibility. |

| Financing | Banks may not value modules properly. | Configured vehicle has clear residual value. |

| Brand language | Modular sounds technical. | Configured sounds personal and useful. |

8.2 Configuration principles

- Sell 6–8 curated launch configurations per region, not 360 theoretical combinations.

- Keep engineering interfaces universal but customer choices simple.

- Let third-party upfitters operate behind a certified interface guide.

- Use fleet and commercial sales to validate the most important configurations before expanding consumer variants.

- Preserve one visual identity across regions, with front fascia, ride height, body module and colour localised.

8.3 Configuration matrix

| Configuration axis | Low-cost / base | Core commercial | Premium / specialised |

| Size class | Kei-Plus | Compact | Hilux-Chassis |

| Powertrain | Petrol | Diesel | Hybrid / PHEV / BEV |

| Drive | 2WD | 4WD mechanical | Electric AWD / future e-axle |

| Cab | Single | Extended | Double |

| Body | Flatbed | Dropside / box / service | Camper / specialty upfit |

| Trim | Basic | Comfort | Fleet / Adventure |

| Price target | $6k–$12k | $12k–$16.5k | $16.5k–$20k+ |

9. Technical, Safety, Durability and Compliance Requirements

ARC cannot be built around nostalgia or visual references alone. It needs a measurable requirement set. This section defines the requirements that should be converted into engineering specifications in the next programme gate.

| ID | Area | Priority | Requirement | Reason |

| REQ-SAF-01 | Safety | Must | Comply with target-market homologation requirements before road sale; define FMVSS, Euro NCAP, Global NCAP strategies separately. | Legal entry and brand trust. |

| REQ-SAF-02 | Safety | Must | Dual front airbags, ABS, ESC, seat-belt reminders, compliant lighting, side-impact structure. | Minimum global safety expectation. |

| REQ-DUR-01 | Durability | Must | 200 mm target ground clearance on rugged variants; sealed connectors; dust/water resistance strategy. | Rural and Global South durability. |

| REQ-REP-01 | Repairability | Must | Replaceable front clip, bumper, fenders, lamps, bed panels; standard fasteners. | Low downtime and lower insurance write-offs. |

| REQ-USE-01 | Usability | Must | Low bed height, visible tie-downs, flat load floor and simple cabin ingress/egress. | Work credibility. |

| REQ-COM-01 | Comfort | Must | Air conditioning / heating, USB, phone mount, durable seating. | Global climate usability. |

| REQ-POW-01 | Powertrain | Must | Shared mounting strategy for petrol, diesel, hybrid/PHEV and BEV modules where feasible. | Localisation flexibility. |

| REQ-SW-01 | Software | Must | Safety-critical software closed/certified; fleet and upfitter interfaces documented. | Liability and ecosystem balance. |

| REQ-MFG-01 | Manufacturing | Must | CKD-ready body, frame and powertrain module packaging. | Tariff, supply and local assembly strategy. |

| REQ-COST-01 | Cost | Must | Every feature must be classified as base, regional, optional or deleted to protect price targets. | Affordability discipline. |

9.1 Homologation strategy

The programme must not assume a single global certification. North America, Europe, China, India, Latin America and Africa have overlapping but distinct safety, emissions, lighting and data requirements. The next step is a regulatory matrix by launch country.

| Region | Primary compliance emphasis | ARC strategy |

| North America | FMVSS, EPA/CARB emissions, crashworthiness, lighting, OBD, warranty and recalls. | Kei-Plus must grow enough for crash structure; petrol/hybrid first; BEV only if cost and charging support justify it. |

| Europe | Type approval, Euro 7, Euro NCAP expectations, ADAS, pedestrian safety, battery durability, charging standards. | EcoFlex BEV/PHEV, compact footprint, box/service body, ADAS standard. |

| China | Local type approval, NEV opportunities, supply chain and battery rules, data governance. | Possible manufacturing nucleus and NEV pilot; partner essential. |

| India / ASEAN | Local emissions, safety escalation, cost sensitivity, high utilisation. | StrongGo/Compact with local content and fleet/government pilots. |

| Africa / LATAM | Country-specific rules, fuel quality, road durability, parts networks. | Diesel/petrol rugged trims; local service and finance bundled. |

10. Software, Hardware, Materials and Data Stack

10.1 Software stack

| Layer | Recommended approach | Open/proprietary position |

| Vehicle control | Certified ECU/VCU, BMS, ABS/ESC, airbags, powertrain controllers. | Closed and safety-certified; no open modification. |

| Body control | Lighting, HVAC, locks, wipers, upfitter power, rear body interface. | Controlled API for approved upfitters. |

| Infotainment | Phone-first interface, mount, USB, optional fleet tablet. | Keep minimal; avoid costly built-in screens on base. |

| Fleet telematics | GPS, diagnostics, maintenance, battery/fuel use, job-cost data. | Opt-in; regional privacy compliance. |

| Service diagnostics | Low-cost diagnostic app, OBD support, service manuals. | Open enough for authorised repair networks and right-to-repair expectations. |

| Digital passport | Optional ownership, battery, maintenance, accident and parts traceability ledger. | Blockchain only where it solves finance/residual/anti-fraud problems; not core control system. |

| OTA updates | Limited OTA for non-safety features; safety updates governed. | Conservative; avoid bricking vehicles in low-connectivity markets. |

10.2 Hardware stack

- Universal E/E backbone with regional harness add-ons.

- Base sensor pack: rear camera, wheel-speed sensors, basic telematics option, OBD diagnostics.

- EU/upper trims: AEB, lane warning, adaptive cruise where required or commercially justified.

- BEV/PHEV: LFP battery preference for durability, safety and cost stability; IP-rated battery sealing; battery health monitoring.

- ICE: simple petrol/diesel engines prioritising torque, serviceability and parts availability rather than maximum power.

- 4WD: mechanical transfer-case solution for rugged ICE; possible electric rear/front e-axle in version 2.

10.3 Materials stack

| Subsystem | Material / approach | Rationale |

| Ladder frame | High-strength steel | Repairable, globally familiar, suitable for rough roads and body upfits. |

| Body panels | Stamped steel; selective galvanized/corrosion treatment | Low-cost tooling, repairable, paint/wrap-friendly. |

| Bumpers/cladding | Black textured polypropylene or equivalent | Replaceable, durable, hides scratches. |

| Interior | Rubber flooring, vinyl/durable cloth, hard-wearing plastics | Washable, low-cost, suitable for commercial users. |

| Battery | LFP chemistry for BEV/PHEV where available | Safer thermal profile and potentially lower cost than nickel-rich chemistries. |

| Glass | Large simple glazing with shared apertures | Visibility, common tooling, lower cost. |

| Fasteners | Standardised global fasteners | Local repairability and upfitter compatibility. |

11. Manufacturing, CKD, Plant Strategy and Localisation

The manufacturing strategy is the core of ARC’s affordability. The programme cannot meet its price promise by design language alone. It must use supply-chain discipline, common parts, regional assembly and a controlled configuration range.

11.1 Manufacturing options

| Route | Advantages | Risks | Recommendation |

| Option A: China / Asia nucleus + global CKD | Highest supply-chain depth, battery/EV component access, low parts cost, speed | Geopolitical/tariff risk, brand trust, export restrictions, IP management | Best early proof-of-cost option if partner governance is strong. |

| Option B: Mexico assembly + US finishing | USMCA logic, North American proximity, labour advantage, political acceptability | Supply chain still imported; tariff/policy uncertainty | Strong for WorkOne North America. |

| Option C: EU light assembly / final fit | Better for EcoFlex fleet tenders, compliance and service trust | High labour cost; BEV battery sourcing complex | Use for final calibration, body fit, fleet upfit. |

| Option D: India / ASEAN production hub | Strong frugal engineering, Global South export logic, ICE and small commercial expertise | May need multiple homologation paths | Strong for StrongGo and Asia/Africa exports. |

| Option E: Full US manufacturing | Political appeal, local jobs, brand trust | Cost risk may break $20k ceiling | Only for higher trims or when incentives/volume justify it. |

| Option F: Contract manufacturing | Lower initial plant risk, faster launch | Lower control, margin sharing, capacity dependency | Useful for prototype and first series. |

11.2 Robotics/manual labour strategy

The previous 80% robot / 20% human target is suitable for highly structured body/frame work but should not be rigidly applied everywhere. Different markets need different automation ratios.

| Plant type | Robot/manual mix | Best location | Use |

| Central stamping / frame plant | High robotics, high automation | China, Thailand, India, Mexico, Turkey | Stamping, welding, quality-controlled body/frame kits. |

| Regional CKD assembly | 50–80% robot depending volume | Mexico, EU, India, South Africa, Brazil | Final body assembly, powertrain installation, local trim. |

| Low-volume local assembly | 20–50% robot, higher manual | Selected Global South markets | Simple kits, high labour availability, basic inspection rigs. |

| Upfitter ecosystem | Mostly manual / jig-based | Local body builders | Flatbed, service body, ambulance, fire, farm equipment. |

11.3 Localisation modules

| Module | Localisation criteria |

| Regulatory module | Lighting, mirrors, emissions, crash equipment, ADAS, labels, data rules. |

| Powertrain module | Fuel type, emissions kit, battery size, charger standard, gear ratios, cooling. |

| Infrastructure module | Charging access, fuel quality, road conditions, dust/water sealing, tyres. |

| Service module | Dealer density, mobile service, spare-parts depots, technician training. |

| Finance module | Loan/lease/rental, microfinance, fleet residual, seasonal use, government procurement. |

| Cultural module | Name translation, colour preferences, status expectations, trust signals. |

12. Financial Model, Profitability and Break-Even

The financials below are concept-stage ranges, not audited projections. They exist to test whether the programme logic is plausible and to identify which assumptions require validation. All values are illustrative USD unless noted.

12.1 Unit economics by product band

| Product | Target price | Illustrative variable cost | Contribution estimate | Comment |

| ARC Basic / farm kit | $6k–$9k | $4.8k–$7.2k | $0.8k–$1.4k | Off-road/limited-use; local labour; minimal warranty; high risk if positioned as road vehicle. |

| StrongGo base | $10k–$14.5k | $7.4k–$11.0k | $1.8k–$3.0k | Most plausible affordability leader if produced in low-cost hub. |

| WorkOne base | $14k–$16.5k | $10.2k–$12.5k | $2.4k–$3.5k | US compliance, logistics and dealer margin are the main risks. |

| WorkOne hybrid / Weekender | $17k–$20k | $13.0k–$16.0k | $2.8k–$4.5k | Higher margin; consumer/accessory opportunity. |

| EcoFlex BEV/PHEV | $18k–$22k+ | $15.0k–$19.5k | $1.5k–$3.2k | Battery cost, ADAS and EU labour may push above $20k unless fleet-financed. |

12.2 Fixed investment scenarios

| Scenario | Illustrative fixed investment | Average contribution/unit | Break-even volume | Interpretation |

| Partner-led lean | $650m | $1,900 | ~342k units | Uses existing supply chain, contract manufacturing, limited tooling and staged regional launch. |

| Balanced global programme | $1.25bn | $2,600 | ~481k units | Purpose-built platform with one major hub, regional CKD and meaningful validation. |

| OEM clean-sheet | $2.4bn | $3,400 | ~706k units | Full OEM process, multiple regions, higher tooling/testing/plant commitments. |

Break-even formula used: fixed investment divided by average unit contribution. The result excludes financing costs, working capital, taxes, warranty reserve movements and macroeconomic shocks.

12.3 Five-year volume scenario

| Year | Indicative volume | Programme state | Financial implication |

| Year 0 | 0 | Concept, partner search, package mules | No production revenue; prototype and engineering spend. |

| Year 1 | 5k–15k | Pilot CKD / closed fleet / controlled markets | Validate quality, pricing and service. |

| Year 2 | 35k–70k | StrongGo + WorkOne launch markets | Start contribution; high warranty learning. |

| Year 3 | 90k–160k | North America / Global South expansion; EcoFlex pilots | Accessory/upfitter revenue begins to matter. |

| Year 4 | 160k–260k | Full regional catalogue | Potential operating profit if contribution and warranty are controlled. |

| Year 5 | 250k–400k | Mature platform + fleet finance + body ecosystem | Break-even possible in lean or balanced scenario. |

12.4 Profit pools beyond vehicle margin

- Body modules and certified upfit kits.

- Fleet maintenance contracts.

- Seasonal rental and lease programmes.

- Battery lease or energy subscription for BEV/PHEV versions.

- Certified used / remanufactured vehicles.

- Parts ecosystem and low-cost service packs.

- Telematics for fleets where privacy and data rules permit.

- Government, NGO and municipal procurement bundles.

- Wraps, accessory catalogues and dealer-installed personalisation.

13. Commercial Models: Accessibility and Affordability

Affordability is not only the purchase price. For many buyers, accessibility means the ability to rent, lease, share, finance, insure, repair and use the vehicle profitably.

| Model | Target user | Benefit | Risk |

| Cash purchase | Farmers, small businesses, individuals | Simple and trust-building | High upfront cost even if vehicle is cheap |

| Microfinance / asset finance | Global South entrepreneurs | Turns vehicle into income tool | Needs repossession, resale and maintenance controls |

| Seasonal lease | Farms, landscaping, tourism | Matches cash flow to harvest/work season | Residual and utilisation risk |

| Fleet lease | Municipal, delivery, contractor fleets | Predictable TCO, maintenance bundle | Requires fleet service network |

| Battery lease | BEV/PHEV markets | Reduces purchase price and battery fear | Complex accounting and residual risk |

| Body-module finance | Upfitters, SMEs | Lets user start base vehicle and add utility later | Needs warranty and compatibility rules |

| Pay-per-use / rental | Occasional commercial users | Expands access without ownership | Utilisation and damage management |

| Cooperative ownership | Villages, farms, NGOs | Spreads cost across users | Governance, scheduling and maintenance responsibility |

| Digital passport / ledger-enabled finance | Finance companies, fleets, used buyers | Traceability of ownership, service, battery, parts, collateral | Only useful if simple and trusted; avoid speculative token framing |

14. Go-to-Market Strategy, Brand Architecture and Naming

ARC can be the platform name, but local market names may be safer for language, culture and positioning. The global brand should communicate reliable, affordable utility; local names can emphasise work, clean urban use or rugged strength.

| Layer | Name | Meaning | Risk / note |

| Global platform | ARC | Affordable Rational Compact | Check trademark clearance; avoid over-explaining acronym in consumer ads. |

| North America commercial | WorkOne | One small truck that works | Clear, practical, low-risk. |

| North America consumer | Weekender | Small utility for life outside work | May be too lifestyle unless tied to WorkOne. |

| Europe | EcoFlex | Clean urban flexibility | Works for BEV/PHEV fleets; check naming conflicts. |

| Global South | StrongGo | Durable, simple, income-building workhorse | Slightly literal but understandable. |

| China / Asia | Local name TBD | Supply-chain and local trust | Requires native naming and legal review. |

14.1 Launch sequence

- Gate 0: validate the global problem and customer segments.

- Gate 1: select one lead market and one lead commercial variant.

- Pilot A: StrongGo / Global South or WorkOne / North America closed fleet.

- Pilot B: EcoFlex BEV/PHEV with city fleet / municipal users.

- Launch 1: commercial workhorse trims only.

- Launch 2: consumer Weekender / camper / adventure trims after work credibility.

- Launch 3: third-party specialised bodies and local upfitter ecosystem.

15. Development Timeline, Test Cycle and Deliverables

| Timing | Phase | Deliverables | Gate decision |

| 0–3 months | Gate 0 concept definition | Product mission, target markets, concept pack, preliminary regulatory scan, investment thesis | Sponsor approves/revises concept direction |

| 3–6 months | Gate 1 feasibility | Package study, competitor teardown plan, supplier RFIs, preliminary BOM, manufacturing route shortlist | Approve feasibility budget |

| 6–12 months | Architecture mules | Rolling chassis, cab package bucks, powertrain cradle tests, upfitter interface mockups | Select architecture and first powertrain |

| 12–18 months | Alpha prototypes | Initial crash CAE, durability rigs, ergonomics, first customer clinics, styling refinement | Freeze engineering direction |

| 18–30 months | Beta / DV prototypes | Durability, emissions, safety, ride/handling, climate, water/dust, battery tests | Approve design validation |

| 30–36 months | PV / pilot production | Tooling tryout, CKD packaging, plant training, service manuals, parts logistics | Approve production validation |

| 36–42 months | Homologation and launch readiness | Regulatory submissions, fleet pilots, dealer/service training, launch stock | SOP decision |

| 42+ months | SOP + post-launch learning | Warranty tracking, customer data, upfitter expansion, v1.1 updates | Refresh roadmap and V2 decisions |

15.1 Test cycle

| Test family | Examples | Why it matters |

| Safety | Crash CAE, sled, full crash, pedestrian impact, restraint tuning | Do not claim compliance until independently validated. |

| Durability | Rough-road, pothole, corrosion, dust, mud, thermal cycling, load-bed fatigue | Global South and work-fleet credibility. |

| Powertrain | Fuel quality tolerance, cooling, towing, steep grade, battery durability, charging | Different tests by region. |

| Usability | Loading height, visibility, ingress/egress, cabin controls, noise/vibration | Validate with farmers, contractors and delivery drivers. |

| Manufacturing | CKD packing, assembly takt time, robot/manual quality, serviceability | Protect target cost and quality. |

| Software | Diagnostics, telematics, OTA discipline, fleet integration, cybersecurity | No overcomplexity in low-cost versions. |

| Upfitter | Mounting grid, power takeoff/aux power, ambulance/service/fire/farm modules | Ensure third-party ecosystem does not break warranty. |

16. Risk Register, Strategic Scenarios and Version-2 Roadmap

| Risk | Impact | Likelihood | Mitigation |

| $6k pricing promise | High | High | Define $6k as kit/limited-use/selected-market floor, not US/EU road-legal promise. |

| BEV cost overrun | High | Medium | Use fleet lease, smaller battery, PHEV bridge, incentives and battery sourcing validation. |

| Regulatory non-compliance | High | Medium | Early homologation partner and region-by-region compliance matrix. |

| Modularity complexity | Medium | High | Curated configurations, certified upfitter system, limited launch variants. |

| Geopolitical supply chain | High | Medium | Dual sourcing, regional assembly, tariff-aware sourcing, local content strategy. |

| North America changes product identity | Medium | Medium | Protect ARC platform DNA; let USA have Weekender trim without overpowering core architecture. |

| Warranty and quality | High | Medium | Pilot fleets, telemetry, conservative launch volumes, simple components. |

| Brand trust | Medium | Medium | Partner with trusted OEM/contract manufacturer; transparent safety and service plan. |

| Diesel environmental criticism | Medium | High | Position diesel only where infrastructure requires it; roadmap to hybrid/low-carbon fuels/electrification. |

| Third-party upfit liability | Medium | Medium | Certified interface, approved suppliers, clear warranty boundary. |

16.1 Scenario planning

| Scenario | Signal | Strategic response |

| North America embraces ARC | US demand moves from workhorse to lifestyle; pressure for bigger engines and higher trims | Keep WorkOne base protected; create Weekender / Sport trim without changing platform fundamentals. |

| North America drops out | Policy, tariffs or consumer rejection make US launch unattractive | Continue as Global South + Europe + Asia platform; defer US to later partner. |

| Europe BEV costs fail | EcoFlex cannot meet price ceiling | Launch PHEV or fleet-only BEV; use lease rather than retail price headline. |

| Global South repair ecosystem wins | StrongGo becomes the volume backbone | Expand local body builders, service training and microfinance. |

| China becomes ground zero | Supply chain and plant capability make China the initial platform nucleus | Protect IP, manage tariffs, create regional assembly layers and local brand trust. |

16.2 Version 2 roadmap

- Electrified StrongGo urban variant as charging infrastructure improves.

- Swappable body-module certification programme with more service, health, fire and farm modules.

- Battery passport and remanufacturing pathway.

- Electric auxiliary power / power-take-off for tools, refrigeration, pumps or field clinics.

- Improved ADAS and fleet data stack for Europe and North America.

- Local facelifts every 2–3 years; core architecture refresh every 6–7 years; platform life target 12–15 years.

- Remanufactured / certified-used programme to preserve residual value and affordability.

Appendix A — Partner / OEM Pitch Brief

ARC is a low-cost global utility vehicle programme seeking a manufacturing, engineering, supply-chain or OEM partner. The target is a right-sized truck platform built around one universal stamped body shell, one modular ladder-frame architecture, curated regional powertrains and a global upfitter ecosystem.

What ARC wants

- A partner willing to explore a low-cost global work-truck architecture.

- Access to existing small-engine, hybrid, diesel or BEV powertrain modules.

- Manufacturing discipline for stamped panels, ladder frames, CKD packaging and regional final assembly.

- Regulatory expertise in at least one lead region.

- Supplier capability for low-cost HVAC, seating, electrical backbone, lighting, brakes, steering, tyres and batteries.

- A willingness to protect repairability rather than chase high-complexity design theatre.

If the proposed ARC solution is rejected

The underlying customer need remains valuable: a small, affordable, repairable, safe, globally localisable work vehicle with real payload and low total cost of ownership. If one-body-shell global modularity proves too complex, the fallback brief is to develop two architectures: a Global South / North America ICE-hybrid ladder-frame utility and a Europe/urban BEV compact contractor vehicle sharing design language, interior, rear module interfaces and software rather than full body/frame commonality.

Appendix B — Acceptability Checklist

| Area | Checklist |

| Political | Local jobs story, tariff exposure, government procurement eligibility, emissions policy fit. |

| Policy / regulatory | FMVSS, Euro 7, Global NCAP, local emissions, data privacy, battery transport, recycling. |

| Mechanical | Payload, towing, ground clearance, cooling, braking, suspension, service access. |

| Software | Cybersecurity, diagnostics, fleet data, OTA governance, right-to-repair interface. |

| Manufacturing | Tooling cost, CKD logistics, takt time, quality control, local content. |

| Sustainability | Fuel/energy use, repair life, recyclability, battery durability, remanufacturing. |

| Commercial | Unit margin, break-even, financing, residual value, warranty reserve. |

| Cultural | Local name, status perception, colour, body style, trust in brand or partner. |

| Design | Toyota-Honda friendly reliability, not brutally American, credible in city and farm. |

| Upfitter | Mounting points, power, warranty, CAD data, certification process. |

Appendix C — Programme Open Questions

- Which lead market is approved for first feasibility: Global South, North America or Europe?

- Is $6k a symbolic access price, a kit price, an off-road/farm vehicle price, or a road-legal retail price in selected markets?

- Which powertrain is the first proof-of-cost: petrol, diesel, hybrid, PHEV or BEV?

- Does the platform need one body shell globally, or two bodies sharing architecture and design language?

- Which partner archetype is preferred: major OEM, Chinese supply-chain partner, contract manufacturer, regional JV, or startup-led outsourced programme?

- What is the minimum acceptable payload and towing by market?

- Which safety standards are non-negotiable for first launch?

- What level of open upfitter API is allowed without creating liability?

- Should ARC prioritise commercial fleet credibility before consumer lifestyle trims?

- What evidence would stop the programme before major investment?

Appendix D — Source Basis and External References

Uploaded source basis used in this dossier:

- ARC Truck questions.docx — analyst questions and validation framework.

- ARC.docx — PESTLE, SWOT, Porter, market analysis, launch strategy and approval-gate logic.

- ARC is an affordable.docx — ARC world-truck concept and platform narrative.

- alternate spec.docx / recap and spec.docx / spec3.docx / Based on the provided design brief.docx — regional specifications, stakeholder analysis and technical logic.

- prompt.docx and original kei/Hilux design exercise — initial design brief, visual inspiration and requested deliverables.

- Other inspiration.docx — Slate, TELO and other product reference signals.

External references used for current context:

- Toyota Global Newsroom — Toyota launches IMV 0 in Thailand / Hilux Champ customisability.

- Toyota Thailand / Toyota Asia — Hilux Champ launch and 459,000 baht pricing references.

- NHTSA — vehicle importation and 25-year rule / FMVSS context.

- EUR-Lex / EU Euro 7 summary — emissions, brake/tyre, battery durability requirements.

- Cox Automotive / Kelley Blue Book — December 2025 full-size pickup average transaction price.

- Ford — 2025 Maverick sales and affordability demand signal.

- Slate official / public specs references — minimalist EV truck and accessory ecosystem reference.

Appendix E — Final Decision Request

The next meaningful human approval is not a production approval. It is a Gate 1 feasibility approval.

| Approve / revise | Decision needed |

| Architecture | Approve modular ladder-frame + universal stamped shell as the default direction, or request two-platform fallback. |

| Lead market | Choose Global South, North America, or Europe as first feasibility market. |

| Lead variant | Choose ARC Basic, StrongGo, WorkOne, EcoFlex or Weekender as first proof vehicle. |

| Price ladder | Confirm whether $6k is a kit/limited-use floor or a road-legal retail promise in selected markets. |

| Partner strategy | Choose preferred build path: OEM partner, Chinese supply-chain nucleus, contract manufacturer, or regional JV. |

| Evidence threshold | Define what market/customer/engineering evidence is required before funded development. |

Appendix F — Illustrative Visual Appendix

Reference: Japanese kei-truck side proportion, compact footprint and low bed.

Reference Toyota Hilux Champ

{kind=link}

{kind=link}

{kind=link}

{kind=link}