Preamble: Why the technologies quietly solving today’s problems matter more than the ones promising to solve tomorrows and a framework for telling them apart

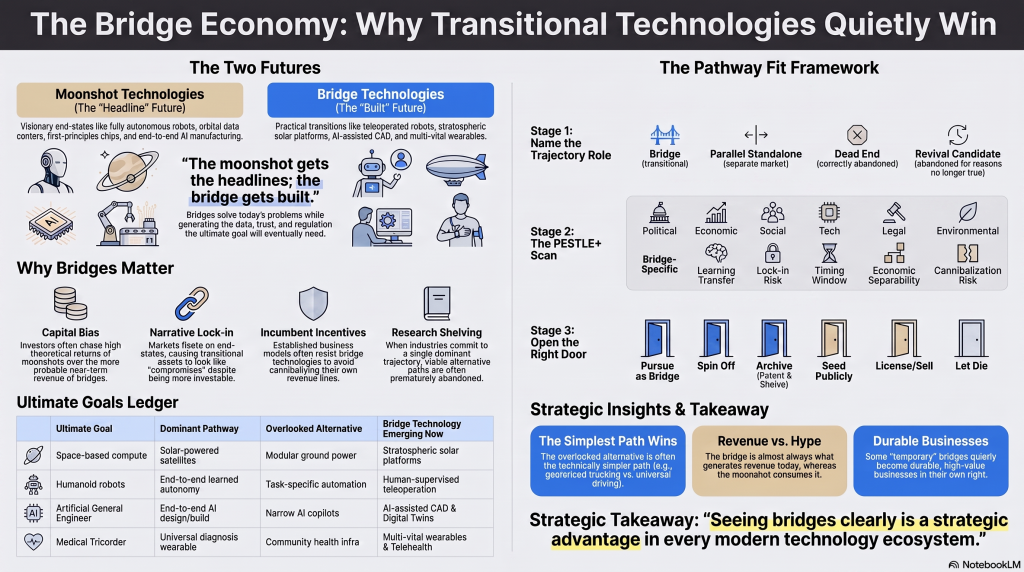

I spend most of my working life inside organisations, architecture reviews, and investment memos, watching the same scene repeat itself. A room full of smart people gets shown two futures. One is a moonshot: fully autonomous robots, orbital data centres, a chip built from first principles, a diagnostic device that reads any illness from a wrist. The other is something smaller, less quotable, and slightly embarrassing to put in a pitch deck a teleoperated robot, a stratospheric solar platform, a slightly-better CAD tool, a wearable that tracks five vital signs instead of curing anything.

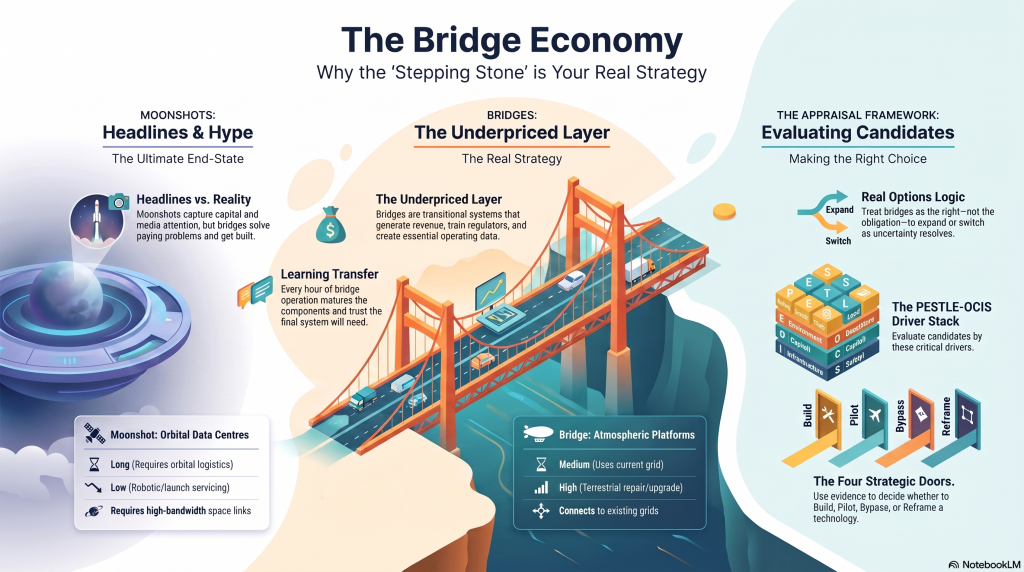

Every time, the room falls in love with the first future and starts writing checks. And every time, it’s the second thing the unglamorous, transitional, stepping-stone technology that actually ships, earns revenue, trains the regulators, and quietly becomes the infrastructure the moonshot will eventually stand on.

I’ve come to think of this as the Precursor or Bridge economy: the vast, underpriced layer of technology that exists between where we are and where the marketing decks say we’re going. This piece the first of two sets out a framework for seeing that layer clearly: for telling an ultimate goal from a bridge, a bridge from a dead end, and a dead end from a technology that was simply born thirty years too early.

The second piece, coming next, deals with the harder corporate question that follows once you can see the bridge economy: what do you actually do about it build it, spin it out, patent it and shelve it, open-source it, sell it, or let it die?

What this is not. This is not a forecast. I’m not going to tell you which of these ultimate goals will actually arrive, or when. It’s not a roadmap for any single company, and it isn’t an AI-generated list of trends dressed up as insight. It’s a way of thinking a set of questions I’ve found useful for separating genuine stepping stones from expensive distractions, applied honestly across a dozen industries at once. This is part 1 of 4

YouTube: The Precursor or Bridge Economy Part 1 :The Framework & The Ultimate Goals

1. Two kinds of technology

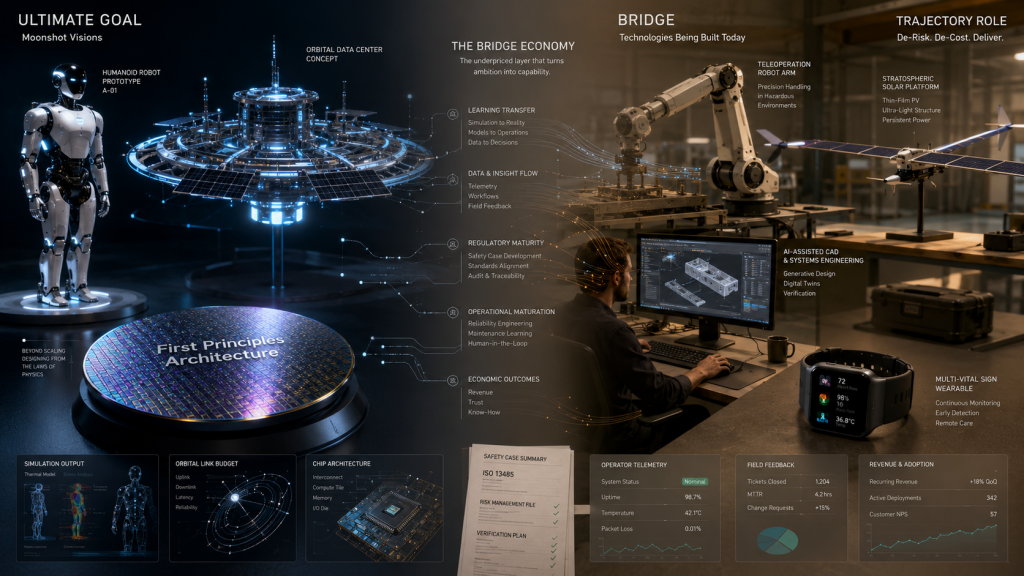

Almost every serious industrial or technological push has a shape. Somewhere at the top of the pitch deck sits an ultimate goal a singular, often beautiful, end-state vision. Fully autonomous humanoid labour. Space-based compute running on unlimited sunlight. A chip redesigned from first principles instead of forty years of silicon inheritance. An AI that designs and manufactures physical objects end to end, with no human in the loop.

Underneath that headline, almost always unglamorously, sits a second population of technologies: the bridges. They are not trying to be the ultimate goal. They solve a real, paying problem today, using more of today’s infrastructure than tomorrows, while quietly generating the data, trust, regulation, and components the ultimate goal will eventually need.

The pattern repeats with such regularity that it’s worth stating as a rule: the ultimate goal gets the capital and the headlines; the bridge gets built. Jeff Bezos’s industrial AI venture, Prometheus, is a clean recent example of a company that seems to understand this instinctively. Since launching in November 2025 with $6.2 billion and raising a further $12 billion in June 2026 at a $41 billion valuation, Prometheus has been explicit that it is not building humanoid robots or a factory of the future in one leap. Bezos has gone out of his way to say the company has “nothing to do with robotics” instead it is building what he calls an “artificial general engineer,” AI tooling that compresses the design-to-manufacturing cycle for things like jet engines and chips, a very modern, AI-native version of CAD. The ultimate goal a system that designs and builds physical products with no human engineer in the loop is the destination. What Prometheus is actually funding first is the bridge: tools that make today’s engineers dramatically faster, while the underlying “artificial general engineer” matures.

Why does this pattern hold across industries as different as energy, robotics, computing, and medicine? Four forces keep recurring:

- Capital chases the most attractive theoretical return, not the most probable near-term one. A venture story about orbital data centres running on infinite sunlight is more fundable than a story about a stratospheric platform that merely helps today’s grid even when the second is closer to revenue.

- Market narratives fixate on the end state. Once “fully autonomous” or “space-based” becomes the accepted shorthand for a sector’s future, anything that isn’t that starts to sound like a compromise, even when it is the more investable asset.

- Incumbents avoid paths that conflict with their existing business model. A company built around one architecture rarely funds the bridge that could cannibalise it even when that bridge is the more defensible near-term business (more on this in Part 2).

- Research gets shelved the moment it stops aligning with the dominant trajectory. Once an industry decides which future it’s building, anything adjacent a parallel chip architecture, an alternative substrate, an “obsolete” mechanical approach quietly stops getting funded, regardless of its underlying merit.

None of this means the ultimate goals are wrong to pursue. It means most industries are structurally bad at noticing, valuing, and building the bridges that make those goals reachable and even worse at noticing when a “temporary” bridge has quietly become a durable business in its own right.

2. Why PESTLE isn’t enough anymore

If you trained in strategy at any point in the last forty years, you know PESTLE: Political, Economic, Social, Technological, Legal, Environmental. It’s a good tool for scanning a macro-environment. It is a poor tool for answering the question that actually matters here: is this specific technology, at this specific moment, a bridge worth building, a standalone market in disguise, or a dead end?

PESTLE doesn’t ask about trajectory. It doesn’t distinguish a technology that’s genuinely transitional from one that only looks transitional because everyone assumes the “real” future looks different. It has no concept of learning transfer, lock-in risk, or the possibility that a stepping stone might outlive the destination it was built to reach. It was built to describe an environment, not to make a call.

What’s needed is PESTLE with a spine a framework that keeps the macro-scanning discipline but adds the questions that are specific to evaluating a technology’s position on a trajectory toward, alongside, or away from an ultimate goal.

3. The Pathway Fit Framework

Here is the version I use. It runs in three stages, and it is deliberately domain-agnostic I’ve applied it, in the space of a single week, to a chip architecture, a diagnostic wearable, and a stratospheric energy platform, and it holds up in all three.

Stage one — Name the trajectory role

Before scoring anything, force an honest answer to a single question: what is this technology, relative to the ultimate goal it sits nearby? There are only four honest answers.

| Trajectory role | What it means |

| Bridge | A transitional technology that solves a real problem now and feeds capability, data, or trust into the ultimate goal. |

| Parallel standalone | A technology that looks like a stepping stone but doesn’t actually feed the ultimate goal it will keep existing as its own market regardless of whether the ultimate goal ever arrives. |

| Dead end | A technology that was correctly abandoned the constraints that killed it are still true today. |

| Revival candidate | A technology that was abandoned for reasons that no longer hold the constraint that killed it has since been removed by materials, compute, energy, or AI. |

Most strategy conversations skip this step entirely and argue about scores before agreeing on what’s actually being scored. Nine times out of ten, disagreements about a technology’s value are actually disagreements about its trajectory role that nobody surfaced.

Stage two — Run the PESTLE+ scan

Once the trajectory role is named, run the classic six PESTLE lenses but add the five dimensions that PESTLE was never built to capture:

| Added lens | The question it forces |

| Learning transfer | Does building this generate data, skills, or trust that the ultimate goal will need later or is the learning a dead end in itself? |

| Lock-in risk | Could building this trap capital, regulation, or supply chains around the wrong architecture, making the real destination harder to reach? |

| Timing window | Does this have five to ten years of useful commercial life, or eighteen months before something else overtakes it? |

| Economic separability | Could this survive and monetise as its own business even if the ultimate goal is delayed by a decade, or never fully arrives? |

| Cannibalisation risk | Does pursuing this threaten an existing revenue line badly enough that the organisation’s own incentives will work against it? |

The six original PESTLE lenses still matter a technology can pass every one of the five new tests and still be dead on arrival because of an export control regime or a shifting subsidy landscape. But run alone, PESTLE tells you about the weather. PESTLE+ tells you whether to build the boat.

Stage three — Open the right door

The scan produces a recommendation, not a single number. In practice it resolves into six possible doors, which is the subject of the whole of Part 2: pursue as a bridge, spin it off, archive it (patent and shelve), seed it publicly, license or sell it, or let it die. For this article, the two that matter are the first and last of the trajectory roles above — bridge and dead end — because they set up the ultimate-goals ledger below. The other four doors are where Part 2 will spend most of its time.

4. The ultimate goals ledger

Below is a working ledger of twelve visionary end-states currently pulling serious investment and research attention, evaluated the way the framework above intends: not “will this happen,” but “what’s the dominant pathway everyone is funding, what’s being overlooked, and what bridge is quietly being built regardless.”

| Ultimate goal | Scale of investment | Dominant pathway | Overlooked alternative | Bridge technology emerging now |

| Space-based data centres | Billions across Google’s Project Suncatcher, Starcloud, and others running live orbital AI workloads since 2025 | Solar-powered compute satellites, launched at scale as reusable-rocket costs fall | Underwater data centres — abandoned by Microsoft’s Project Natick in 2024 as unmaintainable, yet built commercially by a Chinese operator off Hainan | Behind-the-meter and modular ground power, high-altitude solar and airborne-wind platforms |

| Fully autonomous humanoid robots | Tens of billions across Tesla Optimus, Figure AI, Unitree, and a wave of well-funded challengers | End-to-end learned autonomy trained on teleoperated and imitation-learning data at scale | Fixed, task-specific automation and human-worn exosuits, both cheaper and safer for narrow high-value tasks today | Teleoperated, human-supervised robots sold as a service — every operator hour is training data for the autonomy meant to replace it |

| The artificial general engineer | $18B+ raised by Prometheus alone, reportedly seeking a further $100B affiliated fund | An end-to-end AI system spanning design, simulation, and manufacturing for complex physical products | Narrower AI copilots embedded inside existing CAD, PLM, and simulation tools, with a human engineer still closing the loop | AI-assisted CAD, simulation-first engineering, and digital twins — the actual product being sold today |

| Universal AI governors (model-agnostic orchestration) | Rapidly growing spend across enterprise agent orchestration and agent-governance tooling | A single control layer that can direct any underlying model or agent toward a governed outcome | Deliberately narrow, single-vendor agent stacks that trade flexibility for auditability | Retrieval-augmented generation, the Model Context Protocol, and policy-gated action layers that verify every model-driven step |

| Next-generation AI chips, designed from first principles | Tens of billions across custom silicon, with a smaller but growing pool for non-silicon approaches | Ever-denser, ever more specialised silicon accelerators | Analog, in-memory, and optical computing architectures shelved decades ago for lack of fabrication precision and AI-scale demand | Chiplet architectures and hybrid analog-digital accelerators that borrow ideas from both camps |

| Global, energy-neutral distributed compute | Part of the broader multi-hundred-billion-dollar hyperscale AI infrastructure buildout | Centralised hyperscale data centre campuses, sited wherever power and land allow | A genuinely distributed mesh of community and home-scale AI nodes, sharing load the way rooftop solar shares generation | Edge accelerators and regional micro data centres that soften — without solving — the grid-connection bottleneck |

| Fully autonomous ground transport | Well over $100B cumulatively since the mid-2010s across the sector | Learned, end-to-end driving trained on enormous real-world and simulated mileage | Fixed-guideway and infrastructure-assisted transit, which sidesteps the hardest parts of open-world driving entirely | Geofenced robotaxis and autonomous trucking on fixed interstate corridors, now operating commercially without an in-cab safety driver |

| Autonomous scientific discovery engines | Billions across foundation models for science and “self-driving lab” startups | Foundation models generating and testing hypotheses inside largely automated robotic laboratories | Human-AI collaborative discovery, where the AI proposes and a scientist still chooses what’s worth running | AI copilots for literature synthesis and hypothesis generation, paired with partially automated lab equipment |

| The medical tricorder | Hundreds of millions since the 2012–2017 Qualcomm Tricorder XPRIZE, now folded into a much larger wearables market | A single handheld or wearable device diagnosing almost any condition without a clinician | Distributed, low-cost community health infrastructure pairing trained health workers with narrower AI tools | Multi-vital-sign wearables, point-of-care test kits, and telehealth-linked diagnostic kiosks |

| Photorealistic spatial computing (the holodeck) | Tens of billions across Apple Vision Pro, Meta’s headset line, and adjacent spatial-computing bets | All-day, fully immersive mixed-reality headsets that eventually replace the screen entirely | Lightweight AR glasses built for one narrow job — navigation, translation, notifications — rather than general immersion | Enterprise spatial computing for design and training, and glasses-free autostereoscopic displays for content and signage |

| Grid-scale fusion power | Billions across Commonwealth Fusion, Helion, TAE, and others | Magnetic confinement, chiefly tokamaks and stellarators, chasing net energy gain at commercial scale | Inertial confinement and hybrid fission-fusion designs, both historically under-resourced next to the magnetic mainstream | Superconducting magnet and plasma-diagnostics advances that are already finding commercial life outside fusion itself |

| Autonomous aerial logistics networks | Billions across cargo-drone operators and a resurgent interest in airships | Fixed-wing and rotor autonomous drones operating under evolving regulatory sandboxes | Modern airships and tethered aerostats, sidelined for a century by early accidents but revisited with new materials and hydrogen-safety systems | Low-altitude infrastructure intelligence and regulatory pilot programmes that mature the airspace rules before full autonomy needs them |

A few patterns jump out once you lay twelve unrelated industries side by side like this. First, the overlooked alternative is very often the technically simpler, not the more advanced, path — a stratospheric platform is a simpler engineering problem than an orbital data centre; a geofenced robotaxi is a simpler problem than a car that can drive anywhere. Second, the bridge is almost always what’s actually generating revenue today, while the ultimate goal is almost always what’s generating headlines. Third, and most usefully: in at least three of these twelve rows, the “overlooked alternative” and the “bridge technology” are the same idea wearing two different names which is exactly the kind of technology Part 2 will argue deserves to be spun out into its own business, rather than kept as a footnote inside someone else’s moonshot.

Enterprise response: digging for gold in the discarded pile

Enterprises should establish a formal Dormant Asset and Bridge Option Review to reassess patents, copyrighted material, old R&D, discontinued products, failed pilots, technical archives, and legacy software. The review should not ask whether these assets match the perfect future. It should ask whether they can solve today’s constraint, generate transferable learning, use existing infrastructure, and create an investable bridge toward a future system.

The framework combines IP clearance, historical failure analysis, PESTLE-OCIS environmental scanning, technical feasibility, operational readiness, capital fit, and real-options-style staged commitment. The output is not a simple yes/no decision. It is a portfolio decision: Build, Pilot, Hold, Reframe, License, Sell, or Bypass.

This is the enterprise version of the bridge economy: the systematic conversion of forgotten intellectual assets into strategic options. This will be detailed in further parts

An example: An enterprise can revisit old AI chip, architecture, substrate, cooling, and software research through a bridge economy lens.

Instead of asking whether old assets can compete directly with frontier GPUs, the framework asks whether they can solve current AI infrastructure bottlenecks: inference, retrieval, digital twins, archive intelligence, regional compute, cooling, power delivery, or specialised workloads.

The main conclusion is that the strongest opportunities are not full “post-silicon” replacements. They are layered bridge technologies:

| Opportunity | Recommended action |

| Second-life GPUs, servers, and accelerators | Build / Reframe as a circular AI compute bank |

| Mature-node chips for embeddings, retrieval, and archive search | Pilot as workload-specific accelerators |

| Diamond, SiC, and GaN materials | Build targeted pilots for thermal and power infrastructure |

| Full custom ASIC for one current LLM | Bypass for now due to lock-in and model-change risk |

| Active Cold Intelligence for enterprise archives | Build as a practical near-term product |

| Graphene, 2D materials, CNT logic replacement | Hold as option until manufacturing and integration improve |

| Cooling and heat reuse systems | Reframe as infrastructure, not just facility cost |

The practical 90-day pilot would inventory dormant chip and substrate assets, profile workloads such as embeddings and retrieval, build a small second-life compute demonstrator, then compare cost, energy use, latency, reliability, and avoided premium GPU hours against cloud alternatives.

Bottom line: old chip research should not be treated as obsolete by default. Much of it may be valuable as a bridge layer in the AI infrastructure stack, especially where it reduces cost, improves energy efficiency, supports regional compute, or activates dormant enterprise knowledge.

Conclusion: The Bridge Is Not a Compromise

The mistake is to think of bridge technologies as lesser versions of the future.

They are not.

A good bridge is not a failed moonshot. It is a technology with its own commercial logic, its own adoption curve, and its own compounding advantages. It solves something now while making something larger possible later.

That makes it strategically awkward.

It may be too practical for venture storytelling, too disruptive for incumbents, too transitional for analysts, and too unglamorous for the public imagination.

But it may also be exactly where the value is.

The central question is not whether the ultimate goal is real.

The central question is whether the path toward it contains underpriced technologies that can become durable businesses before the destination arrives.

That is the bridge economy.

And once you start seeing it, you start noticing it everywhere.

In Part 2, we move from recognition to decision. When an organisation finds itself sitting on one of these bridges, what should it do?

Build it?

Spin it out?

Patent it and wait?

Open-source it?

License it?

Sell it?

Or let it die?

That is the next problem.

And it is the one that determines whether a bridge becomes infrastructure, a business, or another forgotten footnote in someone else’s moonshot.

What to Build, Spin Off, Shelve, or Let Die

Part 2 will look at how organisations should act once they identify a bridge technology. It will cover abandoned technologies worth revisiting, the investment dynamics that starve good bridges of capital, corporate examples of missed or mishandled opportunities, and a practical decision framework for choosing which of the six doors to open.

That is where this series goes next: not which of these twelve ultimate goals will actually arrive, but what an organisation sitting on one of these bridges should do about it — pursue it, spin it out, patent it and wait, open it to the world, sell it, or let it go. That’s Part 2.

Part 2 — “What to Build, Spin Off, Shelve, or Let Die” — covers revisiting technologies the industry left for dead, the investment dynamics that starve good bridges of capital, real corporate decisions (Kodak, Xerox, Philips, Oracle, and Google’s long list of retired products), and a working criteria set for deciding, project by project, which of the six doors to open.

{kind=link}

{kind=link}

{kind=link}

{kind=link}